International Business Machines (IBM) entered mid-July 2026 after one of the sharpest sell-offs in its history. On July 14, the company reported preliminary second-quarter revenue of $17.2 billion and operating EPS of $2.93, both below expectations. IBM shares fell about 25% in one session, their worst day since 1968, dropping toward $211 only six weeks after reaching an all-time high of $332.46.

The results pointed to execution and timing issues rather than a broad demand collapse. Software still grew 5%, Consulting remained stable, and operating pre-tax margin expanded. Most of the weakness came from Infrastructure, where revenue fell 7% as the z17 mainframe cycle faced a difficult comparison and several large deals failed to close on schedule.

The IBM stock forecast for 2026 now centers on two competing views:

- The recovery case: Bulls expect delayed deals, enterprise AI demand, and hybrid-cloud growth to support a rebound, with analyst targets ranging as high as $375.

- The structural-risk case: Bears see enterprise budgets shifting toward AI hardware and away from traditional consulting and software services.

This guide breaks down the IBM stock forecast, 2026 price scenarios, key risks, and how to trade IBM stock futures on BingX TradFi with USDT collateral.

Top 5 Things for IBM Investors to Know in July 2026

- Q2 revenue of $17.2 billion grew only 1%: The figure landed roughly $660 million below the LSEG consensus of $17.86 billion, with GAAP diluted EPS of $2.27, down 2%, and operating EPS of $2.93 against about $3.01 expected.

- The stock fell 25% in one session, its worst since 1968: The July 14 drop wiped out roughly $67 billion in market value and took IBM from an all-time high of $332.46 on June 2 to near the $212.34 52-week low within six weeks.

- Infrastructure fell 7% as clients bought memory instead: Management pointed to a late-June capex reprioritization toward supply-constrained servers, storage and memory, which hit IBM Z and the associated Transaction Processing software stack.

- Analysts split rather than capitulated: HSBC cut to Reduce with a $191 target while Oppenheimer downgraded to Perform, yet Morgan Stanley raised to $293 and BofA kept a Buy at a trimmed $280, leaving a consensus near $299 against a $375 Street high from Citigroup.

- The quantum and Lightwell commitments were reaffirmed: IBM confirmed more than $10 billion of quantum investment over five years, a letter of intent for the Anderon quantum wafer foundry backed by $1 billion in CHIPS incentives plus $1 billion of IBM cash, and the July 8 general availability of Lightwell, a $5 billion open source security initiative.

What Is International Business Machines (IBM)?

International Business Machines Corporation, incorporated in 1911, is a global provider of hybrid cloud, artificial intelligence and consulting expertise. It operates in more than 175 countries with roughly 287,000 employees and counts 95% of Fortune 500 companies among its clients. Following the 2021 Kyndryl spin-off, IBM repositioned itself away from legacy managed infrastructure and toward a higher-margin software and services mix.

The company reports through four segments: Software, Consulting, Infrastructure and Financing. Software is the profit engine, contributing roughly 45% of revenue and, by J.P. Morgan estimates, close to two-thirds of profit, anchored by Red Hat OpenShift at a $2 billion annual recurring revenue run rate and software ARR of roughly $25 billion growing 10%. Consulting delivers AI implementation and modernization work. Infrastructure houses the IBM Z mainframe franchise, whose z17 program remains at nearly 130% program-to-program against z16, IBM's previous record. Under CEO Arvind Krishna, recent capital allocation has favored data and automation, with HashiCorp closing in February 2025 and Confluent closing in March 2026 for roughly $11.6 billion.

IBM (IBM) Q2 2026 Earnings: What Caused the Revenue Miss and 25% Stock Drop?

- The z17 cycle created a difficult comparison. Infrastructure revenue fell 7% as IBM Z moved past its launch period, creating a tougher year-over-year base.

- Clients redirected late-quarter spending toward scarce hardware. Rising memory prices and constrained server and storage supply led some customers to prioritize hardware purchases, delaying software renewals and consulting projects.

- Several large contracts missed the quarter-end deadline. Management said major deals remained in the pipeline but did not close when expected, increasing the size of the revenue shortfall.

- Transaction Processing weakened alongside IBM Z. The Infrastructure slowdown also affected related software revenue, showing how IBM’s mainframe hardware and software businesses remain closely connected.

- Margins held up despite weaker revenue. Operating pre-tax margin expanded 30 basis points to 19.2%, and operating EPS still rose 5%, suggesting execution and deal timing caused more damage than rising costs.

IBM Corporation Q2 2026 Financial and Consensus Profile: Revenue, EPS and Margins

IBM's preliminary Q2 print showed a company holding its profitability while losing its growth narrative. Revenue rose 1% against expectations for a mid-single-digit result, and the gap between the Q1 trajectory and the Q2 outcome is what triggered the de-rating rather than the absolute miss. Final results and full-year guidance are due on the July 22 conference call.

|

Financial Metric |

Consensus Estimate |

Reported / Preliminary |

Surprise |

|

Q2 2026 Revenue |

~$17.86 billion |

$17.2 billion |

Missed by ~$660 million; grew only 1% |

|

Q2 2026 Operating EPS |

~$3.01 |

$2.93 |

Missed; still up 5% year over year |

|

Q2 2026 GAAP EPS |

— |

$2.27 |

Down 2% year over year |

|

Q2 2026 Software Revenue |

— |

Up 5% |

Below plan; Red Hat accelerated to 11% |

|

Q2 2026 Consulting Revenue |

— |

Flat |

Up 1% at constant currency |

|

Q2 2026 Infrastructure Revenue |

— |

Down 7% |

Worse than the low-single-digit decline guided |

|

Q2 2026 Operating Pre-Tax Margin |

— |

19.20% |

Up 30 basis points year over year |

|

H1 2026 Free Cash Flow |

— |

$4.8 billion |

From $7.8 billion operating cash flow |

|

FY2026 Free Cash Flow Guidance |

— |

Up ~$1 billion year over year |

Prior guidance; to be updated July 22 |

For context, Q1 2026 was the mirror image. Revenue of $15.9 billion grew about 9% and beat consensus, Software rose 11% to $7.1 billion, Infrastructure rose 15% on IBM Z strength, and operating EPS of $1.91 beat by roughly 5%. IBM had beaten EPS in four consecutive quarters before the warning. Debt stood at $66.4 billion at March 31, up $5.1 billion in the quarter to fund Confluent, and the dividend yields roughly 2.3% backed by a 31st consecutive year of increases.

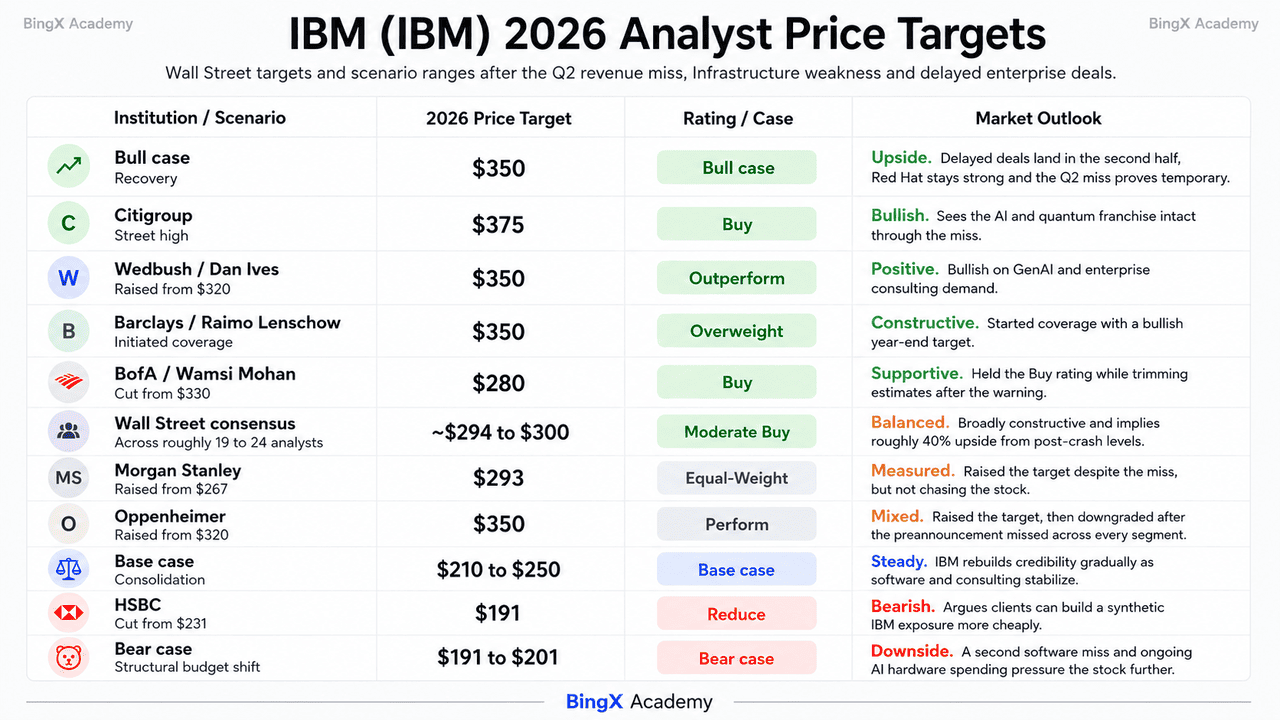

IBM (IBM) 2026 Investment Outlook: $350 Bull Case vs. $191 Bear Case

The remainder of 2026 for IBM is a referendum on one question: whether hyperscaler AI capex is temporarily crowding out enterprise software budget or permanently taking it.

The Bull Case: IBM Recovers Toward $350

The bull case rests on the composition of the miss. Operating margin expanded, operating EPS still grew 5%, Red Hat accelerated to 11%, and Distributed Infrastructure posted its best quarter on record. Red Hat, IBM’s fastest-growing unit, was not identified as a source of weakness. If large deals were delayed rather than lost, they could close in the second half, making Q2 a temporary trough.

This scenario requires memory and server supply pressure to ease so enterprise budgets can rotate back toward watsonx, Red Hat, and Consulting. Wedbush, Barclays, and Oppenheimer have all pointed to targets near $350. IBM’s reaffirmed $10 billion quantum commitment, the Anderon foundry plan, and its 2029 fault-tolerant computing target add long-term upside. With consensus near $299, the post-sell-off price still implies roughly 40% upside.

The Base Case: IBM Consolidates Between $210 and $250

In the base case, IBM avoids another major breakdown but recovers gradually. The July 22 call confirms the preliminary figures, full-year constant-currency growth guidance is trimmed, and free cash flow finishes slightly below the earlier path. The stock spends the second half rebuilding confidence one quarter at a time.

The dividend and cash flow provide support while the valuation remains compressed. IBM’s roughly 2.3% yield, 31-year dividend growth streak, and $4.8 billion of first-half free cash flow help establish a floor. Stable mid-to-high single-digit Software growth and stronger GenAI consulting conversion would support a range between the $212.34 low and the $245 to $255 resistance zone.

The Bear Case: IBM Toward $191 on a Structural Budget Shift

The bear case depends on enterprise budgets continuing to move toward AI hardware and away from IBM’s higher-margin software and consulting businesses. HSBC cut IBM to Reduce with a $191 target, while Oppenheimer downgraded the stock after the preannouncement missed across every segment.

A second quarter of Software deceleration would be the main warning sign. Software generated about 45% of 2025 revenue and close to two-thirds of profit, so weaker organic growth would pressure earnings quickly. Confluent may also account for a large portion of the reported 5% Software growth, suggesting softer underlying momentum. Combined with $66.4 billion of debt and a maturing mainframe cycle, that could push IBM toward $201 and then HSBC’s $191 target.

IBM Stock Price Forecasts for 2026 By Wall Street Analysts

Wall Street did not move in unison after the warning, and that divergence is the clearest available signal that the Street reads this as one distorted quarter rather than a structural break. Ratings run roughly 15 Buy-equivalent, 7 Hold and 1 Sell across about 19 to 24 analysts.

|

Institution |

2026 Price Target |

Rating |

Market Outlook |

|

Citigroup |

$375 |

Buy |

Street high. Sees the AI and quantum franchise intact through the miss. |

|

Oppenheimer |

$350 |

Perform |

Raised the target from $320 on July 14, then downgraded the rating after the preannouncement missed across every segment. |

|

Wedbush / Dan Ives |

$350 |

Outperform |

Bullish. Raised from $320 pre-warning on GenAI and enterprise consulting. |

|

Barclays / Raimo Lenschow |

$350 |

Overweight |

Bullish. Initiated coverage with a year-end target. |

|

Wall Street consensus |

~$294 to $300 |

Moderate Buy |

Broadly constructive. Implies roughly 40% upside from post-crash levels. |

|

Morgan Stanley |

$293 |

Equal-Weight |

Measured. Raised from $267 despite the miss. |

|

BofA / Wamsi Mohan |

$280 |

Buy |

Constructive. Cut from $330 after the preannouncement but held the rating. |

|

HSBC |

$191 |

Reduce |

Bearish. Cut from $231, arguing clients can build a synthetic IBM more cheaply. |

|

Bear scenario |

$191 to $201 |

N/A |

Cautious. Assumes a second software miss and a sustained budget shift to AI hardware. |

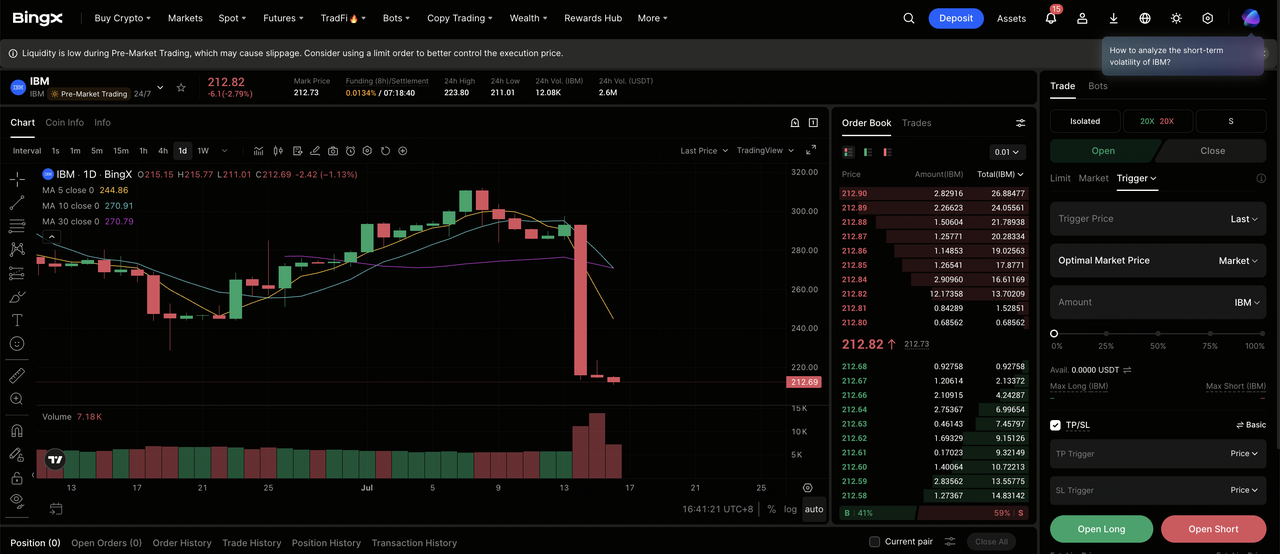

How to Trade IBM Common Stock (IBM) on BingX

Navigate the volatility of IBM's earnings cycle using BingX TradFi and BingX AI tools. With the full Q2 results and updated guidance due on July 22, AI-driven predictive analytics can help you better anticipate market sentiment shifts and price action around the release.

Long or Short IBM Stock Futures on BingX TradFi

Step 1: Access BingX TradFi. Sign up and navigate to the specialized TradFi section on the main BingX exchange dashboard.

Step 2: Select International Business Machines (IBM). Search for and select the IBM-USDT perpetual futures contract.

Step 3: Choose your direction. Select Open Long if you expect the slipped deals to close in the second half, software growth to reaccelerate toward the Q1 pace, and the quantum roadmap to re-rate the stock toward consensus. Select Open Short if you expect enterprise budgets to keep rotating toward AI hardware, a second consecutive software miss, or full-year guidance to be cut on July 22.

Step 4: Select leverage and margin mode. Choose Isolated or Cross-Margin based on your risk tolerance. Because IBM moved 25% in a single session despite a beta near 0.7, conservative leverage and clear position sizing are important.

Step 5: Execute strict risk protocols. Set Take-Profit and Stop-Loss (TP/SL) levels before or immediately after entering the trade. IBM can react quickly to quarterly earnings, memory and server pricing headlines, hyperscaler capex commentary, quantum roadmap milestones, and analyst rating changes.

Top 5 Risks to Watch for IBM Investors in 2026

To navigate the second half of 2026, investors must weigh IBM's intact margin profile and quantum optionality against these five structural and macro headwinds.

- Hyperscaler AI capex is crowding out enterprise software budget: The same dynamic that hit IBM also pushed Oracle down about 33% and Accenture down roughly 49% year to date. If the rotation persists rather than normalizes, IBM's highest-margin revenue is the line most exposed.

- Software carries the profit and it decelerated to 5%: Software delivered roughly 45% of 2025 revenue and close to two-thirds of profit at an 82.8% Q1 gross margin. With Confluent estimated to contribute about $340 million of the quarter, organic growth underneath the reported 5% looks thin.

- July 22 guidance is an unresolved binary: IBM has not yet updated its full-year outlook for more than 5% constant-currency growth or the roughly $1 billion free cash flow improvement. Prediction markets price a high probability of a further miss next quarter.

- The $66.4 billion debt load sits against heavy quantum spending: Debt rose $5.1 billion in Q1 to fund Confluent, and the company has committed more than $10 billion to quantum over five years plus $1 billion of cash toward the Anderon foundry, all at the peak of the rate cycle.

- The mainframe cycle has entered its late stage: Infrastructure declined 7% as z17 lapped its launch, and management had already guided to full-year declines. Any further weakness in IBM Z pulls the attached Transaction Processing software down with it.

Final Thoughts: Should You Invest in IBM in 2026?

IBM after the July 14 warning is a story of an intact franchise with a broken quarter and an unresolved question about whose budget it is competing for. Record margin expansion, 11% Red Hat growth, a best-ever Distributed Infrastructure quarter, and a reaffirmed $10 billion quantum commitment are not in dispute. What is in dispute is whether the enterprise software wallet that funds two-thirds of IBM's profit is being borrowed by AI hardware or taken by it.

The bull case is that slipped deals close, the memory squeeze normalizes, and a stock trading near 23 times forward earnings against a roughly $299 consensus re-rates as the second half proves Q2 was timing. The bear case, articulated by HSBC while most of the Street held its targets, is that clients can now assemble IBM's value from cheaper parts and that the budget shift is permanent. Investors who believe enterprise AI spending eventually rotates back through watsonx, Red Hat and consulting may find the post-crash price the best entry in years. More conservative traders might wait for the July 22 full results and updated guidance before initiating a long-term position, using the $212 to $213 area as the line that defines whether the reset is over.

Risk Reminder: Trading and investing in equities like IBM involves a high risk of capital loss. As July 14 demonstrated, even a low-beta mega-cap can lose a quarter of its value in a single session on a guidance surprise. Conduct independent research before allocating capital.

Related Reading

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

- Palantir (PLTR) Stock Outlook for 2026: Can AI-Driven Enterprise Supercycle Take PLTR to $235+?

- Oracle (ORCL) Stock Price Outlook for 2026: Can AI Cloud Infrastructure Take ORCL Back to Its Highs?

- Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?

- Goldman Sachs (GS) Price Prediction 2026: Record Quarter Momentum or Valuation Ceiling at $1,140?

- Micron Stock Price Prediction 2026: $1,500 AI Supercycle or Peak Margin Cyclical Trap?