In April 2026, Taiwan Semiconductor Manufacturing Co. (TSMC) is operating at the absolute limit of global silicon capacity. While the broader tech sector faces valuation scrutiny, TSMC has just upgraded its 2026 revenue outlook to above 30% growth, anchored by an insatiable demand for AI high-performance computing (HPC). Despite a neutral market reaction to its record-smashing Q1 earnings, where profit surged 58% to $18.2 billion, the company remains the undisputed bottleneck of the AI revolution. Investors are currently at a crossroads: Bulls point to a virtual monopoly on 3nm/2nm logic chips and a 66.2% gross margin as catalysts for a surge toward $500+, while skeptics warn that a $56 billion spending spree and a 33% overvaluation premium make the stock vulnerable to a geopolitical black swan.

As the second half of 2026 approaches, TSMC is pivoting from a mere manufacturer into a strategic global asset. With CEO C.C. Wei pulling in all equipment to meet orders from Nvidia, Apple, and AMD, the company is aggressively expanding its footprint in Arizona and Japan. This guide breaks down the TSM stock price prediction for 2026 using data from Bloomberg, Reuters, and Aletheia Capital.

You will also discover how to gain exposure to TSMC stock futures through BingX TradFi.

Top 5 Things for TSMC Investors to Know in 2026

- The 30% Growth Upgrade: TSMC officially raised its 2026 revenue guidance from nearly 30% to above 30% in U.S. dollar terms, citing extremely robust AI demand that shows no sign of slowing.

- The $56B Capex Ceiling: The company is hitting the upper bound of its $52–$56 billion capital expenditure range, aggressively investing in 3nm expansion and the 2nm N2 ramp-up.

- HPC Overthrows Mobile: For the first time, High-Performance Computing (HPC) accounts for 61% of revenue, officially dwarfing the smartphone segment (26%) as the company’s primary growth engine.

- The 66% Margin Miracle: Despite warnings of dilution from overseas fabs, TSMC reported a staggering 66.2% gross margin in Q1 2026, showcasing immense pricing power over its dependent customer base.

- Geopolitical Supply Risks: Volatility in the Middle East has raised concerns over the supply of critical gases like helium and hydrogen; while TSMC maintains safety stocks, any prolonged disruption could impact 2027 profitability.

What Is Taiwan Semiconductor Manufacturing Co. (TSM)?

TSMC is the world's largest dedicated semiconductor foundry, commanding over 70% of the global market share for advanced nodes. Founded in 1987, it is the sole provider capable of mass-producing the sub-7nm chips required for modern AI data centers, autonomous vehicles, and high-end smartphones.

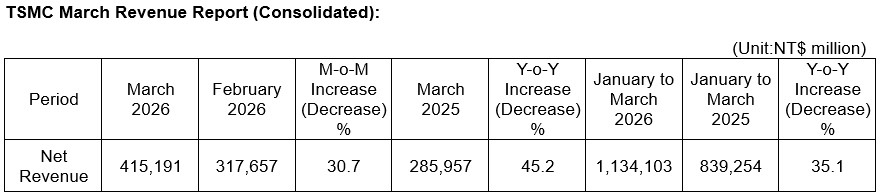

TSCMC Q1 2026 earnings highlights | Source: TSMC

Under the leadership of CEO C.C. Wei, TSMC operates as the Switzerland of the tech world, manufacturing designs for rivals like Intel and partners like Nvidia alike. It enters Q2 2026 with a market capitalization of approximately $1.95 trillion, trading as a premium infrastructure play on the global shift toward decentralized AI and agentic workflows.

TSMC enters the mid-year period with a Q2 revenue forecast of $39 billion to $40.2 billion, representing a 10% sequential increase. With a PEG ratio of 0.6, the stock presents a unique paradox: it is historically expensive at a 35x TTM P/E, yet fundamentally cheap when measured against its projected triple-digit earnings growth through 2028.

Read more: TSMC (2330) Posts Record Q1 Profit on AI Surge: Why Did TSM Stock Slip Despite a 58% Earnings Beat?

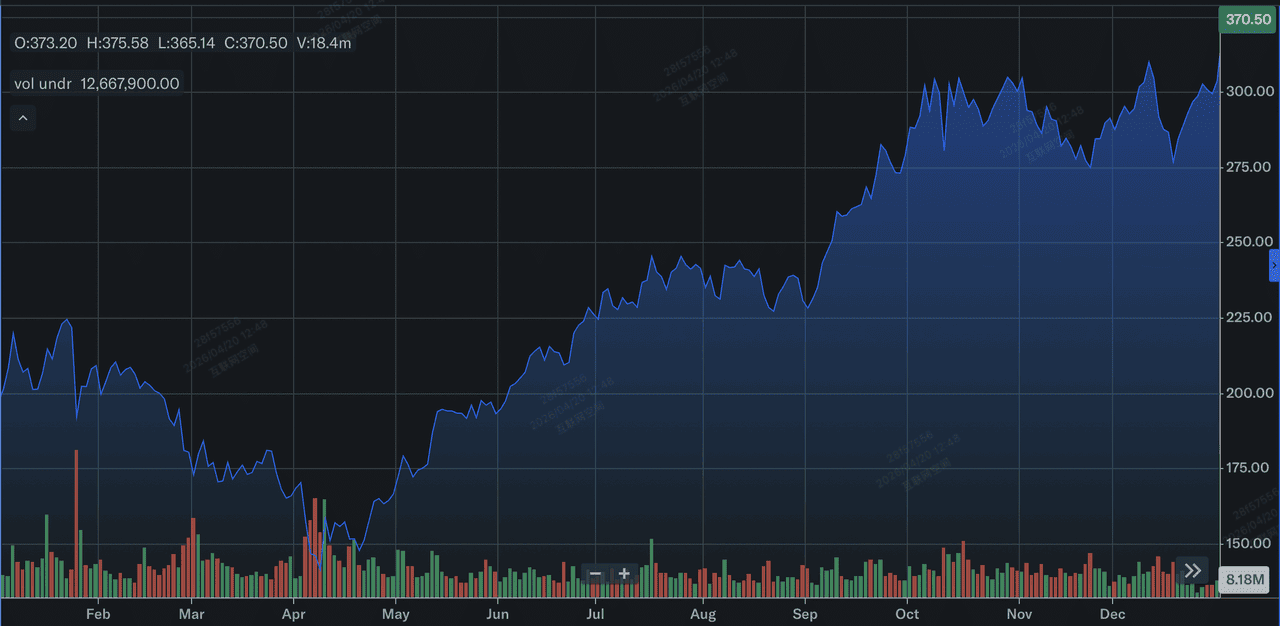

TSMC (TSM) Stock Performance in 2025: A Review

Taiwan Semiconductor Manufacturing Company Limited (TSMC) stock performance in 2025 | Source: Yahoo Finance

In 2025, TSMC delivered a powerhouse financial performance, recording a 31.6% increase in full-year revenue to NT$3,809.05 billion or approximately $122 billion. This growth was catalyzed by a structural shift toward High-Performance Computing (HPC), which surged 48% year-over-year to account for 58% of total 2025 revenue. Profitability remained exceptional despite the heavy capital burden of overseas expansion, with full-year gross margins averaging 59.9% and annual EPS climbing 46.4% to NT$66.25. Strategically, 2025 marked the year TSMC effectively de-risked its reliance on mobile by establishing AI-driven HPC as its primary and most resilient growth engine.

Technologically, TSMC achieved its most critical roadmap milestone by beginning mass production of 2-nanometer (N2) chips in Q4 2025. By the end of the year, advanced technologies of 7nm and below reached 74% of total wafer revenue, up from 69% in 2024, with the 3nm node alone contributing 24% of the annual total. This transition was supported by a massive $40.9 billion capital expenditure program, which funded the ramp-up of the Arizona and Kaohsiung fabs. For investors, the takeaway from 2025 is TSMC’s unparalleled execution: the company successfully stabilized 2nm yields between 60% and 70% during its initial rollout, significantly outpacing rivals and securing its monopoly on the next generation of AI hardware.

TSMC’s 2026 Strategy: The Foundry Monopoly

- The 2nm Transition: TSMC is currently converting 5nm tools to 3nm and preparing the first 2nm (N2) production lines in Taiwan. This node is expected to be the most significant performance leap in a decade.

- Global Diversification: To mitigate Taiwan risk, TSMC is accelerating volume production at its Arizona and Tainan GIGAFAB clusters, with U.S.-based 3nm production scheduled for late 2027.

- Advanced Packaging (CoWoS): Beyond just making chips, TSMC is expanding its proprietary Chip on Wafer on Substrate capacity, which is the current industry bottleneck for Nvidia’s Blackwell and Rubin GPU architectures.

TSM Stock 2026 Investment Outlook: $600 Alpha vs. $280 Valuation Risk

The 2026 outlook for TSM is a tug-of-war between its role as the AI Godhead and the reality of mounting operational costs in the U.S. and Japan.

The Bull Case: TSMC’s $600 Alpha Breakout

The bullish narrative centers on TSMC’s transformation into the ultimate AI toll booth, where a massive EPS doubling by 2028 is driven by an unprecedented hardware supercycle. If TSMC maintains its 66.2% gross margins, beating its long-term target of 53%, it proves that its pricing power is effectively absolute. By successfully transitioning to the 2nm (N2) node with stable yields, TSMC captures the entire high-end market, validating its $56 billion capex not as a burden, but as a high-ROI barrier to entry that competitors simply cannot fund.

Practically, this scenario relies on the market re-rating TSM from a cyclical foundry to a SaaS-like infrastructure platform. With a 30%+ revenue growth rate and a PEG ratio trending toward 0.6, the stock becomes a magnet for institutional alpha seekers. As the AI megatrend shifts from experimental hype to massive physical data center installation, TSMC’s dominance in CoWoS in advanced packaging creates a secondary revenue moat, potentially propelling the ADR price toward the $600 psychological ceiling.

The Base Case: TSM’s $420 Fair Value Consolidation

The base case views TSMC as the essential market compounder, expected to reach a mean analyst target of $423.50. This outlook assumes a soft landing for the global economy, where the total addressable market for AI chips remains robust at the projected $650 billion spend level. While the second half of 2026 will introduce a 2% to 4% margin dilution as the Arizona fabs ramp up, the sheer volume of 3nm orders from Big Tech anchors, Apple, Nvidia, and AMD, acts as a massive floor for earnings, keeping the stock in a healthy consolidation phase.

For investors, this scenario frames TSM as the ultimate 'buy the dip' asset. Revenue is expected to track steadily with the 32% year-over-year jump projected for Q2 2026, supported by a 10% sequential increase in wafer shipments. Even with high operational expenses, TSMC’s $11.1 billion quarterly capex ensures it remains the gold standard for global tech supply chains. At this level, the stock provides a reliable 0.90% dividend yield and trades in line with its premium 35x P/E, reflecting its status as a defensive fortress in the tech sector.

The Bear Case: TSMC Stock at $280 Amid Margin Compression

The bear case is triggered by the Value Trap realization, where the current 33% overvaluation relative to the intrinsic $281.67 GF Value leads to a sharp multiple compression. This downward pressure would likely stem from an external shock, such as a helium or hydrogen supply crunch caused by Middle East volatility, which could spike specialty chemical costs. If Elon Musk’s Terafab project or Japan's Rapidus Corp demonstrate viable 2nm pilot results by late 2026, TSMC’s unassailable monopoly would face its first legitimate threat in decades.

In this risk-off environment, TSM would likely test its 52-week support floor of $280–$290. Investors would focus on the 3% to 4% margin dilution from overseas expansion as a structural liability rather than a strategic asset. If credit card delinquencies or a broader recession dampen the smartphone market, the 26% revenue share from mobile could drag down overall growth. This scenario essentially strips away the AI premium, pricing TSM as a traditional capital-intensive manufacturer exposed to rising geopolitical and energy costs.

TSMC Stock Price Forecasts for 2026 By Wall Street Analysts

|

Institution |

2026 Price Target |

Market Outlook |

|

Aletheia Capital |

$600 |

Buy: EPS to double by 2028; aggressive expansion. |

|

Needham |

$480 |

Buy: Unmatched 66% gross margin expansion. |

|

Wedbush |

NT$2,400 (~$445 ADR) |

Outperform: Competitive risk is years away. |

|

J.P. Morgan |

NT$2,400 (~$445 ADR) |

Overweight: Solid Q2 guidance; market share leader. |

|

GuruFocus |

$281.67 |

Modestly Overvalued: Minimal margin of safety. |

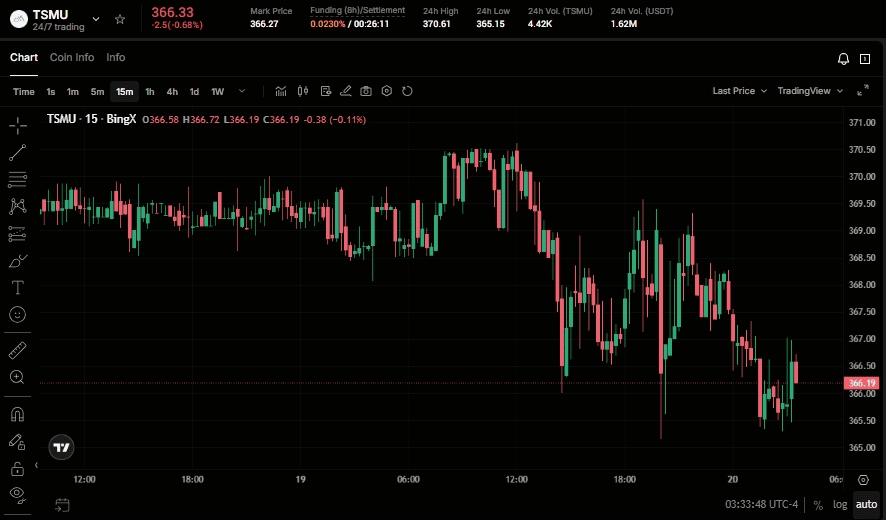

How to Trade Taiwan Semiconductor (TSMC) on BingX

Navigate the volatility of the AI hardware cycle using BingX AI and BingX TradFi tools. Whether you are hedging against geopolitical risk or going long on the 2nm transition, BingX provides the liquidity you need.

TSMU/USDT perpetual futures on BingX

Long or Short TSMU Stock Futures on BingX

- Navigate to BingX TradFi and select Stock Futures.

- Select the TSMU/USDT perpetual contract.

- Set your leverage, e.g., 2x–5x, and select Open Long if you expect a Q3 revenue beat, or Open Short to hedge against margin dilution risks.

- Set Take-Profit (TP) and Stop-Loss (SL) levels to manage the high-volatility nature of the semiconductor sector.

Top 5 Risks to Watch for TSM Investors in 2026

To successfully navigate the 2026 semiconductor market, investors must balance TSMC’s tech-driven dominance against these five critical macro and operational headwinds.

- Arizona Execution Risk: Any delays in the 2027 volume production timeline for U.S. fabs could lead to massive capital write-downs.

- Resource Constraints: The global sold-out environment for equipment like ASML machines could cap TSMC’s upside despite high demand.

- 2nm Yield Rates: As transistors shrink to 2nm, the complexity of manufacturing increases exponentially; any yield miss would crush margins.

- Energy Stability: TSMC is a massive consumer of electricity; any instability in Taiwan’s power grid or rising energy costs in the U.S. remains a threat.

- Competitive Entrants: While shortcuts are impossible, the combined $100 billion+ backing of Intel, Tesla, and Rapidus represents a long-term threat to the monopoly.

Final Thoughts: Should You Invest in TSMC Stock (TSM) in 2026?

TSMC in 2026 is the primary beneficiary of the global race for AI sovereignty. With an upgraded 30% growth target and a pivot toward the higher-margin HPC segment, the fundamental case for TSM has never been stronger. However, the 35x P/E ratio and the $56 billion capex requirements suggest that this is no longer a hidden gem but a priced for perfection titan.

For investors, the key indicator for the rest of 2026 will be margin resilience. If TSMC can absorb the costs of global expansion without dropping below a 60% gross margin, it will likely remain the gold standard of the tech industry. Conservative traders may wait for a consolidation toward the $330 level, while those seeking AI alpha may find TSM the most durable play in a volatile market.

Risk Reminder: Trading and investing in equities like TSM involves a significant risk of capital loss. Semiconductor stocks are highly cyclical and sensitive to geopolitical tensions, trade restrictions, and global manufacturing supply chains. Always conduct independent due diligence before allocating capital.

Related Reading

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

- Apple (AAPL) Stock Outlook for 2026: MacBook Neo Growth or AI Valuation Trap?

- Intel (INTC) Stock Forecast 2026: Foundry Breakthrough to $89 or Value Trap?

- Tesla (TSLA) Stock Outlook for 2026: Can the Great AI and Robotaxi Pivot Take TSLA Stock to $600?

- ASML Holding (ASML) Stock Price Forecast 2026: AI Infrastructure King or Geopolitical Target?