In early June 2026, IonQ (NYSE: IONQ) stands at the absolute epicenter of a high-stakes technology arms race. Emerging from a massive May rally fueled by the U.S. government’s $2.013 billion CHIPS Act quantum funding package, IONQ shares are currently trading near $71.40, boasting a vertical market capitalization of roughly $26.5 billion. While the quantum computing narrative has long been dismissed as an unmonetized science experiment, IonQ stunned Wall Street by reporting a staggering 755% year-over-year revenue surge to $64.7 million in its latest quarter, prompting management to raise its full-year 2026 revenue guidance to an unprecedented $260 million to $270 million range.

Yet, beneath this explosive top-line traction lies an aggressive, capital-intensive pivot. By executing a $1.8 billion cash-and-stock acquisition of semiconductor foundry SkyWater Technology, IonQ has fundamentally recast its business model to become the public market’s first vertically integrated quantum hardware pure-play. Investors must now weigh an accelerating $470 million contract backlog against a widening $271.5 million quarterly operating loss and a blistering cash-burn profile.

This guide breaks down the IonQ stock forecast for 2026 using data from SEC filings, Morgan Stanley, Jefferies, and D.A. Davidson.

You will also discover how to trade IONQ stock futures using the advanced trading ecosystem on BingX TradFi.

Top 5 Things for IonQ Investors to Know in 2026

As the quantum computing sector transitions from laboratory promise to industrial-grade infrastructure, traders must monitor these five foundational market-moving factors:

- The Vertical Foundry Pivot: IonQ’s $1.8 billion acquisition of SkyWater Technology transfers absolute ownership of a domestic semiconductor fabrication business in-house. This gives IonQ sovereign control over proprietary chip designs, production timelines, and micro-hardware IP that rivals like IBM, Google, and Rigetti still route through third-party foundries.

- The $470 Million Backlog Anchor: Remaining Performance Obligations (RPO) surged an eye-popping 554% year-over-year to $470 million. This contracted, unbooked revenue pipeline provides long-term commercial visibility, heavily driven by critical defense, cybersecurity, and sovereign computing mandates.

- Deepening Operating Cash Burn: Despite explosive growth, IonQ’s industrial scaleup is highly dilutive in the short term. The company posted a steep quarterly operating loss of $271.5 million and maintains an annual adjusted EBITDA loss outlook of -$310 million to -$330 million, proving that monetization speed is locked in a race against capital consumption.

- The Quantinuum IPO Benchmark: Honeywell’s quantum unit, Quantinuum, is launching an upsized Nasdaq initial public offering targeting up to $1.46 billion at a valuation cap of $14.3 billion. This landmark debut will serve as an immediate public market pricing mechanism and valuation sanity check for IonQ’s $26.5 billion multiple.

- Washington’s Sovereign Tailwinds: The Trump administration's $2 billion CHIPS Act allocation directly targeted the domestic quantum supply chain. Though IonQ was not among the nine immediate direct grant recipients, such as IBM's $1 billion foundry grant, the policy has established quantum computing as an urgent national security priority, driving aggressive institutional accumulation of sector leaders.

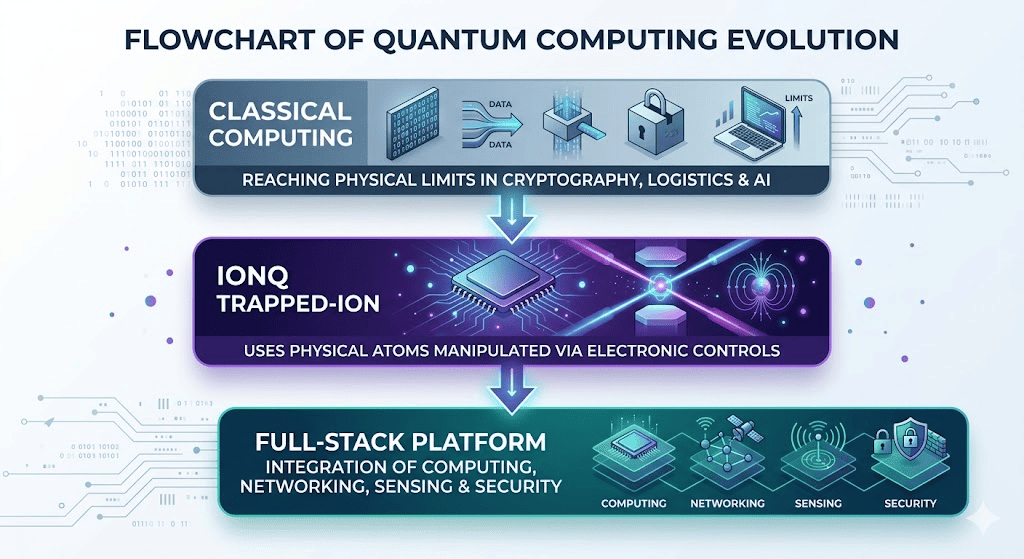

What Is IonQ (IONQ)?

IonQ is a leading pure-play developer of quantum computing hardware and software architecture. Unlike competitors utilizing superconducting circuits like IBM or quantum annealing like D-Wave, IonQ’s core technological edge lies in its trapped-ion architecture. This approach isolates individual, microscopic atoms in electromagnetic fields and manipulates them using high-fidelity electronic controls and lasers. Trapped ions naturally possess exceptionally low error rates and prolonged coherence times, which are essential for scaling accurate quantum computing.

In 2026, IonQ is aggressively transitioning from a hardware provider into a multi-product platform company spanning quantum computing, secure networking, atomic clocks, and post-quantum cryptography. System architectures like its fifth-generation Tempo and upcoming 256-qubit sixth-generation platforms are accessible globally via major cloud ecosystems including Amazon AWS, Microsoft Azure, and Google Cloud.

On the BingX platform, global macro investors track the performance of disruptive tech giants and high-beta infrastructure leaders, managing risk across rapidly changing technological cycles.

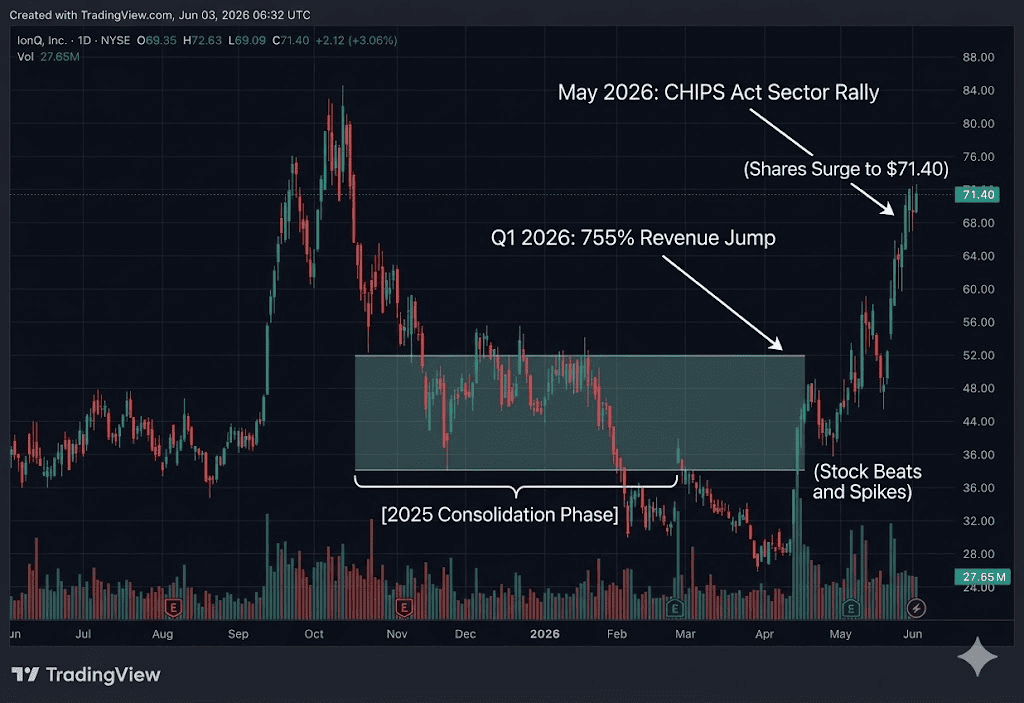

IonQ’s Performance in 2025: Steady Accumulation Before the 2026 Explosion

In 2025, IonQ was a steady but volatile performer, spending much of the year consolidating within a defined trading range after achieving over $100 million in annual GAAP revenue. The market initially treated the equity as a speculative, long-term venture vehicle, keeping the stock anchored below its previous all-time highs while it incurred heavy research and development outlays at its 105,000-square-foot manufacturing plant in Bothell, Washington.

IONQ stock performance in 2025

The narrative shifted aggressively in early 2026. The convergence of commercial contract conversions with federal agencies like DARPA, multi-million dollar commitments from international hubs like QuantumBasel, and the historic SkyWater acquisition sparked an absolute paradigm shift, driving the stock out of its multi-month base directly up to a multi-year peak of $72.63 in late May.

IonQ’s 2026 Strategy: How to Navigate Quantum Valuation Volatility

- The Multi-Product Mix Matrix: Over one-third of IonQ's current revenue is driven by multi-product customers buying across computing, sensing, and networking lines. This cross-selling deepens customer enterprise integration, dramatically increasing switching costs and smoothing out irregular hardware procurement cycles.

- The Price-to-Sales (P/S) Risk Envelope: Trading at a trailing Price-to-Sales multiple exceeding 120x, IonQ is pricing in nearly a decade of flawless technical and financial execution. Traders must treat near-term technical milestones, specifically the sprint to the Algorithmic Qubit (AQ) 64 threshold, as the primary justification for this valuation.

- Monitoring Invalidation Metrics: According to rigid risk frameworks, the primary structural threat to the long-term bullish thesis is capital depletion. If quarterly operating cash usage continuously outpaces new commercial bookings for three consecutive quarters before achieving fault-tolerant computing milestones, the timeline to self-sustained profitability could collapse.

IonQ 2026 Price Prediction: $100 Peak vs. $41 Demand Correction

Estimated 2026 Revenue Pool: $260M−$270M⟺Remaining Performance Obligations: $470M

Investors navigating the current IonQ landscape must separate the long-term structural tailwinds of the emerging quantum economy from the immediate financial realities of pre-profitability stock execution.

The Bull Case: The $100 SkyWater Flywheel

The bullish narrative, backed by targets from Jefferies ($85) and premium buy-side desks hitting the $100 mark, assumes an acceleration of the company's full-stack commercial flywheel. By bringing the SkyWater foundry in-house, IonQ eliminates the supply-chain bottlenecks hampering its peers. Defense departments and global intelligence agencies requiring domestic, hyper-secure hardware pipelines are highly likely to funnel larger contracts exclusively into IonQ’s backlog.

Technically, if IonQ successfully converts its massive $470 million RPO backlog into recognized top-line revenue ahead of schedule, the stock can maintain its elevated growth multiple. A successful market debut of Quantinuum at a multi-billion dollar premium would validate sector valuations, giving IONQ bulls the fundamental momentum needed to squeeze short sellers and clear technical overhead resistance toward the psychologic $100 threshold.

The Base Case: $55 – $70 Consolidation and Margin Assessment

The base case envisions a high-volatility plateau where the stock digests its explosive 80%+ year-to-date run-up and consolidates to allow fundamentals to catch up with the valuation. In this scenario, Wall Street institutions will focus heavily on execution rather than forward rhetoric. While revenue growth is guaranteed to remain above 100% organically for the calendar year, the massive costs associated with integrating a manufacturing foundry mean EBITDA losses will remain pinned above $300 million.

Analysts at Morgan Stanley maintain an Equal Weight rating with a recently revised target of $47, reflecting this balanced perspective. For traders, this creates a sustained trading range. Shares will likely fluctuate between structural support at $55 and major overhead supply at $75, with price action tightly correlated to quarterly updates on the deployment of fifth-generation Tempo systems and technical progress toward the 10,000-qubit long-term roadmap.

The Bear Case: The $41 Speculative Valuation Liquidation Trap

The bearish scenario, warned by conservative analyst profiles and reflected in Zacks' low rank, focuses on a 'sell-the-news' correction driven by severe multiple contraction. At a P/S ratio hovering north of 120x, any localized macro shock, broad tech sector rotation out of speculative growth, or extended timeline to commercial profitability could trigger aggressive institutional de-risking.

Furthermore, because a portion of IonQ’s recent top-line expansion was magnified by corporate acquisition mechanics rather than purely organic hardware sales, the quality of growth could face scrutiny. If upcoming earnings reports reveal a widening free cash flow deficit exceeding $80 million per quarter without an exponential jump in localized enterprise enterprise bookings, a sharp correction could follow. A decisive technical breakdown below the short-term 50-day moving average would confirm this trend, exposing the stock to a rapid mean-reversion pullback toward the $48.60 to $41.90 support zone.

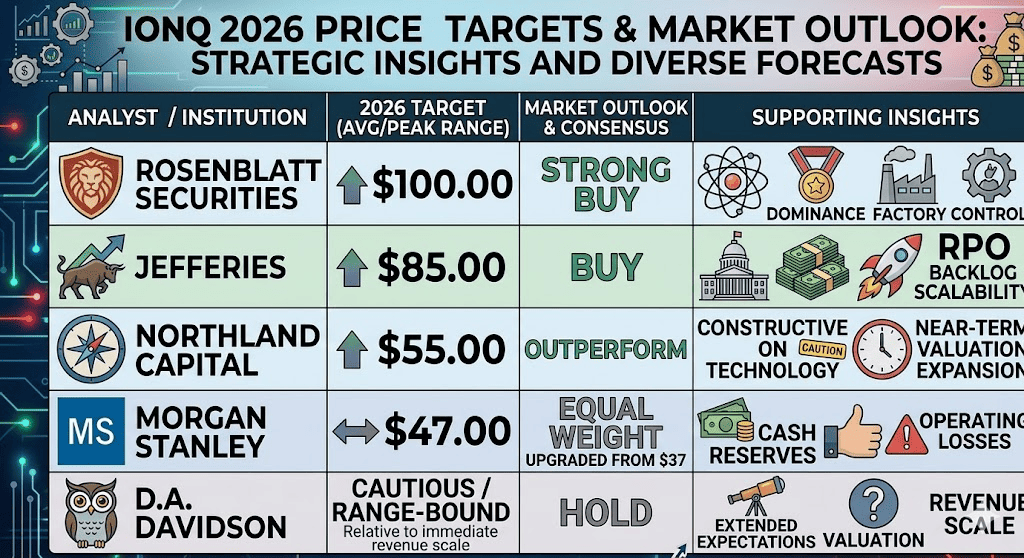

IonQ Price Forecasts for 2026 by Leading Wall Street Analysts

|

Analyst |

2026 Target (Avg/Peak Range) |

Market Outlook & Consensus |

|

Rosenblatt Securities |

$100.00 |

Strong Buy: Cites absolute trapped-ion technology dominance and foundry control. |

|

Jefferies |

$85.00 |

Buy: Points to rapid federal contract monetization and RPO backlog scalability. |

|

Northland Capital |

$55.00 |

Outperform: Constructive on technology but notes near-term valuation expansion. |

|

Morgan Stanley |

$47.00 |

Equal Weight: Upgraded from $37; praises cash reserves but flags sticky operating losses. |

|

D.A. Davidson |

Cautious / Range-Bound |

Hold: Notes market expectations are overly extended relative to immediate revenue scale. |

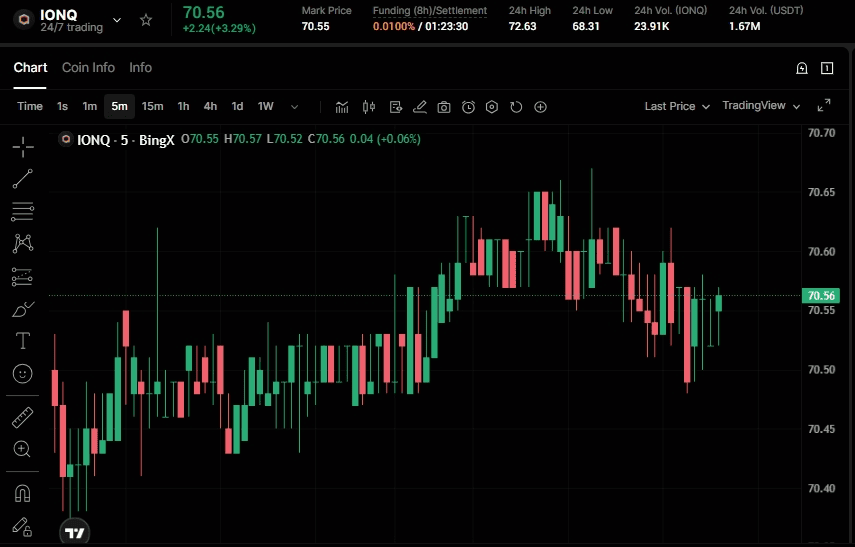

How to Trade IonQ (IONQ) Stock Futures on BingX TradFi

IONQ/USDT perpetual contract on BingX futures market

Position your portfolio for the next phase of the quantum race by leveraging the institutional-grade trading ecosystem on BingX TradFi.

- Access BingX TradFi: Navigate to the TradFi / Stocks section on the BingX platform.

- Select IonQ (IONQ): Choose the IONQ-USDT Perpetual Contract to track the real-time price action of IonQ Inc..

- Choose Your Direction: Select Open Long if you anticipate that the SkyWater foundry integration and defense backlog will accelerate the stock toward $100, or select Open Short if you want to trade the speculative valuation liquidation case down toward the support channels.

- Deploy Strategic Leverage: Select your preferred leverage ratio to optimize capital efficiency on high-beta equity swings, ensuring your position size aligns with your risk tolerance.

- Implement Strict Risk Controls: Utilize BingX’s advanced Take-Profit (TP) and Stop-Loss (SL) tools to automatically shield your trading capital from sudden post-earnings gap moves or overnight macroeconomic headlines.

Top 5 Risks of Investing in IONQ Stock

While IonQ’s vertical full-stack integration creates a compelling technological moat, investors must aggressively manage these five critical structural risks.

- Severe Multiple Contraction: Trading at an extreme price-to-sales multiple north of 120x, the stock carries massive valuation risk. Any broader market rotation out of speculative growth or a macro correction will hit high-multiple equities the hardest.

- Deepening Operational Losses and Dilution: With a quarterly operating loss of $271.5 million and sustained cash burn, IonQ will require heavy, ongoing capital expenditures to scale its physical infrastructure. If revenue conversion lags behind backlog growth, investors face the risk of future equity dilution.

- Foundry Integration Complexity: Absorbing a $1.8 billion semiconductor manufacturing business like SkyWater adds intense operational friction. Balancing foundry utilization between IonQ's internal quantum chip pipelines and external commercial merchant customers introduces significant execution risks.

- Intensifying Sector Competition: IonQ does not operate in a vacuum; larger tech titans like IBM and Google, alongside pure-play rivals like Quantinuum and D-Wave, are investing billions into competing quantum modalities. If a rival achieves definitive fault-tolerance first, IonQ's hardware roadmap could face premature obsolescence.

- The Quantum Winter Threshold: Broad commercial adoption of quantum computing still relies on heavily expanding algorithmic qubits (AQ) and eliminating high hardware error rates. If the technology takes longer than the market expects to transition from government pilots into repeatable enterprise utility, the sector could enter a prolonged cooling phase.

Final Thoughts: Is IonQ a Good Stock to Buy in 2026?

As of June 2026, IonQ has successfully transformed its market identity from an abstract quantum research lab into a vertically integrated, industrial-grade computing stack. At the $71 level, the market is aggressively pricing in its newly established domestic manufacturing moat and undeniable lead in government and defense applications. For technical traders, the $55 zone represents the definitive line in the sand; as long as structural weekly closes remain safely above this threshold, the long-term platform adoption narrative remains the dominant play.

However, the reality of an extreme forward sales multiple means entering positions at current multi-year highs carries a high momentum-risk premium. Shorter-term market participants should look to exploit the stock's high volatility (Beta around 3) by range-trading swings between known support channels, while long-term portfolio builders should wait for orderly post-earnings consolidations before deploying capital into this high-conviction quantum narrative.

Risk Reminder: Trading pioneering technology equities and high-beta growth assets involves significant capital risk due to extreme valuation multiples and extended paths to GAAP profitability. Always deploy strict risk-management and stop-loss protocols to shield capital against sudden shifts in market sentiment.

Related Reading

- What Is the U.S. CHIPS and Science Act? Its Impact on Semiconductors, Technology, and Crypto in 2026

- Firefly Aerospace Stock Outlook 2026: Can Launch Vehicles, Spacecraft Services Drive FLY to $45+?

- Nebius Group (NBIS) Price Prediction 2026: $287 Street-High AI Factory Boom or Stretched Neocloud?

- Top Space Stocks to Buy Ahead of SpaceX IPO

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide