In early July 2026, retail powerhouse Walmart Inc. (NASDAQ: WMT) stands at a defining operational and structural crossroads. Long valued as a mature defensive staple, the global titan is aggressively attempting to transition from an era of low-margin big-box retail into a high-margin, tech-driven omnichannel ecosystem.

In early July 2026, retail powerhouse Walmart Inc. (NASDAQ: WMT) stands at a defining operational and structural crossroads. Long valued as a mature defensive staple, the global titan is aggressively attempting to transition from an era of low-margin big-box retail into a high-margin, tech-driven omnichannel ecosystem.

Following a choppy mid-summer close, Walmart’s shares are currently trading at $111.84, navigating intense market consolidation as investors rotate out of high-beta sectors into blue-chip mega caps. While WMT briefly crossed into the elite $1 trillion market cap club earlier this year, it has corrected roughly 12.3% from its May record highs. The equity sits within a well-defined 52-week structural trading range between a low of $94.23 and a historical peak of $135.16.

Investors are actively balancing an accelerating digital footprint against rich valuation friction. While the company posted solid top-line execution during its recent annual shareholder meeting, localized retail signals have raised high-stakes debates between growth-oriented Wall Street analysts and risk-averse quantitative models.

This comprehensive guide dissects the WMT stock forecast and price prediction for the remainder of 2026, combining proprietary marketplace initiatives with fresh consensus metrics from TD Cowen, RBC Capital, UBS, Piper Sandler, and Simply Wall St.

You can trade WMT stock perpetual futures on BingX TradFi using flexible USDT collateral.

Top 5 Things for Walmart Traders to Know in 2026

As Walmart scales its ecosystem under the operational guidance of Walmart U.S. CEO David Guggina and International chief Chris Nicholas, market participants must closely track these core structural drivers:

- The Digital Profit Engine Pivot: Walmart is engineering a profound structural mix shift. Alternative revenue streams, spanning marketplace operations, last-mile delivery monetizations, Sam's Club memberships, and retail media, now drive roughly one-third of the company's total earnings before interest and taxes (EBIT).

- The $1.4 Billion Vibe.co Acquisition: In late June 2026, Walmart reached an agreement to acquire self-serve connected TV (CTV) advertising platform Vibe.co for an estimated $1.4 billion. The integration into Walmart Connect provides the infrastructure to unlock massive ad budgets from small-to-medium businesses (SMBs).

- The $3 Billion Tariff Refund Buffer: Management has gained visibility into approximately $3 billion in potential regulatory tariff refunds. Rather than claiming this sum immediately, Walmart plans to systematically deploy these funds into high-velocity consumable price rollbacks to aggressively capture low-income grocery market share.

- Affluent Consumer Diversification: Driven by the tech updates to the Walmart+ subscription ecosystem, the retailer has secured a massive market share expansion among households earning over $100,000. Fast delivery fulfillment now handles roughly 35% of digital orders in under three hours.

- The $30 Billion Share Buyback: Demonstrating substantial balance sheet resilience, Walmart’s board has authorized a massive new $30 billion equity repurchase program, providing a powerful structural buffer against macroeconomic downside.

What Is Walmart Inc. (WMT)?

Founded in 1962 by Sam Walton, Walmart has grown into the world's largest brick-and-mortar retailer, operating more than 10,800 stores across 19 countries. The company's massive domestic layout serves as a dominant economic anchor, with roughly 90% of the United States population residing within 10 miles of a Walmart location.

Today, Walmart is shifting away from simple inventory logistics to operate an integrated digital network. Its ecosystem spans physical hypermarkets, digital marketplaces, the Sparky AI conversational shopping agent, and robust supply chain automation frameworks. By leveraging its brick-and-mortar store footprints as localized micro-fulfillment hubs, Walmart is successfully challenging pure-play e-commerce models by optimizing its delivery unit economics at scale.

WMT Stock Performance in 2026: Financial Health vs. Valuation Premiums

Walmart stock YTD performance as of July 2026 | Source: Google Finance

Walmart’s fiscal 2026 financial metrics highlight the complex task of scaling alternative digital networks inside a massive $680 billion retail architecture. During its Q1 FY2027 disclosure (ended April 30, 2026), the company demonstrated solid top-line performance with earnings per share (EPS) matching street targets, though localized inventory pricing actions limited near-term margin expansions.

|

Financial Metric / Segment |

FY 2025 Reported Data |

FY 2026 Reported Value |

2027 Full-Year Forecast |

|

Consolidated Net Sales |

$681.00 Billion |

$713.00 Billion |

$743.00 Billion Target |

|

Walmart U.S. Comps Growth |

4.50% |

4.60% |

3.5% – 4.5% Guide |

|

E-Commerce Growth Rate |

21.00% |

25.0% Acceleration |

Sustained Double-Digit |

|

Adjusted EPS Value |

$2.42 |

$2.64 |

$2.90+ Consensus Target |

|

Trailing Free Cash Flow |

$13.40 Billion |

$15.20 Billion |

Narrowing Capital Outflow |

|

Current Trailing P/E Ratio |

28.5x |

38.1x |

38.4x Tailored Fair Target |

The core driver behind Walmart's retail durability is the sustained expansion of its omni-channel ecosystem. Digital platforms, private-label consumables, and partner brand additions, such as the expansion of the Shapermint apparel label into an additional 1,600 physical locations, have successfully insulated net revenues against weak general merchandise spending. Furthermore, Walmart signed a long-term power purchase agreement (PPA) with Constellation Energy for emissions-free nuclear energy in Illinois, permanently lowering structural utility inputs.

However, quantitative cash flow models reveal notable divergence. While Walmart trades at 38.1x earnings, substantially above the traditional consumer retailing industry average of 18.5x, a 2-Stage Free Cash Flow to Equity (FCFE) analysis reveals a conservative outlook. Factoring the firm's trailing twelve-month free cash flow of $15.2 billion against extended capital expenditures, the model calculates an intrinsic value floor of just $92.86 to $98.74 per share. This indicates that at the current price of $111.84, the stock carries a structural premium of roughly 10.2% to 26.2% relative to projected long-term cash flows.

Walmart 2026 Trading Strategy: Managing Trend Lines and Technical Corridors

Successfully trading WMT for the remainder of 2026 requires market participants to look past retail sentiment and focus on clear horizontal and quantitative technical indicators:

The $110 Consolidation Pivot

Technical analysts are closely tracking the $110.77 horizontal structural support corridor, which converges with recent mid-summer accumulation lines. As long as WMT maintains weekly closes above this $110 to $114 support cluster, its structural base remains healthy. A clean downside breach of this area would invalidate the short-term recovery pattern and expose the stock to a re-test of its macro 52-week low near $94.23.

Navigating Overhead Moving Averages

On any volume-supported momentum shifts, WMT faces distinct technical sell-zones overhead. The price is currently trading below its 20-day Simple Moving Average (SMA), with immediate heavy resistance standing at the $122.33 horizontal resistance and the 50-day moving average. A decisive breakout above the $122 zone, accompanied by a rising On-Balance Volume (OBV) indicator, is required to shift the trading landscape back to structural momentum buyers.

Walmart 2026 Stock Forecast: $155 Peak Target vs. $81 Bearish Floor

Walmart stock prediction for 2026 by Wall Street analysts

Wall Street firms and quantitative research groups are split on Walmart's near-term valuation framework, dividing the 2026 forecast into three separate operational paths:

The Bull Case for WMT Stock: $138 – $155 Peak on Ad Technology Monetization

Led by aggressive Buy ratings from Tigress Financial Partners and TD Cowen, the ultra-bullish thesis assumes that Walmart successfully materializes its high-margin digital engine. In this scenario, the Vibe.co CTV integration scales quickly through Walmart Connect, driving double-digit operating income expansion that outpaces core sales growth by 2 to 2.5 times. Supported by sustained inflows from high-income consumers and proactive deployment of its $3 billion tariff refund pool, institutional capital flows push the stock past its historic highs toward the peak price targets of $138 to $155.

Walmart's Base Case: $120 – $135 Consensus Plateau

Supported by the consensus of 41 active covering analysts, the base case projects a steady, range-bound recovery channel. Under this model, Walmart maintains its structural value positioning amid defensive consumer rotations, hitting its projected FY2027 net sales target of $743 billion. While higher delivery infrastructure costs cap extreme upside, consistent shareholder rewards via the $30 billion share buyback and steady dividend increases hold the stock within a realistic consensus target band of $120 to $135.

The Bear Case for WMT Stock: $81 – $98 Quantitative Liquidity Check

The highly bearish thesis, sustained by individual underperform ratings and algorithmic Discounted Cash Flow models, focuses on valuation expansion. If Cleveland Research’s flags regarding slowing domestic comparable sales intensify, the core low-margin grocery segment could compress operating margins. Under this framework, if consumer spending patterns contract rapidly, the market may roll back WMT's premium 38.1x P/E multiple toward historical peer group averages, forcing a sharp correction toward the model-derived intrinsic value floor of $81 to $98.

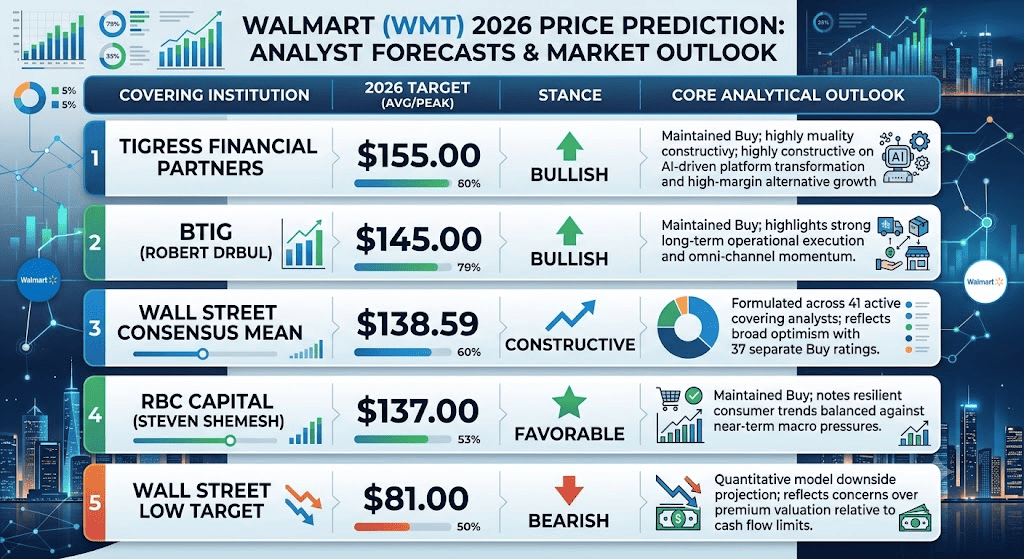

Walmart (WMT) Price Predictions for 2026 by Wall Street Analysts

|

Covering Institution |

2026 Target (Avg/Peak) |

Core Analytical Outlook & Stance |

|

Tigress Financial Partners |

$155.00 |

Bullish: Maintained Buy; highly constructive on AI-driven platform transformation and high-margin alternative growth. |

|

BTIG (Robert Drbul) |

$145.00 |

Bullish: Maintained Buy; highlights strong long-term operational execution and omni-channel momentum. |

|

Wall Street Consensus Mean |

$138.59 |

Constructive: Formulated across 41 active covering analysts; reflects broad optimism with 37 separate Buy ratings. |

|

RBC Capital (Steven Shemesh) |

$137.00 |

Favorable: Maintained Buy; notes resilient consumer trends balanced against near-term macro pressures. |

|

Wall Street Low Target |

$81.00 |

Bearish: Quantitative model downside projection; reflects concerns over premium valuation relative to cash flow limits. |

How to Trade Walmart (WMT) Stock Futures on BingX TradFi

WMT/USDT perpetual contract on BingX TradFi market

Using the advanced, secure BingX TradFi system architecture, market participants can seamlessly capitalize on Walmart's defensive trends and technical volatility:

- Access the BingX TradFi Portal: Log into your verified BingX account and navigate directly to the TradFi section on the primary exchange terminal.

- Locate the Asset: Type WMT into the asset search bar to locate the WMT-USDT perpetual contract interface.

- Configure Leverage and Margin Protocols: Select your preferred account risk management settings: Isolated Margin to strictly confine risk parameters to an individual trade, or Cross-Margin to utilize your broader collateral pool. Set a disciplined leverage multiplier matched for large-cap equities.

- Establish Position Direction: Select Open Long if you expect the combination of the Vibe.co acquisition, digital advertising acceleration, and affluent member growth to drive the equity toward Wall Street's $138+ bullish price targets; select Open Short if you expect slowing domestic comps and high valuation premiums to break the asset down toward its $92 bearish floor.

- Deploy Advanced Risk Parameters: Input your precise entry target, allocate your desired position sizing, and immediately execute mandatory Take-Profit / Stop-Loss (TP/SL) orders to insulate your trading portfolio from unexpected macro market adjustments.

Top 5 Risks to Consider Before Trading Walmart Stock

Before committing active trading capital to Walmart positions, market participants must carefully evaluate these fundamental risk factors:

- Slowing Domestic Comparable Sales: Signs of cooling U.S. comparable growth flag potential consumer spending friction, which could challenge near-term sales guidance if general merchandise sales weaken further.

- Premium Valuation Multiples: Trading at 38.1x earnings puts WMT at a significant premium to its historical peer averages, leaving the stock vulnerable to sharp corrections if execution slowing occurs.

- Fulfillment and Logistics Cost Drag: While omni-channel e-commerce growth remains high at 25%, the associated last-mile delivery and digital infrastructure costs create lingering headwinds for operating margins.

- Macro Inflation and Tariff Adjustments: Shifts in international trade frameworks or renewed consumer spending pressure at the lower income spectrum could restrict Walmart's flexibility in pricing rollbacks.

- Intense Digital Delivery Competition: Competitors like Amazon and Target are continually expanding their next-day and same-day delivery networks, creating constant pressure on Walmart's market share execution.

Final Thoughts: Is Walmart (WMT) Stock a Buy in 2026?

Walmart represents one of the most resilient, large-scale blue-chip assets operating within the global consumer retail landscape. By successfully diversifying into high-margin media channels via its Vibe.co acquisition, rolling out agentic AI search tools, and expanding its high-income subscriber base, the company has built an infrastructure moat that traditional big-box retailers cannot match.

However, trading a mega-cap equity that is priced at a clear valuation premium demands a systematic approach. For active derivatives traders, Walmart's high liquidity, structural option support, and clear response to macro consumer data create an excellent environment for technical volatility capture and momentum trading. Conversely, spot market investors must approach entries defensively, ensuring that the company successfully converts its digital revenue streams into sustained operating income growth before over-leveraging capital.

Risk Reminder: Large-cap consumer defensive equities undergoing structural digital transitions carry execution risks. Always implement strict position sizing, utilize automated stop-loss protocols, and perform independent due diligence.

Related Reading

- Amazon (AMZN) Stock Price Prediction 2026: Can AWS AI Re-acceleration Offset a $200B CapEx Gamble?

- Nike (NKE) Price Prediction 2026: $55.00 Turnaround Comeback or $39.00 Value Trap?

- Apple (AAPL) Stock Outlook for 2026: MacBook Neo Growth or AI Valuation Trap?

- AMC Stock Price Prediction 2026: Fundamental Turnaround or Massive Dilution Trap?

- Ford Stock Price Prediction 2026: $20 Data Center Battery Boom or Legacy Recall Trap?