In April 2026, Exxon Mobil Corp (XOM) is standing at a critical valuation crossroad. While the broader S&P 500 remains flat, XOM has surged nearly 18% year-to-date, fueled by a war premium as the Strait of Hormuz faces ongoing disruptions. Despite the rally, the market is sharply divided: Bulls point to a higher for longer oil price environment and a 40-year production high as catalysts for a breakout to $180, while skeptics, including Wolfe Research, warn that the XOM stock is fairly valued and vulnerable to a $120 correction if geopolitical tensions ease.

As the energy sector faces extreme volatility, Exxon is weaponizing its low-cost asset base in Guyana and the Permian Basin to sustain a massive $37.2 billion shareholder distribution. This guide breaks down the XOM stock price prediction for 2026 using data from Trefis, Zacks Research, Wolfe Research, and 24/7 Wall St.

You will also discover how to trade Exxon Mobil (XOM) stock futures with USDT on BingX TradFi.

Top 5 Things for Exxon Mobil Investors to Know in 2026

- The 4.7 Moebd Milestone: Exxon achieved its highest annual production in over 40 years in 2025, with the Permian Basin hitting 1.8 million barrels per day, providing a massive volume buffer against price volatility.

- The $20B Buyback Engine: For 2026, Exxon has committed to a $20 billion share repurchase program, supporting its 43-year streak of dividend growth and a 2.7% yield.

- Golden Pass LNG Launch: The Exxon-QatarEnergy joint venture started LNG output in Texas in early 2026, diversifying earnings away from pure crude oil sensitivity.

- The "War Premium" Risk: Much of the 2026 rally is tied to the Persian Gulf conflict; a sudden ceasefire or reopening of the Strait of Hormuz could remove the $15–$20 risk premium currently baked into XOM’s price.

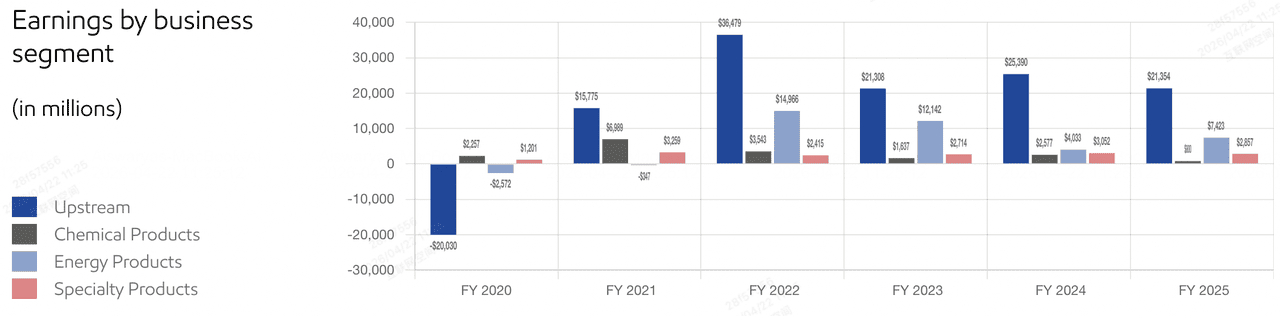

- Chemical Margin Compression: Despite upstream strength, Exxon’s Chemical Products segment posted a $281 million loss in late 2025, signaling that downstream weakness could cap total earnings growth.

What Is Exxon Mobil Corp (XOM)?

Exxon Mobil Corp's earnings | Source: ExxonMobil

Exxon Mobil Corp is the largest integrated energy company in the United States, with a market capitalization of approximately $615 billion. It operates across the entire energy value chain: Upstream (exploration and production), Energy Products (refining and fuels), Chemical Products, and Specialty Products.

Under its current strategy, Exxon has shifted focus toward advantaged assets - low-cost, high-return projects in Guyana and the U.S. Permian Basin. This transition has lowered its portfolio breakeven price to below $40/bbl, allowing the firm to remain profitable even during significant macroeconomic downturns.

Exxon enters Q2 2026 with a P/E ratio of 22.18x, which sits above its historical average. While its 2025 net income of $28.8 billion showed a slight decline due to lower year-over-year commodity prices, its structural cost savings of $15.1 billion since 2019 have created a leaner, more resilient balance sheet.

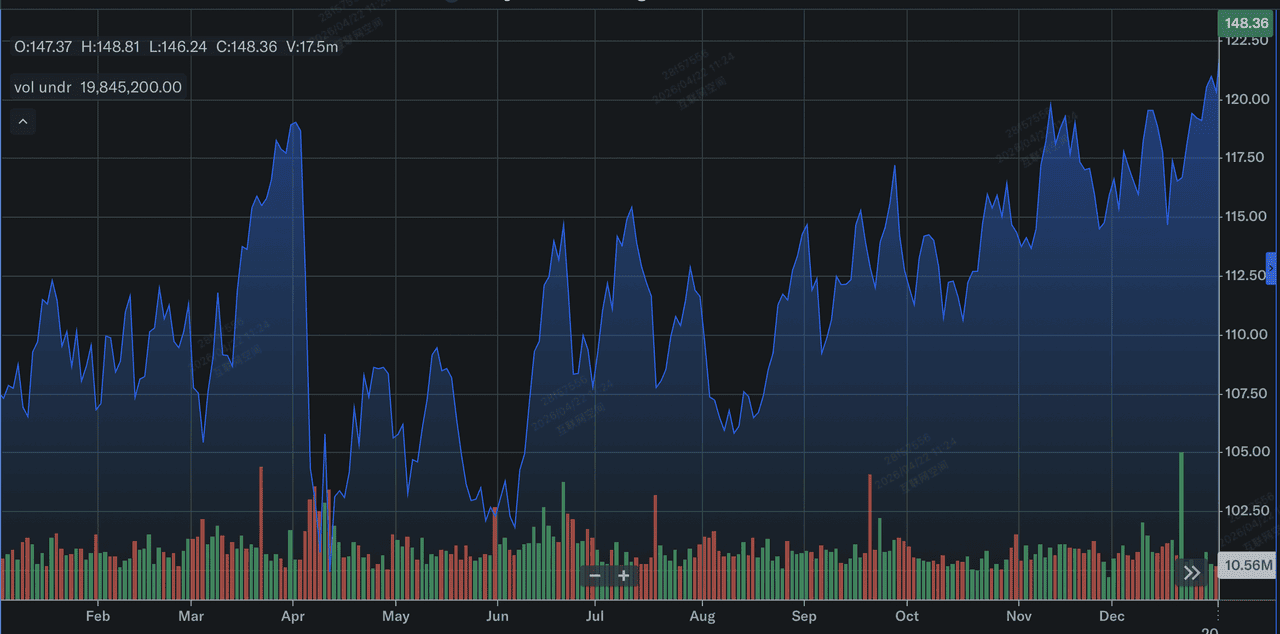

Exxon Mobile (XOM) Stock Performance in 2025: A Review

Exxon Mobil stock's performance in 2025 | Source: Yahoo Finance

Exxon Mobil (XOM) delivered a powerhouse operational performance in 2025, headlined by a record-breaking production volume of 4.7 million oil-equivalent barrels per day, its highest in over 40 years. This growth was anchored by a massive scale-up in advantaged assets, with the Permian Basin reaching 1.8 million barrels per day and Guyana approaching 875,000 gross barrels per day by year-end. Despite these volume gains, GAAP earnings of $28.8 billion reflected a 14.4% year-over-year decline as the company navigated a mean reversion in commodity prices from the highs of previous years and a $281 million loss in the Chemical Products segment during Q4.

2025 solidified Exxon’s transition into a cash-flow machine rather than a mere price-taker. The company utilized its robust $52 billion in operating cash flow to distribute $37.2 billion to shareholders via dividends and aggressive stock repurchases. For investors, the takeaway was the company's improved efficiency; by achieving $15.1 billion in cumulative structural cost savings since 2019, Exxon successfully lowered its portfolio breakeven price to below $40/bbl. This provided a high floor for the stock’s valuation, even as free cash flow faced a 15% squeeze due to a 19% hike in capital expenditures aimed at future-proofing its LNG and upstream dominance.

ExxonMobil’s 2026 Strategy: Advantaged Growth

- Permian Dominance: Following the integration of Pioneer Natural Resources, Exxon is now the dominant force in the Permian, targeting 2 million barrels per day by 2027.

- Guyana Expansion: The Stabroek block continues to outperform, with production approaching 875,000 gross barrels per day, acting as a low-cost cash cow for the firm.

- Cost Discipline: The company is on track to hit $20 billion in cumulative structural cost savings by 2030, ensuring that free cash flow (FCF) remains robust even if oil returns to $70.

Exxon (XOM) Stock 2026 Investment Outlook: $180 Alpha vs. $120 Mean Reversion

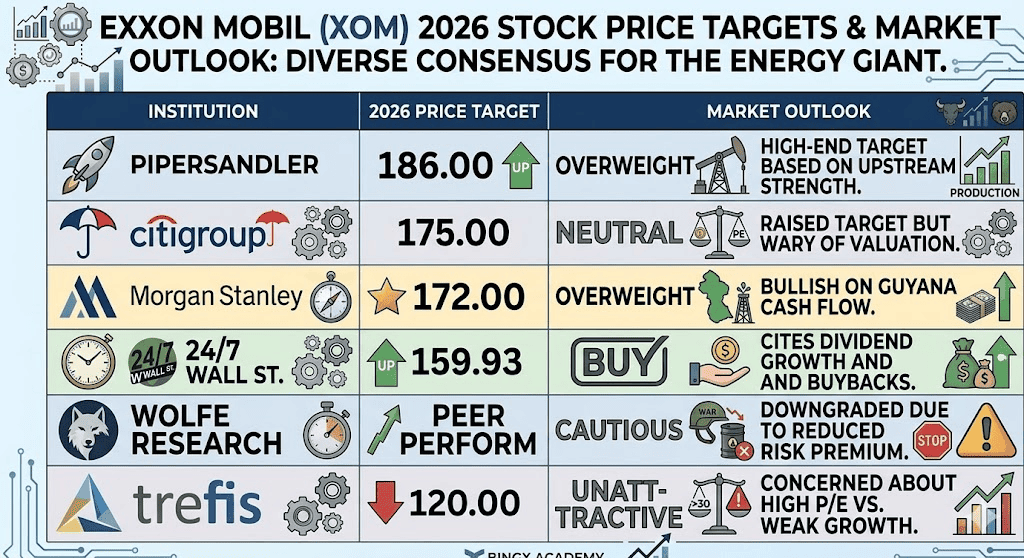

2026 ExxonMobil (XOM) stock forecast by Wall Street analysts

The 2026 outlook for XOM stock is a tug-of-war between record-breaking production and the fragility of the current geopolitical risk premium.

The Bull Case: Exxon’s $180 Commodity Supercycle

The bullish narrative is predicated on a perfect storm of supply constraints and operational execution. If the Strait of Hormuz remains blockaded through late 2026, removing roughly 20% of global oil-equivalent production from the immediate market, WTI is projected to sustain levels above $110/bbl. This environment would likely trigger a massive upward revision of EPS estimates toward the $9.50–$10.00 range, as Exxon weaponizes its record 4.7 Moebd production capacity. Investors in this scenario are betting that Exxon’s advantaged assets in Guyana and the Permian, which boast breakeven costs below $40/bbl, will capture unprecedented cash margins while competitors struggle with regional disruptions.

Practically, the $180 price target depends on a triple threat of fundamental catalysts: volume growth, price sustained by geopolitical tension, and a recovery in downstream segments. A seamless ramp-up of the Golden Pass LNG facility would add high-margin revenue uncorrelated with crude prices, while a rebound in Chemical Products following the $281 million loss in Q4 2025 would diversify the bottom line. Analysts like Citigroup argue that under these conditions, XOM would undergo a valuation re-rating, shifting from a cyclical play to a premier defensive inflation hedge with a target multiple expansion toward 18x-20x.

The Base Case: XOM at $155 Fair Value Consolidation

The base case assumes a soft landing for energy markets, where crude stabilizes in a healthy $85–$95 corridor. In this scenario, Exxon transitions from a growth stock back into the ultimate bond proxy for energy investors. The stock is expected to oscillate near its $159.93 target, supported by a rock-solid 2.7% dividend yield and a massive $20 billion share buyback program for 2026. This buyback acts as a mechanical floor for the stock price, effectively reducing share count by roughly 3–4% annually, which offsets the lack of explosive top-line growth and keeps EPS tracking in the mid-single digits.

Insightfully, this case relies on Exxon’s superior Return on Equity (ROE) of 11.2% and its ability to maintain a 59% payout ratio. Even with elevated CapEx for Permian expansion, the company’s $52 billion operating cash flow remains more than sufficient to fund both growth and shareholder returns. For the practical investor, XOM in this scenario represents the flight-to-quality benchmark. It may not offer the triple-digit alpha of tech agents, but its low 0.29 beta and best-in-class balance sheet, evidenced by a slim 0.13 debt-to-equity ratio, make it the anchor for any energy-weighted portfolio.

The Bear Case: ExxonMobil Stock at $120 Amid Geopolitical De-escalation

The bear case is defined by the sudden removal of the war premium. If U.S.-Iran negotiations in Pakistan result in a transit corridor agreement, the $15–$20 risk premium currently supporting Brent crude could evaporate in days, sending oil back toward the $60–$70 range seen in late 2025. Bears point out that at $148, the stock is trading at a 22x P/E ratio, which is priced for perfection compared to its 10-year historical average. A price correction in crude would expose the underlying weakness in Exxon's recent revenue growth, which contracted 4.5% LTM, forcing a sharp downward revaluation.

From a practical risk management perspective, the bear case highlights a potential value trap. If commodity prices mean-revert, Exxon’s high CapEx, which climbed 19.3% in 2025, could suddenly look like a liability, squeezing free cash flow and threatening the pace of future buybacks. Analysts like Wolfe Research suggest that without the tailwind of triple-digit oil, XOM is significantly overvalued relative to its $109.67 GF Value. In this risk-off environment, capital would likely rotate out of energy and back into high-growth sectors, leaving XOM to test its $120 support level as the market refocuses on the company’s lack of a long-term renewable growth engine.

Exxon Mobil (XOM) Stock Price Forecasts for 2026 By Wall Street Analysts

|

Institution |

2026 Price Target |

Market Outlook |

|

Piper Sandler |

$186.00 |

Overweight: High-end target based on upstream strength. |

|

Citigroup |

$175.00 |

Neutral: Raised target but wary of valuation. |

|

Morgan Stanley |

$172.00 |

Overweight: Bullish on Guyana cash flow. |

|

24/7 Wall St. |

$159.93 |

Buy: Cites dividend growth and buybacks. |

|

Wolfe Research |

Peer Perform |

Cautious: Downgraded due to reduced risk premium. |

|

Trefis |

$120.00 |

Unattractive: Concerned about high P/E vs. weak growth. |

How to Trade Exxon Mobil (XOM) Stock on BingX

Navigate the volatility of energy markets using BingX TradFi tools and BingX AI analysis. Whether you are hedging against a drop in oil or betting on a continued supply squeeze, BingX provides the liquidity you need.

XOM/USDT perpetuals on BingX futures market

Long or Short XOM Stock Futures on BingX

- Navigate to BingX TradFi and select Stock Futures.

- Select the XOM/USDT perpetual contract.

- Set your leverage, e.g., 2x–5x, and select Open Long if you expect oil prices to stay elevated, or Open Short to hedge against a geopolitical de-escalation.

- Set Take-Profit (TP) and Stop-Loss (SL) levels to manage risk during high-volatility news cycles.

Top 5 Risks to Watch for ExxonMobil (XOM) Investors in 2026

To successfully navigate the 2026 energy market, investors must balance ExxonMobil’s record-breaking production volumes against these five critical geopolitical and operational headwinds.

- Middle East Ceasefire: Any resolution to the Iran-Israel conflict will immediately deflate oil prices and XOM’s share price.

- Chemical Industry Glut: Sustained oversupply in global plastics and polyethylene could keep Exxon’s downstream segment in the red.

- OPEC+ Policy Shifts: A sudden decision by Saudi Arabia to regain market share by increasing production could trigger a price war.

- Climate Litigation: Ongoing legal challenges regarding carbon emissions and greenwashing remain a persistent headline risk.

- Renewable Transition Pace: A faster-than-expected global shift toward EVs could dampen long-term demand projections for refined products.

Final Thoughts: Should You Invest in Exxon Mobil (XOM) Stock in 2026?

Exxon Mobil in 2026 is a powerhouse of operational efficiency, yet its stock price is currently a hostage to global headlines. For income-focused investors, the 43 years of dividend growth and massive buybacks offer a fortress of safety. However, with the stock trading near all-time highs and a P/E of 22x, the margin of error is slim.

Conservative traders may want to wait for a cooldown toward the $135 range before entering, while those betting on sustained geopolitical instability may find XOM to be the best vehicle to capture the "energy alpha" of the decade.

Risk Reminder: Trading and investing in equities like Exxon (XOM) involves a significant risk of capital loss. The energy sector is highly sensitive to geopolitical events, OPEC+ decisions, and global recession risks. Always conduct independent due diligence before allocating capital.

Related Reading

- Crude Oil Price Forecast 2026: $140 War Premium or $60 Surplus Baseline?

- S&P 500 Forecast 2026: 7,600 Bull Run or a 6,000 Energy-Driven Crash?

- Nasdaq 100 (NAS100) Forecast 2026: 27,000 AI Breakthrough or 22,000 Stagflation Trap?

- GE Aerospace (GE) Price Prediction 2026: Can the $190B Backlog Defy Valuation Fears?