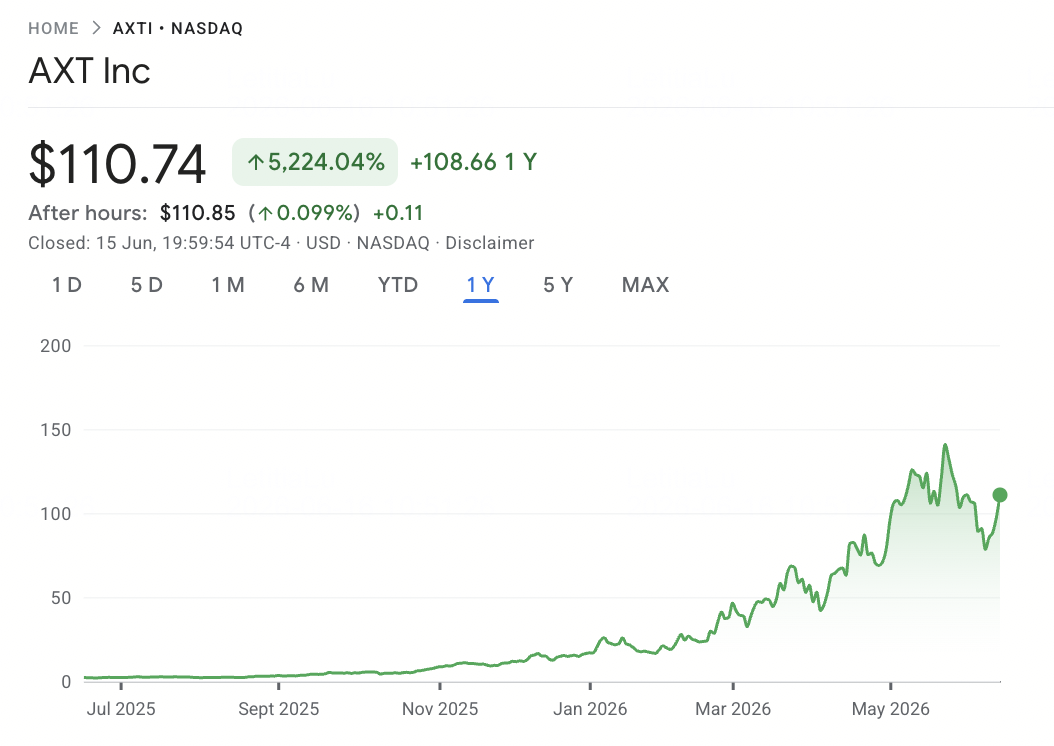

In early June 2026, AXT Inc. (Nasdaq: AXTI) has become one of the biggest semiconductor materials stories of the year. After trading below $15 at the start of 2026, AXTI surged to an all-time high of $96.00 on May 1, driven by rising demand for indium phosphide substrates used in high-speed optical transceivers for AI data centers.

The bull case is built on AXT’s record InP backlog of more than $100 million, a plan to double InP capacity in both 2026 and 2027, and a $632.5 million equity raise to fund the Beijing Tongmei expansion. The risk is that much of this optimism is already reflected in the stock after a 600%+ year-to-date rally, while export permit timing, Tongmei listing execution, and short-seller pressure remain key uncertainties. This guide breaks down the AXT stock forecast, 2026 price scenarios, key risks, and how to trade AXTI stock futures on BingX TradFi with USDT collateral.

Why Is AXT Inc. (AXTI) Stock Surging in 2026?

AXT’s 2026 rally is driven by a sharp shift in how investors value the company. Instead of viewing AXTI only as a cyclical compound semiconductor substrate supplier, the market is now pricing it as a key supplier of indium phosphide substrates for AI data center optical infrastructure.

- AI data center demand is driving record InP backlog: AXT reported Q1 2026 revenue of $26.9 million, up 39% year over year, with indium phosphide contributing $13.6 million, or more than half of total revenue. The InP backlog reached a record $100 million as demand rose for optical transceivers used in 800G, 1.6T, and next-generation AI data center interconnects. Non-GAAP gross margin also improved to 29.9%, supported by higher volume and richer InP mix.

- Vertical integration strengthens AXT’s capacity advantage: AXT designs its own crystal growth furnaces at Beijing Tongmei and controls indium feedstock through its Jinmei subsidiary. This gives the company more control over cost, capacity, and production quality than substrate suppliers that rely more heavily on third-party equipment or external raw materials.

- The $632.5 million equity raise funds major expansion: In April 2026, AXT raised $632.5 million to expand InP capacity and support 6-inch wafer R&D. Management aims to double InP output in 2026 and again in 2027, targeting quarterly capacity of about $65 million to $70 million by the end of 2027. The offering created dilution, but it also gave AXT the capital needed to chase a much larger AI optical infrastructure opportunity.

- Q2 profitability guidance signals an inflection point: Management guided Q2 2026 EPS to $0.06 to $0.08, which would mark the company’s first profitable quarter in years. This shifts the investor debate from loss control to potential earnings power if InP demand, pricing, and capacity expansion continue to improve.

- Tongmei STAR Market listing adds valuation optionality: Beijing Tongmei, AXT’s main manufacturing subsidiary in China, is pursuing a STAR Market listing. A successful IPO could give Tongmei access to independent capital, create a separate valuation for AXT’s China-based substrate operations, and add upside if Chinese AI infrastructure materials companies continue to trade at premium multiples.

Read More: Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure

What Is AXT Inc. (Nasdaq: AXTI)?

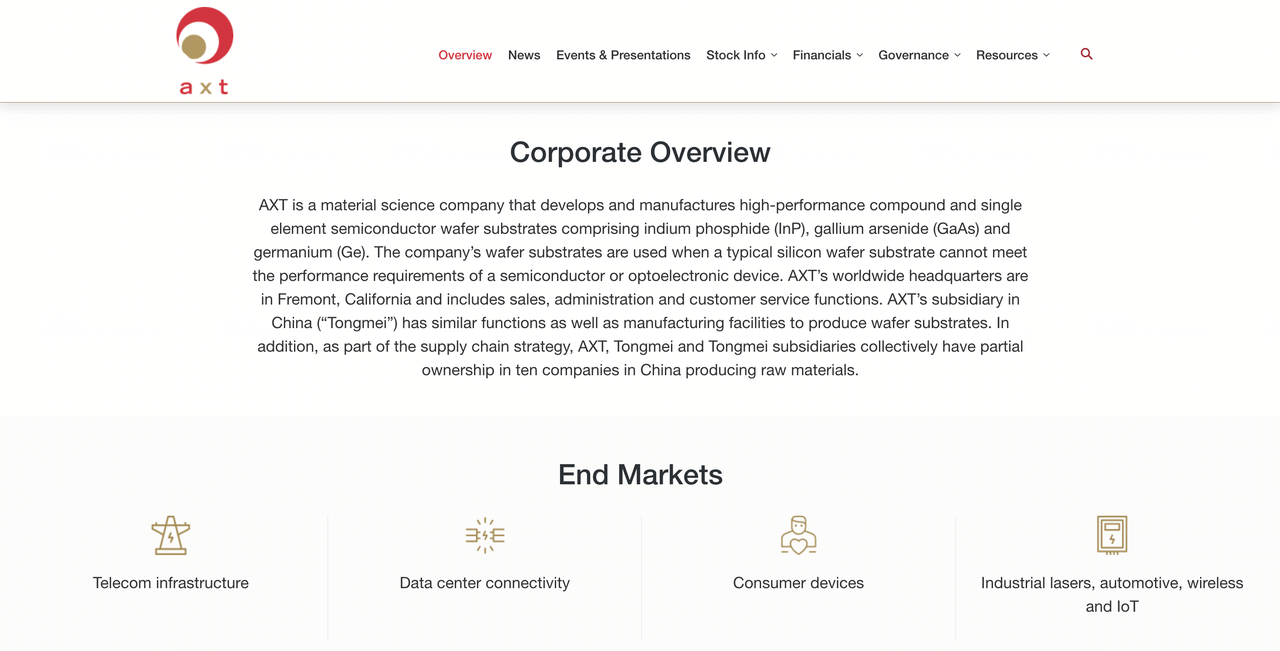

AXT Inc. (Nasdaq: AXTI) is a Fremont, California-based semiconductor materials company founded in 1986. It manufactures high-purity compound and single-element substrate wafers, including indium phosphide (InP), gallium arsenide (GaAs), and germanium (Ge). These materials are used in AI data center optical interconnects, 5G communications, solar cells, lidar, medical imaging, and other advanced electronics applications.

AXT’s main manufacturing operations are conducted through Beijing Tongmei Xtal Technology Co., Ltd., its majority-owned subsidiary in China. The company’s competitive advantage comes from its vertical gradient freeze (VGF) crystal growth technology, in-house crystal growth furnace design, and raw material integration through Jinmei, which refines high-purity indium for InP production.

In 2026, AXT’s biggest growth driver is indium phosphide substrates for optical transceiver components. InP is used in laser diodes and photodetectors inside 800G and 1.6T optical transceivers, which help transmit data across AI data center networks. As AI infrastructure expands, demand for high-speed optical connectivity is rising quickly, creating a supply opportunity for companies with the scale and technical expertise to produce high-quality InP substrates.

Read More: Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

AXT's Performance in Early 2026: From Export Headwinds to Profitability Inflection

AXT entered 2026 after a difficult end to 2025. In January, the company lowered Q4 2025 revenue guidance to $22.5 million to $23.5 million, citing fewer-than-expected export permits for indium phosphide from China’s Ministry of Commerce. Because AXT manufactures mainly in China while selling InP substrates to customers in Europe, the U.S., and other overseas markets, export permit timing remains a recurring risk for revenue visibility.

Q1 2026 marked a sharp turnaround. Revenue reached $26.9 million, beating consensus, while InP accounted for more than 50% of revenue for the first time. Non-GAAP gross margin expanded to 29.9%, and net loss narrowed 81% year over year to $1.6 million. The company also reported a record InP backlog of $100 million and guided for Q2 profitability, signaling a potential shift from recovery to earnings expansion.

Geographic mix is still important to watch. Asia Pacific accounted for 78% of Q1 revenue, Europe 21%, and North America just 1%, with U.S.-bound shipments still affected by export permit constraints. With the $632.5 million equity raise and Tongmei expansion targeting about $280 million in annualized capacity by the end of 2027, AXT is positioned for multi-year growth if demand remains strong and export approvals stay manageable.

Read More: Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

AXT’s 2026 Trading Strategy: Capacity Ramp and Export Permits Drive the Setup

AXT’s 2026 setup depends on three key signals: whether Tongmei can scale InP capacity as planned, whether China export permits normalize enough to support overseas shipments, and whether the Tongmei STAR Market listing makes progress after repeated delays.

- Watch the $65 to $80 Support Zone: After reaching an all-time high of $96.00 on May 1, 2026, AXTI pulled back following the $632.5 million equity offering. The $65 to $80 range is now the key post-offering consolidation zone. A hold above $75 heading into Q2 earnings would support a potential retest of the high, while a break below $60 could revive concerns about dilution, export permits, and capacity execution.

- Capacity Upside vs. Export Permit Risk: The bull case values AXT as a key InP substrate supplier for AI optical networking, with management targeting roughly $280 million in annualized capacity by the end of 2027. The risk is that backlog does not automatically become revenue if export permit approvals slow shipments, especially to North America. Q2 earnings will be the next checkpoint for profitability guidance of $0.06 to $0.08 EPS and updated capacity ramp commentary.

- Monitor Tongmei and Short-Report Volatility: A mid-2026 short-seller report triggered a 35% single-session drop, showing how sensitive AXTI is to any news tied to Tongmei’s STAR Market listing. A successful listing could be a major positive catalyst, while further delays or setbacks could pressure the part of the valuation tied to Tongmei optionality.

Read More: Top AI Hyperscaler Stocks to Watch in 2026: The $700 Billion Cloud Infrastructure Race

The AXT 2026 Forecast: $120+ Capacity Ramp Upside vs. $45 Export Risk Floor

AXT’s 2026 outlook depends on whether Tongmei can execute the InP capacity ramp, whether export permits allow the $100 million backlog to convert into shipped revenue, and whether margins improve enough to support the stock’s AI optical infrastructure re-rating.

The Bull Case: Capacity Ramp and Tongmei IPO Push AXTI Above $120

The bull case requires Tongmei to reach its targeted $35 million quarterly capacity exit rate by the end of 2026, export permits to normalize, and Q2 through Q4 results to confirm the profitability trajectory. If the InP backlog converts into revenue as planned, 2026 revenue could approach $130 million to $140 million. A successful Tongmei STAR Market listing would add another upside catalyst that is not fully reflected in current analyst models.

The Base Case: Profitability and Backlog Conversion Keep AXTI Between $70 and $100

The base case assumes steady execution without a major new re-rating catalyst. Tongmei begins the capacity ramp, AXT delivers Q2 EPS of $0.06 to $0.08, and export permits remain sufficient to support sequential revenue growth. In this scenario, AXTI could consolidate between $70 and $100 as investors wait for Q3 results and clearer evidence that the 2027 capacity target remains on track.

The Bear Case:Export Permit Delays or Tongmei Setbacks Pull AXTI Toward $45

The bear case is driven by export permit delays, slower backlog conversion, Tongmei listing setbacks, or capacity expansion issues. If the market shifts back to valuing AXT on its current revenue base rather than its future capacity roadmap, AXTI could fall toward the $45 to $50 range. The mid-2026 short-seller report and 35% single-session drop show how quickly downside volatility can appear when Tongmei or permit risk returns to the center of the story.

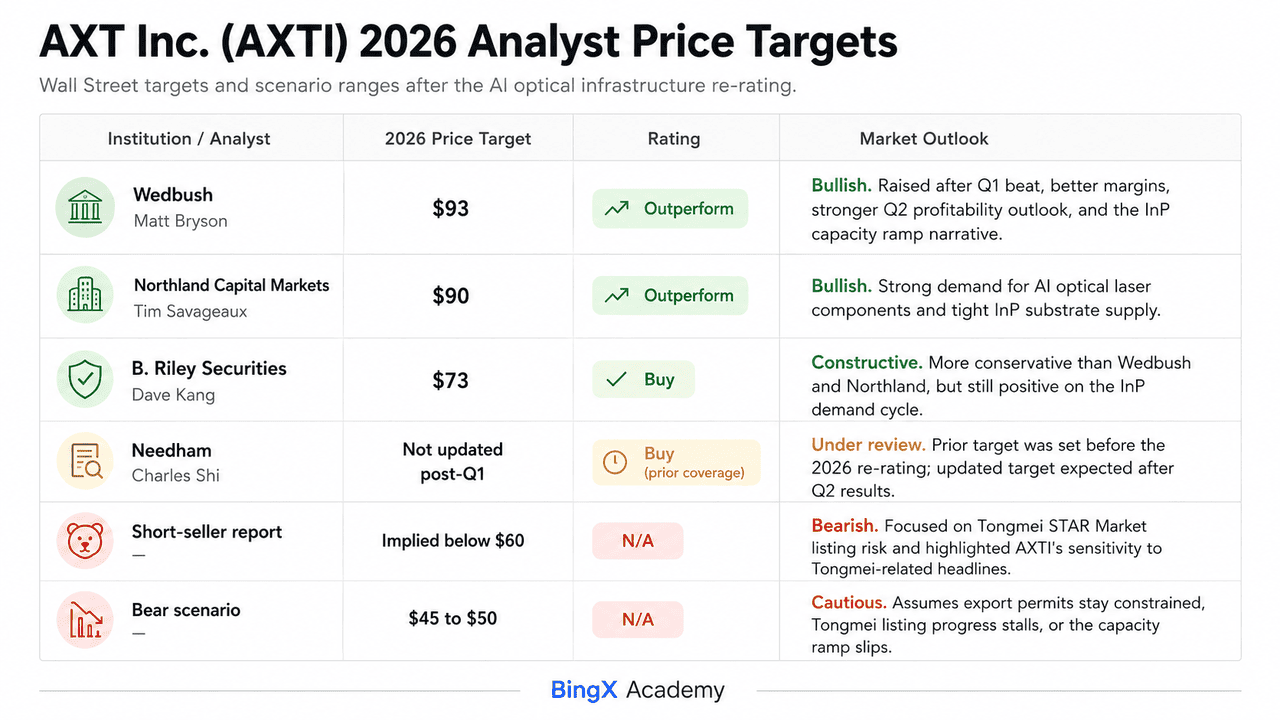

AXT Inc. Price Forecasts for 2026 by Wall Street Analysts

|

Institution / Analyst |

2026 Price Target |

Rating |

Market Outlook |

|

Wedbush / Matt Bryson |

$93 |

Outperform |

Bullish. Wedbush raised its target after AXT’s Q1 beat, stronger margin outlook, Q2 profitability guidance, and InP capacity ramp. The target was lifted several times in 2026, reflecting a major re-rating of AXTI’s AI optical infrastructure exposure. |

|

Northland Capital Markets / Tim Savageaux |

$90 |

Outperform |

Bullish. Northland cited strong demand for AI optical laser components and tight InP substrate supply. Its target was raised sharply from earlier levels as the capacity expansion story gained traction. |

|

B. Riley Securities / Dave Kang |

$73 |

Buy |

Constructive. B. Riley maintained a Buy rating and raised its target modestly after Q1 earnings. Its outlook is more conservative than Wedbush and Northland, but still supports the InP demand cycle. |

|

Needham / Charles Shi |

Not updated post-Q1 |

Buy prior coverage |

Under review. Needham’s prior $5 target was set before AXTI’s 2026 re-rating. An updated target may follow Q2 results, given the scale of the company’s backlog, capacity ramp, and profitability inflection. |

|

Short-seller report |

Implied below $60 |

N/A |

Bearish. The report focused on Tongmei STAR Market listing risk and triggered a sharp one-day decline, highlighting AXTI’s sensitivity to Tongmei-related headlines. |

|

Bear scenario |

$45 to $50 |

N/A |

Cautious. This scenario assumes export permits remain constrained, Tongmei listing progress stalls, or the capacity ramp slips into 2028, pushing the stock back toward a valuation based on current revenue rather than future capacity. |

How to Trade AXT Inc. (AXTI) Stock Futures on BingX TradFi

As AXT navigates the most consequential capacity expansion in its history alongside persistent export permit volatility and a Tongmei STAR Market listing that could be either a transformational positive or a prolonged overhang, tactical traders can capitalize on its exceptionally sharp bidirectional moves through the BingX TradFi platform.

Step 1: Access BingX TradFi. Sign up and navigate to the specialized TradFi section on the main BingX exchange dashboard.

Step 2: Select AXT Inc. (AXTI). Search for and select the AXTI-USDT perpetual futures contract.

Step 3: Choose your direction. Select Open Long if you expect AXT to confirm Q2 profitability, convert more of its InP backlog into revenue, and keep the Tongmei capacity ramp on track. Select Open Short if you expect export permit delays, Tongmei listing setbacks, dilution concerns, or valuation pressure after AXTI’s sharp 2026 rally.

Step 4: Select leverage and margin mode. Choose Isolated or Cross-Margin based on your risk tolerance. Because AXTI has already shown sharp single-day moves in 2026, conservative leverage and clear position sizing are important.

Step 5: Execute strict risk protocols. Set Take-Profit and Stop-Loss (TP/SL) levels before or immediately after entering the trade. AXTI can react quickly to earnings, China export permit updates, Tongmei listing news, optical transceiver supply chain commentary, and short-seller headlines.

Top 5 Risks to Consider Before Investing in AXT Inc. Stock

AXT has one of the strongest AI materials narratives in semiconductors, but AXTI also carries major risks tied to export permits, Tongmei execution, dilution, geographic concentration, and substrate cycle volatility.

- Export permit timing remains the biggest near-term risk: AXT manufactures indium phosphide substrates in China and needs export permits before shipping to overseas customers. Even with a record $100 million InP backlog, slower permit approvals could delay revenue conversion and pressure quarterly results.

- Tongmei STAR Market listing risk could affect valuation: Part of AXTI’s re-rating reflects the potential value of Beijing Tongmei listing on Shanghai’s STAR Market. If the listing is delayed, suspended, or cancelled, the stock could lose part of the premium tied to that optionality.

- Revenue remains highly concentrated in Asia Pacific: Asia Pacific accounted for 78% of AXT’s Q1 2026 revenue, while North America represented only 1% due to export permit constraints. This leaves AXT highly exposed to Asian optical transceiver supply chains and limits its ability to capture U.S. demand.

- The $632.5 million equity raise created dilution risk: AXT’s April 2026 equity offering funded its InP capacity expansion, but also diluted existing shareholders. If the Tongmei buildout is delayed or demand softens, the higher share count could weigh on per-share earnings.

- Compound semiconductor demand cycles can be volatile: AXT’s business has historically been cyclical. AI data center demand supports the current InP cycle, but slower hyperscaler spending, architecture shifts, or new substrate supply could pressure demand and trigger a fast re-rating.

Final Thoughts: Is AXT Inc. Stock a Buy in 2026?

As of June 2026, AXT Inc. (AXTI) has become one of the most closely watched semiconductor materials stocks, driven by a real shift in demand rather than narrative alone. Its record $100 million InP backlog, 39% year-over-year Q1 revenue growth, Q2 profitability guidance, and $632.5 million capacity raise all point to a company at a major inflection point. AXT’s vertical integration, from indium feedstock to proprietary furnace design and finished substrates, also gives it a manufacturing advantage that is difficult to replicate quickly.

The risk is valuation and execution. After a 600%+ year-to-date rally, AXTI is already pricing in strong export permit progress, Tongmei capacity execution, STAR Market listing optionality, and sustained AI optical transceiver demand. Any disappointment could trigger sharp downside, as shown by the 35% single-session drop after a mid-2026 short-seller report. For traders, AXTI futures on BingX TradFi offer a high-volatility way to trade earnings, export permit updates, and Tongmei-related news. For longer-term investors, the key question is whether AXT can fill its planned $280 million annualized capacity by the end of 2027 with real, backlog-backed demand.

Related Reading

- Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

- Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure

- Top 10 AI Hardware Stocks to Watch in 2026: The Architecture Driving Next-Gen Intelligence

- What Is the U.S. CHIPS and Science Act? Its Impact on Semiconductors, Technology, and Crypto in 2026