In late June 2026, Micron Technology Inc. (NASDAQ: MU) finds itself positioned at a dramatic crossroads between an unprecedented AI hardware infrastructure boom and the stark historical realities of semiconductor cyclicality. Following a spectacular, record-breaking third-quarter financial report on June 24, 2026, the Boise, Idaho-based chipmaker surged over 13% in extended-hours trading, reclaiming a market capitalization above $1.18 trillion and pushing shares past the $1,213 threshold. This caps an astonishing, vertical 232% year-to-date rally that has established MU as one of the elite performers of the global technology sector.

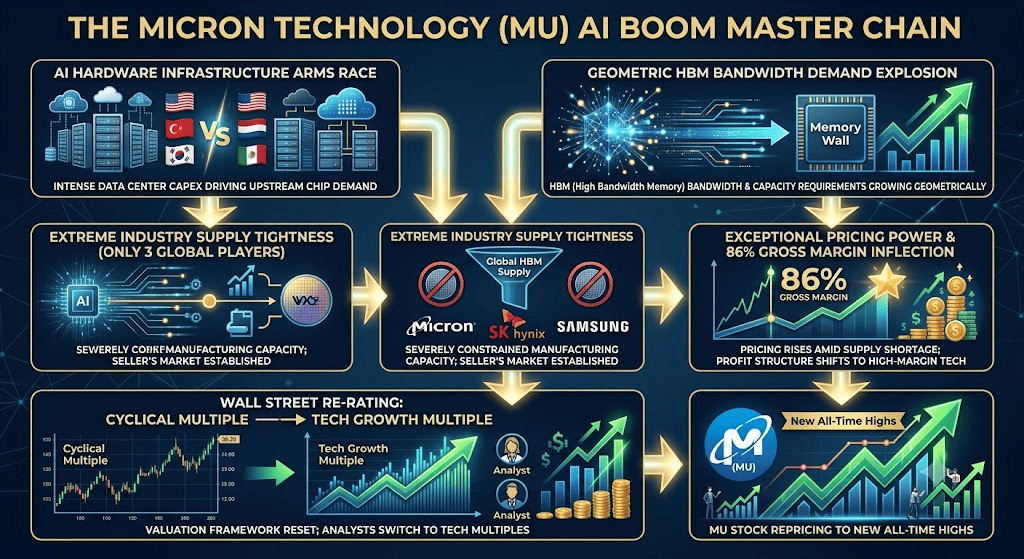

While the stock spent previous cycles anchored to the volatile ups and downs of standard PC and smartphone memory chips, a structural supply shortage in High Bandwidth Memory (HBM) has fundamentally transformed Micron's corporate profile. Investors are aggressively weighing an eye-popping 346% year-over-year quarterly revenue explosion against a growing wave of open-market insider sales and strict valuation warnings from macro bears.

As hyperscale cloud providers like Microsoft, Google, Meta, and Amazon accelerate global data center capital expenditures beyond an estimated $2.7 trillion, memory has shifted from a generic commodity to a non-negotiable strategic asset. However, the sheer velocity of the stock's parabolic run has ignited a fierce debate on Wall Street: Is Micron now a permanent, high-margin AI growth monopoly, or is the market dangerously paying peak-cycle multiples for a business that will eventually face supply normalization?

This guide breaks down the Micron stock forecast and price prediction for the remainder of 2026, utilizing data from Bank of America, JP Morgan, Susquehanna, Goldman Sachs, and official regulatory filings.

You will also discover how to trade Micron Technology (MU) stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Micron (MU) Traders to Know in 2026

As Micron navigates a high-stakes environment of sold-out production lines and massive capacity expansion, traders must closely monitor these five market-moving factors:

- The $22 Billion Eco-System Lock-In: Micron has secured a historic strategic supply partnership with Anthropic, alongside 16 comprehensive Supply Commitment Agreements (SCAs) with core hyperscalers. This has yielded a staggering $22 billion in total contract cash commitments, backed by nearly $18 billion in upfront cash deposits.

- Revolutionary 'Take-or-Pay' Contract Structures: For the first time in memory history, Micron has insulated its business via 5-year, non-cancellable, Take-or-Pay provisions featuring quarterly price collars. This structural shift effectively transfers cyclical pricing risk directly to the buyers.

- The Unprecedented 86% Gross Margin Inflection: Driven by high-premium HBM3E and next-generation HBM4 shipments, Micron's gross margins surged to 84.6% in Q3, with formal Q4 management guidance pointing to an uncharted 86%. This profit structure mirrors elite software firms rather than traditional hardware manufacturers.

- Nvidia Vera Rubin Platform Endorsement: Chief Financial Officer Mark Murphy confirmed that Nvidia has officially certified Micron as a primary HBM4 supplier for its upcoming ultra-premium Vera Rubin (B300) GPU architecture, which utilizes 8 HBM stacks per unit, a 33% quantity increase over the Blackwell B200.

- The SK Hynix $29 Billion Nasdaq Threat: South Korean arch-competitor SK Hynix is advancing plans for a massive $29 billion standalone Nasdaq listing. Once completed, this liquidity event could dilute Micron's premium status as the sole major U.S.-listed pure-play HBM manufacturer.

What Is Micron Technology (MU)?

Micron Technology Inc. (NASDAQ: MU) is a global leader in advanced semiconductor memory and storage solutions. The company's core portfolio consists of dynamic random-access memory (DRAM), low-power LPDRAM, and negative-AND (NAND) flash architecture. These technologies serve as the essential data-retrieval and storage engines across cloud data centers, enterprise networking, automotive systems, and consumer electronics.

In 2026, Micron occupies a critical, irreplaceable role in the global AI hardware stack. Because modern AI large language models (LLMs) feature parameter counts scaling at geometric rates, standard computing architectures are bottlenecked by data-transfer speeds. Micron’s HBM solves this 'memory wall' by vertically stacking memory dies using through-silicon vias (TSVs), delivering the extreme bandwidth required by tier-one AI processors.

Read more: Top 10 AI Hardware Stocks to Watch in 2026: The Architecture Driving Next-Gen Intelligence

Micron's Performance in Early 2026: The AI Supercycle Re-Rating

Micron kicked off the middle of calendar year 2026 by delivering a blockbuster fiscal third-quarter report that shattered even the most optimistic sell-side estimates. Quarterly revenue hit a staggering $41.46 billion, beating the consensus estimate by $5.77 billion, a 16% positive surprise, and marking an astronomical 346% year-over-year revenue increase. Non-GAAP adjusted earnings per share (EPS) landed at $25.11, soundly beating Wall Street projections of $20.20.

Core Financial Snapshot — Q3 FY2026

|

Metric |

Actual Results |

Consensus Estimate |

Beat / Variance |

|

Quarterly Revenue |

$41.46B |

$35.69B |

+$5.77B (+16%) |

|

Adjusted EPS |

$25.11 |

$20.20 |

+$4.62 (+24%) |

|

Q4 Revenue Guidance |

$49.0B–$51.0B |

$43.24B |

+$6.80B (+16%) |

|

Q4 EPS Guidance |

$31.00 (Midpoint) |

$25.50 |

+$5.50 (+22%) |

|

Operating Margin |

80.40% |

25.4% (Historical) |

Significant Expansion |

Single-quarter data center revenue exploded to $25 billion, capturing over 60% of Micron's total business. This massive surge was supplemented by a $5 billion quarter for enterprise solid-state drives (SSDs), where Micron holds a commanding position via its Gen6 NVMe technologies. Free cash flow margins climbed to a robust 44.2%.

Crucially, management offered an incredibly bullish near-term outlook, guiding Q4 revenue to a midpoint of $50 billion and EPS to $31.00, figures that sit substantially above previous consensus numbers. This massive 'beat-and-raise' execution has fundamentally reset the stock's baseline, forcing Wall Street analysts to abandon traditional cyclical valuation models in favor of growth-tech multiples.

Micron 2026 Trading Strategy: How to Navigate Extreme Semiconductor Beta

Successfully trading a mega-cap asset that has climbed over 260% year-to-date requires looking past short-term momentum and anchoring execution to technical support levels, supply constraints, and corporate insider patterns.

The $990 - $1,050 Structural Support Floor

Following its post-earnings vertical gap, the $990 to $1,050 zone represents an important structural consolidation window. As long as MU respects this zone on weekly candle closes, the macro accumulation structure remains highly intact. Traders can view pullbacks to this region as prime areas for identifying institutional accumulation.

Evaluating the HBM4 Sold-Out Backlog vs. Macro Capex Risks

Chief Commercial Officer Sumit Sadana stated explicitly that Micron's entire HBM3E and HBM4 capacity is fully sold out through the end of calendar year 2027, with orders stretching into 2028. This extreme supply visibility heavily de-risks near-term revenue. However, macro traders must cross-reference this with aggregate cloud hyperscaler capex trends; any sudden cooling in downstream AI monetization could cause minor multi-quarter order pauses.

Monitoring Insider Liquidations and the Peak-Cycle Multiple

With the stock trading at an elevated trailing multiple, bears frequently point out that CEO Sanjay Mehrotra and various senior executives have executed over 100 net insider selling transactions throughout mid-2026, offloading tranches between $942 and $979. While much of this is automated, pre-scheduled 10b5-1 selling, it serves as a technical reminder that capital preservation strategies are actively occurring near the psychological $1,200 barrier.

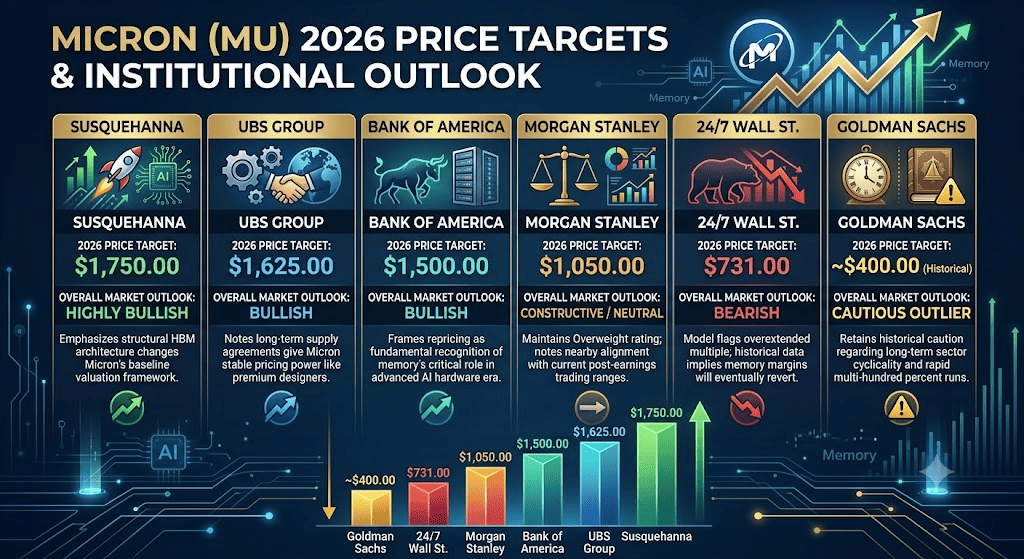

Micron 2026 Stock Forecast: $1,500 Multi-Year Supercycle vs. $731 Bear Trap

Evaluating Micron’s forward path requires balancing a structural supply deficit against the historical tendency of the memory market to overproduce during cyclical peaks.

Micron's Bull Case: The $1,500+ Structural Technology Re-Rating

The bullish thesis is built on the reality that the HBM Total Addressable Market (TAM) is scaling at a blinding pace, with projections now exceeding $100 billion by 2027, a full year ahead of initial analyst expectations. Tapped as a verified supplier for Nvidia's high-premium Vera Rubin architecture, Micron is firmly insulated at the absolute top tier of hardware hardware components.

Furthermore, because HBM manufacturing features an aggressively high wafer trade ratio, consuming significantly more physical wafer area than standard DRAM, global production capacity is naturally constricted. Since greenfield output from Micron's domestic facilities in Idaho One and Idaho Two won't scale until 2028, supply will remain structurally behind demand for the foreseeable future. Supported by price targets from Bank of America ($1,500), UBS ($1,625), and Susquehanna ($1,750), the bull case assumes that expanding pricing power will drive FY2027 EPS toward $121, powering the equity past near-term resistance toward a multi-trillion dollar valuation.

The Base Case: $1,100 – $1,350 Post-Earnings Consolidation

The base case envisions a scenario where the market actively absorbs Micron’s spectacular operational numbers but encounters minor upside resistance due to overall valuation optimization. In this environment, commercial revenue continues to comfortably hit the guided $50 billion Q4 mark as enterprise SSD and agentic-AI LPDRAM sales accelerate alongside core HBM products.

However, upside momentum may face a temporary speed limit as capital flows adjust for the upcoming SK Hynix Nasdaq listing and potential yield recoveries from Samsung. This creates a volatile, range-bound consolidation phase between $1,100 and $1,350, where massive quarterly earnings beats are digested by broader macroeconomic asset allocation shifts.

Micron's Bear Case: The $731 Valuation Mean-Reversion Trap

The bearish outlook focuses entirely on valuation extension and structural normalization. Championed by cautious models like the 24/7 Wall St. technical framework, this path highlights that at over 53x trailing earnings, Micron is priced for a flawless, non-cyclical future. If Samsung successfully resolves its HBM4 manufacturing yield bottlenecks earlier than expected, global supply could rebalance with surprising speed, compressing Micron's current premium pricing structures.

This risk is compounded if high-growth AI names experience a temporary cool-down or macro liquidity tightens. If quarterly results merely match guidance rather than delivering massive outperformance, momentum capital could rapidly rotate out of extended hardware names. Under this bear case, a technical breach of the psychological $1,000 support level could trigger a swift mean-reversion selloff back toward the structural $731 support zone.

Micron (MU) Price Predictions for 2026 by Wall Street Analysts

|

Institution |

2026 Price Target (Peak / Avg) |

Overall Market Outlook |

|

Susquehanna |

$1,750.00 |

Highly Bullish: Emphasizes that structural HBM architecture changes Micron’s entire baseline valuation framework. |

|

UBS Group |

$1,625.00 |

Bullish: Notes long-term supply agreements give Micron stable pricing power similar to premium computing designers. |

|

Bank of America |

$1,500.00 |

Bullish: Frames the repricing as a fundamental recognition of memory's critical role in the advanced AI hardware era. |

|

Morgan Stanley |

$1,050.00 |

Constructive / Neutral: Maintains Overweight rating but notes nearby alignment with current post-earnings trading ranges. |

|

24/7 Wall St. |

$731.00 |

Bearish: Model flags an overextended multiple; historical data implies memory margins will eventually revert to mid-cycle averages. |

|

Goldman Sachs |

$400.00 (Historical) |

Cautious Outlier: Retains historical caution regarding long-term sector cyclicality and rapid multi-hundred percent runs. |

How to Trade Micron (MU) Stock Futures on BingX TradFi

MU/USDT perpetual futures on BingX TradFi

As Micron navigates this historic period of public market price discovery, tactical traders can seamlessly capitalize on its short-term and long-term price action through the BingX platform:

- Access BingX TradFi: Head to the BingX TradFi section on the main BingX exchange platform interface.

- Select Micron (MU): Locate and select the MU-USDT perpetual futures contract.

- Choose Your Direction: Select Open Long if you believe the $22 billion contract backlog, 86% gross margin expansion, and Nvidia HBM4 integration will drive the stock toward its $1,500 street target. Select Open Short if you believe executive insider sales and cyclical valuation limits will trigger a pullback toward the $731 support floor.

- Configure Leverage and Margin Mode: Set your preferred Isolated or Cross-Margin parameters alongside highly disciplined leverage to maximize your capital efficiency.

- Enforce Strict Risk Controls: Utilize advanced BingX Take-Profit and Stop-Loss (TP/SL) automated execution lines to safeguard your capital against unexpected gaps during high-volatility market openings.

Top 5 Risks to Consider Before Investing in MU Stock

While Micron's structural AI transformation presents a highly compelling narrative, navigating this high-beta asset demands a careful evaluation of its core operational risks:

- Extreme Customer Concentration: Micron's premium HBM order book is heavily concentrated among a select few tier-one AI customers, specifically Nvidia. Any downstream shipment delays or chip-architecture alterations by these anchor clients will directly impact top-line execution.

- Competitor Production Surges: The HBM arena is a tight three-player race consisting of Micron, SK Hynix, and Samsung. If either competitor aggressively scales competing HBM4 yields ahead of schedule, Micron's exceptional pricing power could normalize.

- Capital Expenditure Friction: Management has guided FY2027 capex 'above low-to-mid $40 billion' to build out greenfield sites. This record level of investment introduces massive cash-burn demands that require peak-cycle revenue to execute cleanly.

- Downstream AI Monetization Speed: The entire semiconductor ecosystem is valued on the assumption that hyperscaler AI infrastructure spending will continue unhindered. A near-term deceleration in public cloud AI monetization could lead to downstream contract restructuring.

- Geopolitical and Supply Moat Vulnerabilities: While domestic manufacturing inside the U.S. offers massive regulatory, CHIPS Act, and national security advantages, global chip assembly lines remain deeply interconnected across Asian corridors, leaving the stock exposed to international trade frictions.

Read more: What Is the U.S. CHIPS and Science Act? Its Impact on Semiconductors, Technology, and Crypto in 2026

Final Thoughts: Is Micron (MU) Stock a Buy in 2026?

As of June 2026, Micron Technology represents one of the most fundamentally transformed and strategically vital plays within the entire global artificial intelligence ecosystem. The company’s ability to completely alter its underlying contract mechanics, shifting into 5-year, non-cancellable, take-or-pay structures backed by billions in cash deposits, proves that this upcycle is qualitatively different from the memory cycles of the past decade. An 86% gross margin profile provides definitive proof of immense structural pricing power.

However, navigating an asset that has experienced a vertical, multi-hundred percent rally requires meticulous execution. For short-term tactical traders, the stock offers an unparalleled environment for premium volatility capture via BingX futures. Long-term market participants, conversely, may find it most prudent to position themselves defensively, scaling into exposure during technical consolidations to ensure they are well-positioned as Micron's next-generation HBM4 architectures fully deploy into the elite AI supercomputing tier.

Risk Reminder: Trading mega-cap semiconductor equities involves substantial capital risk due to high beta metrics, rapid technological iteration, and changing institutional asset allocations. Always maintain strict position sizing, disciplined margin rules, and explicit stop-loss parameters.

Related Reading

- Top High-Bandwidth Memory (HBM) Stocks to Buy in the 2026 Memory Supercycle

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

- Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure

- Roundhill Memory ETF (DRAM) Forecast 2026: $1.5B AI Supercycle or 'RAMmageddon' Trap?

- SanDisk (SNDK) Price Prediction 2026: AI Memory Supercycle or $913 Technical Peak?