Marvell Technology Inc (MRVL) has entered 2026 at a historic inflection point, trading near $95 as it solidifies its position as a leading provider of custom AI silicon, high-speed connectivity, and data center semiconductors. With custom ASIC programs for major hyperscalers ramping rapidly and optical interconnect solutions capturing share in next-generation AI clusters, Marvell Technology Inc (MRVL) is transitioning from a broad-based analog and mixed-signal semiconductor company to a core enabler of the AI infrastructure build-out. Explore the institutional price targets, the AI silicon roadmap, and whether MRVL is a buy in 2026.

In early 2026, Marvell Technology Inc (MRVL) decoupled from traditional semiconductor cycles. While storage and carrier markets provide baseline stability, custom AI silicon and data center optics have fueled unprecedented growth. As of March 2026, the narrative centers on hyperscaler ASIC ramps, 800G/1.6T optical module adoption, and margin expansion amid AI demand. Marvell Technology Inc (MRVL) enters 2026 with massive structural tailwinds. CEO Matt Murphy continues to emphasize custom compute and connectivity leadership, projecting sustained triple-digit growth in data center revenue and meaningful margin improvement. With record design wins and manufacturing partnerships, 2026 shapes up as a pivotal year. This guide breaks down the Marvell Technology Inc (MRVL) stock price prediction for 2026 using data from analysts and consensus estimates. You will also discover how to gain exposure to Marvell Technology Inc (MRVL) stock futures through BingX TradFi.

Read more: Ferrari N.V. (RACE) Stock Outlook for 2026: Can An Iconic Brand and EVs Drive RACE Stock to $550+?

Key Highlights: Top 5 Things for Marvell Technology Inc (MRVL) Investors to Know in 2026

- Custom AI Silicon Ramp: Multiple hyperscaler ASIC programs moved into volume production in late 2025, contributing meaningfully to data center revenue.

- Data Center Optics Acceleration: 800G and emerging 1.6T optical interconnect solutions saw strong adoption in AI clusters.

- Revenue Momentum: FY2026 guidance projects data center revenue growth exceeding 60%, driving overall company revenue toward $7 billion+.

- Polarized Targets: Analyst forecasts for 2026 range from bearish lows around $70 to bullish highs of $150 to $170.

- Valuation Debate: Forward P/E around 35–40x reflects AI growth premium, but custom silicon margins and design-win visibility support continued re-rating.

What Is Marvell Technology Inc (MRVL)?

Marvell Technology Inc (MRVL) is a leading semiconductor company specializing in custom compute, high-speed connectivity, storage controllers, and networking solutions. Globally recognized for PAM4 DSPs, custom ASICs for hyperscalers, and data center optics, in 2026 it is increasingly classified as a core AI infrastructure enabler. Its core value lies in custom silicon design wins, optical interconnect leadership, and broad portfolio across data center, enterprise, and carrier markets. Unlike pure-play GPU or memory companies, Marvell Technology Inc (MRVL)'s ecosystem includes custom ASIC expertise, high-speed SerDes technology, and strong partnerships with major cloud providers.

Marvell Technology Inc (MRVL)'s Strategic Evolution (1995–2026): From Storage to AI Infrastructure Leader

Founded in 1995, Marvell Technology Inc (MRVL)'s history features key milestones in semiconductors. Early focus on storage controllers expanded into networking and connectivity. The 2018 acquisition of Cavium accelerated data center presence. Recent years centered on custom AI silicon, PAM4 DSPs, and optical interconnect leadership. From storage roots to AI infrastructure dominance, Marvell Technology Inc (MRVL) has consistently executed strategic acquisitions and technology shifts.

Marvell Technology Inc (MRVL)'s Key Growth Phases Over the Years: From Storage to AI Dominance

Marvell Technology Inc (MRVL)'s journey spans distinct eras:

- Storage & Connectivity Phase (1995–2015): Building hard disk and networking leadership.

- Data Center Expansion Era (2015–2022): Cavium acquisition and cloud connectivity growth.

- The AI Infrastructure Era (2023+): Custom ASICs, optics, and hyperscaler ramps driving hyper-growth.

Read more: What Is TradFi (Traditional Finance) On-Chain: A Beginner's Guide

Marvell Technology Inc (MRVL) 2025 Performance Overview: The Custom Silicon Ramp Year

In 2025, Marvell Technology Inc (MRVL) navigated a mixed semiconductor environment characterized by inventory digestion in some end markets while experiencing explosive demand acceleration in AI data center infrastructure. While storage controllers, carrier networking, and enterprise segments provided baseline stability and cash flow, the custom ASIC programs for major hyperscalers and high-speed optical interconnect solutions delivered triple-digit growth, positioning Marvell Technology Inc (MRVL) as one of the key beneficiaries of the AI training and inference build-out. Record investments in advanced node design, SerDes technology, PAM4 DSP development, and optical module capacity fueled momentum, with several custom silicon programs transitioning from design to volume production and 800G optics gaining rapid adoption in AI clusters. This powerful combination of diversified legacy revenue and hyper-growth AI/data center exposure drove accelerating financial performance and margin improvement, though elevated R&D spending and cyclical pressures in non-AI segments introduced some earnings volatility during the year.

1. MRVL Stock Performance, Market Cap Expansion

Marvell Technology Inc (MRVL)'s stock exhibited powerful momentum throughout 2025, particularly during periods of heightened AI enthusiasm and positive hyperscaler commentary. Shares reached multiple all-time highs, with market capitalization consistently surpassing $80 billion and peaking near $95–$100 billion following strong quarterly updates and design-win announcements. Volatility was elevated compared to broader semiconductor peers due to AI sentiment swings, but the stock maintained premium multiples reflecting Marvell Technology Inc (MRVL)'s custom silicon exposure, optics leadership, and long-term AI infrastructure positioning, while significantly outperforming the broader semiconductor index in key periods.

2. Financial Performance: Revenue Acceleration, Margin Improvement

Marvell Technology Inc (MRVL) delivered progressively stronger results throughout 2025, with full-year revenue showing meaningful acceleration year-over-year, driven primarily by the data center segment. Data center revenue grew triple-digits in multiple quarters, fueled by custom ASIC ramps and high-speed optics demand. Non-AI segments (storage, carrier, enterprise networking) remained stable to modestly down due to inventory corrections but provided important cash flow support. Gross margins expanded significantly as high-margin custom silicon and optics revenue scaled, while operating margins improved notably despite elevated R&D investment. Net income and EPS growth accelerated in the second half of the year, reflecting operating leverage from AI revenue mix.

3. Custom AI Silicon & Optics Surge: Growth Exceeds 100%

Custom ASIC programs for major hyperscalers (Google, Amazon, Meta, Microsoft) moved into volume production during 2025, contributing substantially to data center revenue and marking a key inflection point. Demand for Marvell Technology Inc (MRVL)'s PAM4 DSPs and 800G/1.6T optical interconnect solutions accelerated sharply in AI clusters, with several large customers adopting Marvell Technology Inc (MRVL) technology for next-generation training and inference infrastructure. This segment's growth significantly outpaced the broader semiconductor market and underscored Marvell Technology Inc (MRVL)'s successful positioning as a critical AI connectivity and custom compute supplier.

Read more: Palantir (PLTR) Stock Outlook for 2026: Can AI-Driven Enterprise Supercycle Take PLTR to $235+?

4. Strategic Milestones: Design Wins, Capacity, and AI Focus

Marvell Technology Inc (MRVL) secured additional high-profile custom silicon design wins and expanded manufacturing partnerships with leading foundries to support volume ramps. The company continued heavy investment in next-generation 3nm/2nm design, advanced packaging, and optical module capacity to meet hyperscaler requirements. Significant R&D was directed toward 1.6T optics, co-packaged optics, and next-generation custom compute architectures. Marvell Technology Inc (MRVL) also deepened ecosystem relationships with major cloud providers and AI system integrators, reinforcing its role in AI infrastructure.

The Marvell Technology Inc (MRVL) Thesis for 2026: 5 Data-Driven Pillars of $MRVL Stock Valuation

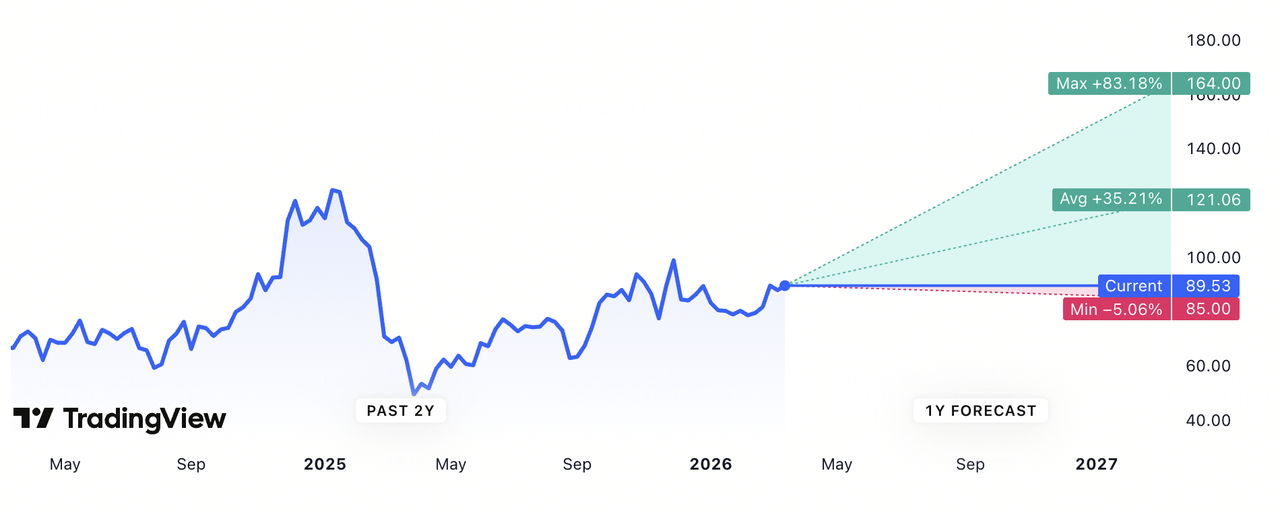

MRVL Price Targets Source: TradingView

While Marvell Technology Inc (MRVL) maintains a well-diversified portfolio across storage, carrier, enterprise networking, and automotive that provides baseline revenue stability and strong free cash flow generation, the company's valuation in 2026 is overwhelmingly driven by its rapidly expanding role as a core enabler of AI data center infrastructure. Through custom silicon design wins with major hyperscalers, leadership in high-speed PAM4 DSPs and optical interconnects, and proven execution on advanced node programs, Marvell Technology Inc (MRVL) is positioned to capture outsized share of the multi-hundred-billion-dollar AI compute and connectivity opportunity. These five pillars explain why many analysts view MRVL as one of the most structurally attractive semiconductor plays in the AI era.

Read more: Accenture (ACN) Outlook 2026: Can AI Transformation and Consulting Demand Drive ACN Stock to $450+?

1. Custom AI Silicon: The Core Growth Pillar

Marvell Technology Inc (MRVL) has secured multiple high-profile custom ASIC programs with leading hyperscalers (Google, Amazon, Meta, Microsoft, and others), several of which transitioned from design/tape-out to volume production in late 2025 and are ramping aggressively in 2026. These programs drive triple-digit data center revenue growth, deliver significantly higher gross margins than standard products, and create long-term design-win stickiness due to the deep integration and multi-year nature of custom silicon. As hyperscalers increasingly rely on tailored accelerators to optimize training and inference costs, Marvell Technology Inc (MRVL)'s proven execution on complex ASICs positions it to secure additional wins and sustain high-growth contribution from this segment for years.

2. Data Center Optics & Connectivity: The High-Growth Pillar

Marvell Technology Inc (MRVL) holds leading positions in PAM4 DSPs, SerDes IP, and high-speed optical modules critical for AI cluster interconnects. The transition to 800G and emerging 1.6T optics is accelerating rapidly in 2026 as next-generation AI training clusters require dramatically higher bandwidth and lower power per bit. Marvell Technology Inc (MRVL)'s optical solutions capture outsized share of this exploding demand, with strong design-win momentum and volume ramps already underway. This segment provides sustained high growth, attractive margins, and a natural hedge against custom ASIC cyclicality due to its role as essential connectivity infrastructure across multiple hyperscaler platforms.

3. Diversified Portfolio & Cash Flow Stability: The Foundation Pillar

Beyond AI, Marvell Technology Inc (MRVL) generates meaningful recurring revenue from storage controllers (HDD/SSD), carrier/5G networking, enterprise Ethernet, and automotive solutions. These segments provide important cash flow stability, fund continued heavy R&D investment in AI, and offer a defensive base during potential AI spending pauses or inventory corrections. The diversified mix reduces overall earnings volatility compared to pure-play AI silicon companies and supports consistent free cash flow generation even in softer market environments.

4. Margin Leverage & Operating Efficiency: The Profitability Pillar

As custom silicon and high-speed optics revenue scales, Marvell Technology Inc (MRVL) benefits from powerful operating leverage. Custom ASICs and advanced optics typically carry significantly higher gross margins than legacy products, while disciplined cost management, mix shift, and manufacturing efficiencies drive gross and operating margin expansion. Analysts project meaningful margin improvement in 2026 as AI-related revenue becomes a larger portion of the total, creating a virtuous cycle of earnings growth, free cash flow acceleration, and potential multiple expansion.

5. Design-Win Moat & Hyperscaler Relationships: The Defensive Pillar

Marvell Technology Inc (MRVL) has built deep, multi-year strategic relationships with the world's largest hyperscalers through proven custom ASIC execution, best-in-class SerDes and PAM4 DSP technology, and early leadership in co-packaged optics. These relationships create formidable competitive barriers, new entrants face years of qualification, ecosystem integration, and trust-building. The sticky nature of custom silicon (once designed into a platform, switching costs are extremely high) and Marvell Technology Inc (MRVL)'s track record of delivering on complex programs provides long-term visibility into AI infrastructure spending and protects against near-term competitive displacement.

Marvell Technology Inc (MRVL) Price Forecasts for 2026: Bull vs. Bear Outlook

Institutional views on Marvell Technology Inc (MRVL) stock remain divided, balancing explosive AI data center momentum against cyclical risks and execution challenges. The wide range from bullish targets above $150 to bearish calls below $90 captures uncertainty around AI CapEx cycles, custom program execution, and broader semiconductor demand.

|

Institution / Analyst |

2026 Price Target |

Market Outlook |

|

Morgan Stanley |

$150 to $170 |

Super-Bullish: Custom ASIC ramps and optics momentum drive significant upside. |

|

Goldman Sachs |

$145 |

Bullish: Maintains Buy on AI data center leadership and design-win strength. |

|

Market Consensus (aggregated from MarketBeat, TipRanks, Zacks) |

$120 to $130 |

Moderate Buy: Balanced view on AI growth offset by cyclical exposure. |

|

JPMorgan |

$115 |

Neutral: Hold rating on execution and spending cycle watch. |

|

Bearish Outlooks (various low-end) |

$70 to $90 |

Pessimistic: AI spending moderation, competition, and cyclical risks. |

Source: Aggregated from MarketBeat, Yahoo Finance, and analyst reports (as of early March 2026)

The wide range from bullish targets above $150 to bearish calls below $90 captures uncertainty around AI CapEx cycles, custom program execution, and broader semiconductor demand.

The Bull Case: The AI Surge Drives MRVL Stock Price Above $150

Bulls focus on Marvell Technology Inc (MRVL)'s custom silicon ramps with major hyperscalers and leadership in high-speed data center optics. If Marvell Technology Inc (MRVL) sustains triple-digit data center revenue growth, successfully executes ASIC volume ramps, and captures significant share of 800G/1.6T interconnect demand, the company could achieve strong EPS growth and multiple expansion. This positions Marvell Technology Inc (MRVL) as a critical AI infrastructure enabler, supporting targets of $150 or higher by year-end 2026.

The Bear Case: The Correction to $90 or Lower

Bears highlight heavy cyclical exposure and competition risks. If hyperscaler AI CapEx moderates, custom programs face delays or losses, or broader semiconductor inventory corrections intensify, multiples could compress sharply. Execution shortfalls would drive the share price lower, with some targets in the $70 to $90 range.

Read more: PepsiCo (PEP) Stock Outlook for 2026: Can PEP Cross $220 on Beverage Portfolio and Emerging Markets?

Long or Short Marvell Technology (MRVL) Stock Futures with USDT on BingX TradFi

Marvell Technology stock perpetuals on the futures market with BingX AI insights

For active traders looking to capitalize on high-volatility events like earnings reports, BingX TradFi offers advanced margin trading.

- Go to the BingX TradFi section and select Stock Futures.

- Locate the MRVL/USDT perpetual contract.

- Choose your Margin Mode (Isolated or Cross) and set your Leverage (typically 2x–5x is recommended for equities).

- Analyze the trend and select Open Long if you expect a price increase or Open Short to profit from a decline.

- Set your Take-Profit (TP) and Stop-Loss (SL) levels immediately to manage risk against 2026's aggressive price swings.

5 Critical Risks to Watch for Marvell Technology Inc (MRVL) Traders in 2026

While Marvell Technology Inc (MRVL)'s custom AI silicon ramps, high-speed connectivity leadership, and data center optics momentum offer substantial upside through hyperscaler AI infrastructure demand and margin expansion, traders must navigate a complex landscape of semiconductor cyclicality, competitive intensity, execution challenges, supply chain constraints, and macro demand variability.

1. AI Spending Cycle Sensitivity and Hyperscaler CapEx (short for Capital Expenditure or Capital Expenses) Volatility

Marvell Technology Inc (MRVL)'s growth is heavily dependent on hyperscaler capital expenditures for AI data centers. A slowdown, pause, or redirection of AI infrastructure spending in 2026, due to ROI scrutiny, economic uncertainty, or shifts in AI model training priorities, could materially reduce demand for custom ASICs and high-speed optical interconnects. Even a temporary flattening of hyperscaler CapEx would cause data center revenue to moderate sharply, pressuring overall growth and exposing the stock to significant downside given the high contribution from AI-related programs.

2. Intensifying Competition in Custom Silicon and Data Center Connectivity

Competitors including Broadcom (custom ASICs for Google/others), Nvidia (GPU dominance and networking push), AMD, Intel, and emerging AI silicon startups are rapidly advancing in custom compute and high-speed interconnects. If Marvell Technology Inc (MRVL) loses key hyperscaler design wins, sees share erosion in 800G/1.6T optics, or faces pricing pressure in DSPs and SerDes, the revenue ramp from custom programs could slow or stall. Increased competition would also limit margin upside in high-growth AI segments.

3. Execution and Custom ASIC Ramp Risks

Marvell Technology Inc (MRVL) has multiple hyperscaler ASIC programs moving into volume production, but execution remains critical. Delays in tape-out, yield issues, design validation challenges, customer qualification delays, or failure to meet performance/power targets could push out revenue recognition, reduce customer confidence, and impact bookings conversion. Any material execution shortfall in these high-visibility programs would undermine investor faith in Marvell Technology Inc (MRVL)'s AI custom silicon leadership.

4. Supply Chain, Foundry, and Manufacturing Constraints

Marvell Technology Inc (MRVL) relies on leading-edge foundries (TSMC, Samsung) for advanced nodes and complex packaging for custom ASICs and optics. Prolonged foundry capacity constraints, wafer shortages, advanced packaging bottlenecks, or geopolitical disruptions affecting supply chains could limit production volumes, delay customer ramps, and constrain revenue growth. These risks are amplified in the AI boom where compute demand far outstrips near-term supply.

5. Macro and Non-AI Segment Cyclicality

While AI is the primary driver, Marvell Technology Inc (MRVL) still derives meaningful revenue from storage (HDD/SSD controllers), carrier networking, and enterprise markets. A broader semiconductor inventory correction, reduced enterprise IT spending, or slowdown in 5G/edge deployments could pressure these legacy segments, offsetting AI gains and creating earnings volatility. Macro weakness would also indirectly impact hyperscaler budgets and AI investment pace.

Read more: Eli Lilly (LLY) Stock Outlook 2026: Can Mounjaro and Zepbound Momentum Drive LLYON Stock to $1,200+?

Conclusion: Should You Invest in Marvell Technology Inc (MRVL) Stock in 2026?

Deciding whether to invest in Marvell Technology Inc (MRVL) in 2026 requires viewing it as a high-conviction play on AI data center infrastructure rather than a broad-based semiconductor company. For growth-oriented investors with tolerance for cyclicality and execution risk, Marvell Technology Inc (MRVL)'s custom ASIC ramps with major hyperscalers, leadership in high-speed optics (800G/1.6T), strong design-win momentum, and expanding data center revenue contribution support significant upside if AI spending continues and programs execute smoothly. Successful scaling of custom silicon and connectivity solutions could drive substantial returns and multiple expansion.

For conservative or risk-averse investors, the stock's heavy dependence on hyperscaler CapEx cycles, intense competition from Broadcom and Nvidia, foundry/supply chain vulnerabilities, and exposure to broader semiconductor cyclicality present substantial downside risks. The performance now ties to multiple key drivers: either AI infrastructure demand and custom program execution accelerate to justify the premium, or spending moderation, competitive losses, or supply bottlenecks trigger sharp multiple compression. Closely monitor quarterly data center revenue trends, custom ASIC ramp updates, optical module adoption metrics, hyperscaler CapEx guidance, and semiconductor industry inventory cycles as the clearest signals of whether Marvell Technology Inc (MRVL) can sustain its position as a core AI infrastructure enabler in 2026.

Risk Reminder: Trading and investing in equities like MRVL involves substantial risk of capital loss. Marvell Technology Inc (MRVL)'s high valuation, cyclical exposure, dependence on hyperscaler spending, and execution risks in custom silicon make it a high-risk asset. Investors should conduct thorough independent research and consider professional financial advice before allocating capital.

Related Reading

- Circle IPO (2025) Everything You Need to Know About CRCL, Valuation, What It Means for Crypto Market

- Strategy (MSTR) Stock Outlook 2026: Can MSTR Cross $700 on Bitcoin Treasury Strategy?

- Robinhood Stock Forecast 2026: $130 Hyper-Growth or Valuation Correction?

- Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?

- What Are Coinbase Tokenized Stocks COINX and COINON and How to Buy Them?