ASML Holding NV (ASML) entered mid-July 2026 after one of the strongest quarters in its history. On July 15, the company reported second-quarter total net sales of €9.3 billion and net income of €2.9 billion, both above guidance, then raised its full-year 2026 outlook to €43 billion to €45 billion from €36 billion to €40 billion. ASML shares rose about 2% on the print toward $1,815, still short of the $1,999.96 52-week high but up more than 65% year to date.

The raise mattered more than the beat. ASML had entered July down about 11% on the month as the market began pricing a peak in AI capital spending, dragging the Philadelphia Semiconductor Index as much as 16% below its June record. A guidance lift of roughly €6 billion at the midpoint, alongside plans to add 30% EUV and immersion capacity for 2027, is difficult to reconcile with a cycle that is topping out.

The ASML stock forecast for 2026 now centers on two competing views:

- The structural demand case: Bulls expect a 2027 order book that management describes as nearly complete, 30% capacity expansion, and live equipment price increases to support a breakout, with analyst targets ranging as high as $2,623.

- The peak-out case: Bears see hyperscaler capex decelerating into a heavily back-loaded second half, with a stock above 50 times forward earnings leaving no room for a delivery miss.

This guide breaks down the ASML stock forecast, 2026 price scenarios, key risks, and research from Bernstein, BofA, JPMorgan, Wells Fargo, RBC and Jefferies, drawing on the July 15 press release and the Q2 investor call, plus how to trade ASML stock futures on BingX TradFi with USDT collateral.

Top 5 Things for ASML Investors to Know in July 2026

- Q2 sales of €9.3 billion and margin of 54.0% both beat guidance: Net income reached €2.9 billion with basic EPS of €7.59, against a consensus near €2.62 billion, driven primarily by Installed Base Management sales that came in roughly €300 million above plan.

- Full-year guidance was raised to €43 billion to €45 billion: The third increase of 2026 lifted the range from €36 billion to €40 billion, with gross margin guidance moving to 54% to 56% from 51% to 53%.

- Q3 guidance implies a step change: Management guided Q3 net sales of €11.0 billion to €12.0 billion at a 55% to 57% gross margin, well above the €9.3 billion just delivered.

- Capacity is expanding 30% and 2027 is nearly sold out: ASML plans to add 30% to both low-NA EUV capacity of around 65 units and DUV immersion capacity of around 130 units for 2027, with another 30% under investigation for 2028. Fouquet said the company is close to having all the orders it needs for 2027.

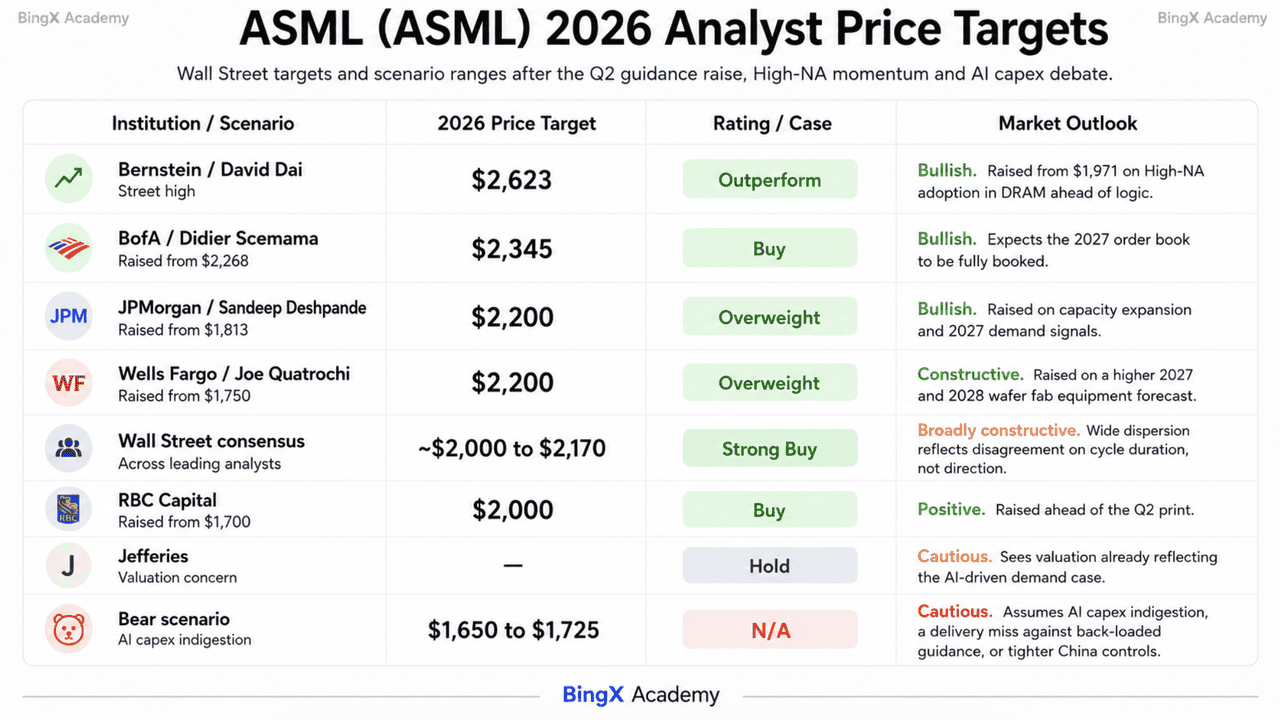

- Analyst targets run from $1,650 to $2,623: Bernstein's David Dai raised to $2,623, BofA sits at $2,345, JPMorgan and Wells Fargo at $2,200, and RBC lifted to $2,000, against a broad consensus that clusters near $2,000 to $2,170.

What Is ASML Holding NV (ASML)?

ASML Holding NV is a Dutch multinational headquartered in Veldhoven and the world's leading supplier of photolithography systems, with more than 44,500 employees. It is the only company capable of manufacturing Extreme Ultraviolet (EUV) lithography machines, the tools required to print the patterns inside the most advanced AI, high-performance computing and memory chips. That position gives ASML effective monopoly economics at the base of the semiconductor supply chain.

The business has two revenue engines. System sales cover EUV, High-NA EUV and DUV immersion tools, with 86 new lithography systems sold in Q2 alone. Installed Base Management, which covers net service and field option sales, delivered €2.8 billion in the quarter and grew 28.1% across the first half to €5.2 billion, a recurring high-margin stream that scales with every machine ever shipped. Customers include TSMC, Intel and Samsung. Intel Foundry confirmed in July that it is using High-NA EUV on its 18A process node, the first high-volume logic product to reach that milestone. Capital returns run through a €12 billion 2026 to 2028 buyback, with roughly €1.1 billion repurchased in Q2, alongside an interim 2026 dividend of €1.88 per share payable August 5.

ASML (ASML) Q2 2026 Earnings: What Drove the Beat and the Guidance Raise

- Installed Base Management carried the upside. Service and field option sales reached €2.8 billion, roughly €300 million above expectations, and were the single largest reason sales and margin cleared guidance.

- System volume stepped up sharply. ASML sold 86 new lithography systems in Q2 against 67 in Q1, with total net sales rising from €8,767 million to €9,326 million sequentially.

- Gross margin expanded despite a conservative guide. Management had guided 51% to 52% for the quarter and delivered 54.0%, ahead of the 53.7% posted in Q2 2025.

- Order intake stayed extremely strong through the first half. Fouquet described customer commitments across the full product portfolio and said visibility into longer-term demand has increased, even though ASML no longer discloses quarterly bookings.

- Pricing power is now an explicit lever. CFO Roger Dassen said the current environment provides a favorable opportunity for equipment price increases and that discussions with customers are underway, with magnitude and timing not yet announced.

ASML Holding Q2 2026 Financial and Consensus Profile: Revenue, EPS and Margins

ASML's Q2 print showed a company beating its own guidance while raising the bar substantially for the rest of the year. The €43 billion to €45 billion full-year range implies a heavily back-loaded second half, which places the burden on Q3 and Q4 delivery timing rather than on demand.

|

Financial Metric |

Guidance / Consensus |

Reported / Actual |

Surprise |

|

Q2 2026 Total Net Sales |

€8.4 to €9.0 billion guided |

€9.33 billion |

Above guidance; up from €8.77 billion in Q1 |

|

Q2 2026 Gross Margin |

51% to 52% guided |

54.00% |

Well above guidance; up from 53.7% a year ago |

|

Q2 2026 Net Income |

~€2.62 billion consensus |

€2.92 billion |

Beat; basic EPS of €7.59 |

|

Q2 2026 Installed Base Management |

~€2.5 billion expected |

€2.76 billion |

~€300 million above plan; the main source of upside |

|

Q2 2026 New Systems Sold |

— |

86 units |

Up from 67 units in Q1 |

|

H1 2026 Total Net Sales |

— |

€18.09 billion |

Up 17.2% year over year |

|

Q3 2026 Sales Guidance |

— |

€11.0 to €12.0 billion |

Implies a sharp sequential step up |

|

FY2026 Sales Guidance |

€36 to €40 billion prior |

€43 to €45 billion |

Third raise of the year; roughly €6 billion higher at the midpoint |

|

FY2026 Gross Margin Guidance |

51% to 53% prior |

54% to 56% |

Raised alongside revenue |

For context, Q1 2026 delivered €8.77 billion of net sales at a 53.0% gross margin with €2.76 billion of net income, which itself prompted a raise to €36 billion to €40 billion. Full-year 2025 revenue was €32.67 billion, up 15.6%, with earnings of €9.61 billion. China now represents roughly 20% of total net sales, though Dassen noted that percentage applies to a higher revenue base than expected earlier in the year, with the incremental demand primarily domestic-led logic.

ASML (ASML) 2026 Investment Outlook: $2,345 Bull Case vs. $1,650 Bear Case

ASML’s outlook for the rest of 2026 depends on one central question: whether the AI capex cycle behind its latest guidance increase still has years to run or is beginning to peak.

The Bull Case: ASML Breaks $2,000 and Moves Toward $2,345

The bull case rests on order visibility. ASML raised full-year revenue guidance by roughly €6 billion at the midpoint and increased its margin outlook at the same time. Management also said the company is close to securing the orders needed for 2027, even as it plans to expand EUV capacity by 30%, with a large number of 2028 EUV orders already received.

This scenario requires Q3 revenue of €11.0 billion to €12.0 billion to arrive on schedule. BofA raised its target to $2,345, JPMorgan and Wells Fargo moved to $2,200, and Bernstein reached $2,623 on expectations that High-NA adoption will expand into DRAM. Intel Foundry’s use of High-NA on 18A and ASML’s €12 billion buyback add further support. A break above the $1,999.96 high would strengthen the path toward the $2,170 consensus range and higher.

The Base Case: ASML Consolidates Between $1,725 and $2,000

In the base case, ASML delivers its raised guidance without another major valuation expansion. Q3 lands within the €11.0 billion to €12.0 billion range, full-year revenue finishes near the midpoint of €43 billion to €45 billion, and the stock digests a gain of more than 65% year to date.

Installed Base Management growth of 28% in the first half provides a recurring revenue floor, while the buyback supports demand for the shares. With support near $1,725 and resistance around $1,840 and $1,999.96, steady execution could keep ASML in the high $1,700s to just below $2,000 as analysts raise their 2027 and 2028 forecasts.

The Bear Case: ASML Falls Toward $1,650

The bear case requires customers to slow capacity spending rather than ASML losing its technology lead. Concerns about an AI capex peak already pushed the stock down 11% in early July, and the low end of Wall Street’s target range sits near $1,650.

A cut to memory or logic expansion plans would be the clearest trigger. ASML trades above 50 times forward adjusted earnings and around 16 times sales, leaving limited room for a delivery miss. China still represents close to 20% of sales, and tighter export restrictions on immersion DUV systems could pressure a profitable revenue stream. If AI hyperscalers shift from infrastructure build-out toward utilization as ASML expands capacity, the stock could retest $1,725 before moving toward $1,650.

ASML Stock Price Forecasts for 2026 By Wall Street Analysts

Wall Street is close to unanimous on direction and widely dispersed on magnitude. All of the analysts covering ASML carry a Buy or Strong Buy with the exception of a small number of Holds, and the target range spans roughly $1,000 from low to high.

|

Institution |

2026 Price Target |

Rating |

Market Outlook |

|

Bernstein / David Dai |

$2,623 |

Outperform |

Street high. Raised from $1,971 on High-NA adoption in DRAM ahead of logic. |

|

BofA / Didier Scemama |

$2,345 |

Buy |

Bullish. Raised from $2,268 expecting the 2027 order book to be fully booked. |

|

JPMorgan / Sandeep Deshpande |

$2,200 |

Overweight |

Bullish. Raised from $1,813 on capacity expansion and 2027 demand signals. |

|

Wells Fargo / Joe Quatrochi |

$2,200 |

Overweight |

Constructive. Raised from $1,750 on a higher 2027 and 2028 wafer fab equipment forecast. |

|

Wall Street consensus |

~$2,000 to $2,170 |

Strong Buy |

Broadly constructive. Wide dispersion reflects disagreement on cycle duration, not direction. |

|

RBC Capital |

$2,000 |

Buy |

Positive. Raised from $1,700 ahead of the Q2 print. |

|

Jefferies |

— |

Hold |

Cautious. Sees valuation already reflecting the AI-driven demand case. |

|

Bear scenario |

$1,650 to $1,725 |

N/A |

Cautious. Assumes AI capex indigestion, a delivery miss against back-loaded guidance, or tighter China controls. |

How to Trade ASML Holding NV (ASML) Stock on BingX

Navigate the volatility of ASML's earnings cycle using BingX TradFi and BingX AI tools. By leveraging AI-driven predictive analytics, you can better anticipate market sentiment shifts and price action around quarterly releases.

Step 1: Access BingX TradFi. Sign up and navigate to the specialized TradFi section on the main BingX exchange dashboard.

Step 2: Select ASML Holding NV (ASML). Search for and select the ASML-USDT perpetual futures contract.

Step 3: Choose your direction. Select Open Long if you expect Q3 delivery to track toward the raised guidance, the 2027 order book to fill as management indicated, and equipment price increases to lift margins further. Select Open Short if you expect hyperscaler capex to decelerate, back-loaded second-half targets to slip on delivery timing, or export controls to tighten around the 20% China base.

Step 4: Select leverage and margin mode. Choose Isolated or Cross-Margin based on your risk tolerance. Because options markets priced an 8.36% move around the Q2 print, more than double ASML's four-quarter average, conservative leverage and clear position sizing are important.

Step 5: Execute strict risk protocols. Set Take-Profit and Stop-Loss (TP/SL) levels before or immediately after entering the trade. ASML can react quickly to quarterly earnings, hyperscaler capex commentary, Dutch and U.S. export control headlines, High-NA qualification milestones at TSMC and Intel, and memory pricing news.

Top 5 Risks to Watch for ASML Investors in 2026

To navigate the second half of 2026, investors must weigh ASML's monopoly economics and raised guidance against these five structural and macro headwinds.

- AI capex indigestion is the sector's dominant fear: The peak-out debate pulled the Philadelphia Semiconductor Index as much as 16% below its June record and ASML down 11% in early July. If hyperscalers pivot from build-out to utilization, order intake, the metric the stock is most sensitive to, turns first.

- Second-half guidance is heavily back-loaded: Reaching €43 billion to €45 billion requires roughly €25 billion of delivery across Q3 and Q4 after €18.09 billion in the first half. Shipment timing and product mix, not demand, become the swing factor.

- The valuation leaves no room for error: ASML trades above 50 times forward adjusted earnings and roughly 16 times sales. A single delivery miss or a customer trimming capacity plans could trigger a sharp de-rating regardless of the order book.

- China sits near 20% of sales with policy unresolved: Management has guided China to roughly 20% of total net sales, down from more than 30% previously. Further allied restrictions on immersion DUV tools would remove high-margin revenue that Western demand may not immediately replace.

- Capacity expansion is a bet on a cycle continuing: Adding 30% EUV and immersion capacity for 2027 with another 30% under investigation for 2028 commits capital years ahead of the revenue. If demand cools mid-build, the operating leverage that drove this quarter's margin beat reverses.

Final Thoughts: Should You Invest in ASML in 2026?

ASML after the July 15 report is a story of a monopoly that just told the market the cycle is bigger than it thought. A €9.3 billion quarter above guidance, a 54.0% margin above guidance, a full-year raise to €43 billion to €45 billion, 30% capacity expansion, and a 2027 order book near complete are not in dispute. What is in dispute is what an investor should pay for a business whose earnings power is this dependent on a capital spending wave it does not control.

The bull case is that ASML is the toll booth on the entire AI build-out, sold out through 2027, with pricing power its CFO is now openly discussing and a €12 billion buyback underneath. The bear case, held by a minority of the Street while most raised targets, is that above 50 times forward earnings the stock already reflects several years of that thesis, and that the first sign of hyperscaler restraint would hit the order book before it hits revenue. Investors who believe the AI infrastructure cycle has years left may find ASML the highest-quality expression of that view. More conservative traders might wait for Q3 to convert the back-loaded guidance before adding, using the $1,725 support and the $1,999.96 high as the levels that define the range.

Risk Reminder: Trading and investing in equities like ASML involves a high risk of capital loss. ASML is subject to stringent export controls, geopolitical friction between the U.S. and China, and a valuation that amplifies any disappointment. Conduct independent research before allocating capital.

Related Reading

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

- Palantir (PLTR) Stock Outlook for 2026: Can AI-Driven Enterprise Supercycle Take PLTR to $235+?

- Oracle (ORCL) Stock Price Outlook for 2026: Can AI Cloud Infrastructure Take ORCL Back to Its Highs?

- Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?

- Broadcom (AVGO) Stock Outlook for 2026: AI Infrastructure King or Margin Victim?

- IBM (IBM) Price Prediction 2026: Can IBM Recover From the 25% Drop After a Q2 Revenue Miss?