In early 2026, Firefly Aerospace (FLY) decoupled from traditional aerospace volatility. While broader commercial markets fluctuate, Firefly's focus on regulated, high-value defense and government verticals has delivered consistent revenue growth and an expanding contract backlog. As of mid-2026, the narrative centers on responsive launch recovery, lunar mission expansion, and technological leverage.

Firefly enters 2026 with solid structural tailwinds. The executive team continues to emphasize vertical depth, global launch reach, and platform scalability, projecting sustained commercial growth and meaningful technological expansion. With strong government client retention and new deep-space penetration, 2026 shapes up as a pivotal year.

This guide breaks down the Firefly Aerospace stock price prediction for 2026 using data from analysts and consensus estimates. You will also discover how to gain exposure to Firefly Aerospace (FLY) stock futures through BingX TradFi.

Key Highlights: Top 5 Things for Firefly Investors to Know in 2026

- Launch Vehicle and Spacecraft Strength: Space exploration and defense contracts remain the largest segments, with strong validation from landmark NASA and Space Force missions. Firefly Aerospace has secured a $75 million subcontract from NASA's Jet Propulsion Laboratory in May 2026.

- Capital Infrastructure Expansion: Production footprints have scaled significantly, expanding cleanrooms and innovation labs to approach rapid-response execution milestones. The company will deliver four drones to the Moon's south pole for the MoonFall mission, targeted for launch in 2028.

- Revenue Momentum: Full-year 2025 revenue outperformed expectations, reaching $159.9 million, up 163% YoY, with management guiding 2026 revenue to a massive $420 million–$450 million.

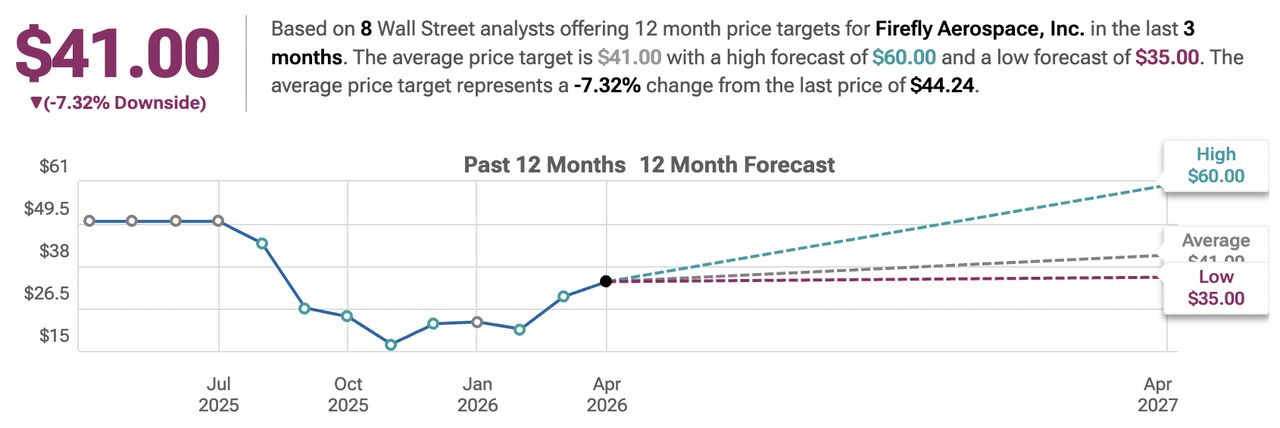

- Polarized Targets: Analyst forecasts for 2026 feature a significant spread, ranging from cautious bearish consolidation targets to highly optimistic bullish expectations of $45 to $50+.

- Valuation Debate: The market continues to balance Firefly's near-term development losses against exponential revenue growth, its massive multi-year backlog, and its unique public space play status.

What Is Firefly Aerospace (FLY)?

Source: Firefly Aerospace Stock on Google

Firefly Aerospace is a global space technology company specializing in launch vehicles, lunar landers, and orbital spacecraft services.It serves major verticals including national security, civil space agencies (like NASA), and commercial satellite operators.In 2026, it is increasingly viewed as a high-growth space infrastructure platform with deep technological expertise.

Its core value lies in simplifying complex orbital deliveries, reducing launch friction, and providing rapid-response space services. Unlike traditional defense contractors or purely pre-revenue space startups, Firefly's ecosystem includes proprietary flight-proven launch systems, robust compliance infrastructure, and long-term infrastructure contracts with sovereign entities.

Firefly's Strategic Evolution (2017–2026): From Launch Vehicle Provider to Global Space Platform

Founded in its current iteration in 2017, Firefly's history features focused mission diversification. Early success in small-to-medium launch vehicle architecture led to spacecraft services and lunar landing diversification. A successful public listing marked mainstream entry. Recent years have focused on launch pad scalability, spacecraft payload integration, and strategic acquisitions. From small-satellite roots to multi-mission space infrastructure leadership, Firefly has consistently built deep domain expertise.

Firefly's Key Growth Phases Over the Years: From Launch to Multi-Vertical Space Leader

Firefly's journey spans distinct eras:

- The Launch Vehicle Phase (2017–2021): Building leadership in medium-class responsive rocketry and foundational propulsion.

- The Diversification Era (2022–2025): Expanding into lunar exploration landers, orbital transfer vehicles, and deep defense integrations (including the milestone acquisition of SciTec).

- The Infrastructure & Production Era (2026+): Scaling automated spacecraft production lines, executing recurring lunar missions, and driving multi-vertical segment revenue.

Firefly (FLY) 2025 Performance Overview: The Infrastructure Scale Year

In 2025, Firefly Aerospace experienced strong acceleration as adoption of its launch vehicles and spacecraft services expanded rapidly amid surging national security demands and growing commercial satellite constellations.

The company's defense segment provided consistent stability and long-term backlog security, while lunar and orbital transport segments delivered significant growth through expanded mission awards and deep system integrations. This powerful combination of factors propelled Firefly to record financial results, solidifying its position as a leading specialized end-to-end space infrastructure provider and driving meaningful shareholder value throughout the year.

FLY Stock Navigation, Market Cap Solidifies Near $7.4 Billion

Firefly's stock exhibited notable volatility during 2025 and early 2026, finding a solid baseline as consistent contract wins and revenue scaling balanced cap-ex requirements. By mid-2026, Firefly maintained robust momentum, with its market capitalization stabilizing around $7.45 billion, underscoring the market's ongoing evaluation of Firefly as a scalable, diversified aerospace leader rather than a niche commercial launcher.

Financial Performance: Revenue Hits $159.9 Million, Up 163% YoY

Firefly delivered exceptional top-line growth in 2025, with full-year revenue climbing 163% year-over-year to $159.9 million.The fourth quarter alone generated $57.7 million in revenue, representing a massive surge from prior periods.This momentum carried powerfully into 2026, with trailing twelve-month revenue hitting $185 million as the company officially guided full-year 2026 targets to a highly ambitious $420 million–$450 million range.

Launch Services and Lunar Spacecraft Surge

The spacecraft services and responsive launch divisions became primary growth engines for Firefly in 2025. The company achieved historic milestones, notably with its Blue Ghost Mission 1 operations on the lunar surface.Civil and national defense clients accelerated program deployments, leading to a record multi-billion dollar backlog and improved pricing leverage across next-generation orbital platforms like Elytra and Eclipse.

Strategic Milestones: Footprint Enhancements Drive Production Scaling

Firefly made significant progress in operational efficiency, launching upgraded automated assembly systems, expanding its Texas headquarters, and building larger cleanroom environments.This culminated in completing the high-value acquisition of national security software firm SciTec, integrating advanced AI-powered data services into their defense portfolio. Furthermore, the company shored up its balance sheet via a strategic follow-on common stock offering at $48 per share to fully fund its expanding payload manufacturing pipeline.

The Firefly Aerospace Thesis for 2026: 5 Pillars of FLY Stock Valuation

Source: Tipranks

While launch services continue to serve as a reliable foundation, Firefly's valuation in 2026 increasingly reflects its evolution into a diversified, multi-mission space technology platform with strong growth across defense and commercial sectors.

1. Civil and Defense Sector Leadership: The Core Pillar

Firefly maintains a premier tier position in responsive space and sovereign defense support.With government mission pipelines expected to scale higher, this vertical delivers stable multi-year backlogs and highly predictable long-term funding lines.

2. Spacecraft Infrastructure & Deep-Space Expansion: The Growth Pillar

Lunar cargo services and advanced orbital transport solutions are positioned for accelerated operational loops in 2026. New subcontract wins, such as JPL's $75 million MoonFall contract to deliver lunar drones, drive outsized pipeline valuations.

3. Integrated AI and Software Moat: The Technology Pillar

Proprietary flight controls, integrated software systems from SciTec, and high-performance automated assembly lines enable efficient spacecraft scaling, supporting rapid deployment iterations.

4. Backlog Realization: The Profitability Pillar

The rapid conversion of signed government contracts into physical launches and orbiter deliveries is expected to drive further operating leverage, creating an inflection point for future corporate earnings.

5. High-Barrier Regulatory and Security Moat: The Defensive Pillar

Deep mission flight heritage, long-term launch pad site leases, and complex structural defense certifications create extremely high barriers to entry for newcomers while ensuring revenue durability.

Read more: Ondo Global Markets vs. xStocks: Which Tokenized Stock Platform Is Better in 2026?

Firefly Aerospace Price Forecasts for 2026: Bull vs. Bear Outlook

Institutional views on Firefly Aerospace stock remain highly active, reflecting massive long-term upside against execution and capital burn profiles.

|

Institution / Analyst |

2026 Price Target |

Market Outlook |

|

Goldman Sachs |

$55 to $60 |

Bullish: Multi-mission launch acceleration and SciTec software synergies drive upside. |

|

Morgan Stanley |

$52 |

Bullish: Overweight rating based on defense responsive launch wins and lunar backlog scaling. |

|

Market Consensus (Aggregated) |

$42 to $45 |

Moderate Buy: Balanced view on rapid top-line growth against capital-intensive cycles. |

|

JPMorgan |

$40 |

Neutral: Stable hold rating tracking near-term execution timelines. |

|

Bearish Outlooks (Various low-end) |

$30 to $35 |

Pessimistic: Focus on near-term development losses and global defense spending pacing. |

Source: Aggregated from MarketBeat, TipRanks, Zacks, Yahoo Finance, and analyst reports (as of mid-2026)

The range from bullish targets above $55 to bearish consolidation models near $30 captures the market's ongoing assessment of capital expenditure cycles versus raw backlog growth.

The Bull Case: Aerospace Expansion Drives FLY Stock Price Above $55

Bulls focus on rapid contract monetization, explosive top-line revenue guidance scaling toward $450 million, and deep integration of space data software.If Firefly maintains its triple-digit growth velocity, successfully scales its Blue Ghost and Elytra mission timelines, and maximizes cash efficiency from its latest equity offering, the stock could achieve aggressive multiple expansions toward $55 or higher by year-end 2026.

The Bear Case: The Correction to $35 or Lower

Bears focus on structural cash burn and execution risk within highly technical environments.If spacecraft assembly pipelines encounter material delays, or if public equity dilution dynamics pressure near-term sentiment, multiples could consolidate, forcing the price floor back toward the $30 to $35 range.

How to Trade Firefly Aerospace (FLY) on BingX

FLY stock perpetuals on the futures market

For active traders looking to capitalize on high-volatility events like earnings reports, BingX TradFi offers advanced margin trading.

- Go to the BingX TradFi section and select Stock Futures.

- Locate the FLY/USDT perpetual contract.

- Choose your Margin Mode (Isolated or Cross) and set your Leverage (typically 2x–5x is recommended for equities).

- Analyze the trend and select Open Long if you expect a price increase or Open Short to profit from a decline.

- Set your Take-Profit (TP) and Stop-Loss (SL) levels immediately to manage risk against 2026's aggressive price swings.

Read more: What are Circle Tokenized Stocks CRCLX (xStocks) and CRCLON (Ondo) and How to Invest?

5 Critical Risks to Watch for Firefly Investors in 2026

While Firefly offers substantial upside through its specialized space and defense platform, investors face capital-intensive, technical, and regulatory challenges.

- Capital Expenditure and Near-Term Cash Burn: Space infrastructure development requires substantial upfront capital. Firefly's continuous engineering investments into next-generation launch and landing lines generate near-term operating losses.If revenue recognition outpaces capital usage less efficiently than expected, additional financing could dilute existing stock values.

- High Technical and Mission Failure Risks: Rocket launches, orbital vehicle dockings, and deep-space lunar operations carry high engineering failure margins. Any unexpected launch anomalies or lost spacecraft payloads during key public missions could trigger immediate structural revisions, slow operational timelines, and dent customer sentiment.

- Concentration in Sovereign and Defense Budgets: A significant portion of Firefly's multi-year backlog depends on allocations from civil entities like NASA and defense vehicles like the U.S. Space Force. Changes in national security initiatives, shifting legislative space targets, or defense budget freezes could alter contract fulfillment timelines.

- Supply Chain and Global Subcontractor Dependencies: Building specialized space vehicles utilizes highly complex global hardware supply chains. Delays in high-grade component manufacturing, precision material bottlenecks, or logistical delivery disruptions could ripple through production phases, slowing vehicle rollouts.

- Shifting Aerospace Regulatory Frameworks: Operating in sensitive defense and aerospace domains binds Firefly to stringent international trade, space deployment licensing, and tracking standards. Evolving compliance adjustments or localized regulatory review delays could prolong necessary mission launch clearances.

Read more: Ondo Global Markets vs. xStocks: Which Tokenized Stock Platform Is Better in 2026?

Conclusion: Should You Invest in Firefly Aerospace (FLY) Stock in 2026?

Deciding whether to invest in Firefly Aerospace in 2026 requires viewing it as a high-conviction play on modern space and defense infrastructure rather than a legacy industrial asset. For growth-oriented investors, the triple-digit 2025 revenue expansion, a massive $400M+ forward revenue guidance, and premier mission selections like the $75 million MoonFall subcontract support a powerful infrastructure growth narrative.

At the same time, the stock's market pricing around $46 reminds investors that capital expenditure cycles and deep-space missions introduce natural volatility. Successful pipeline execution and smooth manufacturing expansion across its Texas facilities will dictate whether the stock breaks confidently out past institutional targets of $55+, or consolidates lower if production timelines extend. Monitor quarterly contract conversions, launch success rates, and spacecraft delivery metrics as core indicators.

Risk Reminder: Trading and investing in equities like FLY involves substantial risk of capital loss. Firefly's growth exposure, capital-intensive milestones, and sensitive defense positioning make it a high-risk asset. Investors should conduct thorough independent research and consider professional financial advice before allocating capital.

Related Reading

- What Are Tokenized Stocks On-Chain, Could They Be the Next Big Trend?

- Ondo Global Markets Unlocks 100+ Tokenized U.S. Stocks on Ethereum - All You Need to Know

- Ondo Global Markets vs. xStocks: Which Tokenized Stock Platform Is Better in 2026?

- Tesla (TSLA) Stock Outlook for 2026: Can the Great AI and Robotaxi Pivot Take TSLA Stock to $600?

- How to Buy Google Stock in 2026: A Guide for TradFi and Crypto Investors

- Reddit (RDDT) Price Outlook for 2026: Can AI Data Licensing Drive RDDT Back to $200?