Bitcoin (BTC) is the cryptocurrency with the highest liquidity globally. Price differences or fee structure variations suitable for arbitrage often exist between different exchanges, as well as between spot and futures markets. The core logic of arbitrage strategies is to exploit pricing deviations of the same asset across different markets by simultaneously establishing hedged positions in both directions, theoretically reducing dependence on market direction while systematically earning spreads or fee income. For Taiwanese investors, BTC arbitrage is one of the most commonly explored strategies by advanced traders, ranging from beginner-friendly funding rate arbitrage to cross-exchange arbitrage requiring API programming, with strategy options varying significantly based on technical barriers.

However, arbitrage strategies are not truly risk-free. Position opening fees, withdrawal costs, execution delays, and reversals in funding rate direction can all compress or even consume arbitrage profits. Choosing the appropriate strategy type and execution platform is fundamental to whether BTC arbitrage can operate stably in the long term. For Taiwanese individual investors, funding rate arbitrage is the entry method with the lowest barrier and most intuitive operational logic; cross-exchange arbitrage and statistical arbitrage require higher capital scale and programming capabilities, suitable for advanced users with corresponding technical backgrounds.

This article starts from the practical usage scenarios of Taiwanese BTC arbitrage investors, systematically introduces the operational logic and barriers of various BTC arbitrage strategies, explains how to execute funding rate arbitrage on BingX, compares the automation level, cost structure, and capital requirements of mainstream arbitrage tools, and provides complete operational process tutorials to help Taiwanese investors find the most suitable BTC arbitrage entry point for their situation.

Key Takeaways

- BTC funding rate arbitrage is the lowest-barrier entry arbitrage strategy for Taiwanese individual investors. By simultaneously holding spot long positions and BingX futures short positions to form a hedge, it collects funding rate compensation every 8 hours without requiring API programming capabilities.

- BingX perpetual futures maker fee is 0.02%, taker fee is 0.05%, spot fee is 0.1%, with funding rate arbitrage single-round position opening cost of approximately 0.15%, among the lowest levels on mainstream platforms, combined with Traditional Chinese interface that is most user-friendly for Taiwanese users.

- Arbitrage strategies are not risk-free. Negative funding rates are the most direct risk for funding rate arbitrage. Rate monitoring mechanisms should be established to exit promptly when rates turn negative, avoiding accumulated losses after compensation direction reversal.

- Cross-exchange arbitrage price difference windows typically last only seconds. Manual operations can hardly complete before the window closes, usually requiring API automation programs, posing high technical barriers for general Taiwanese individual investors.

- Arbitrage profits can be transferred from BingX to MAX or BitoPro via USDT TRC-20 (withdrawal fee under $1) for TWD conversion, following Taiwan's compliant withdrawal path while retaining transaction records for tax reporting.

What Are the Main Bitcoin Arbitrage Strategies?

BTC arbitrage is not a single strategy; different types vary significantly in operational logic, required tools, capital requirements, and risk structure. Before entering platform and tool comparisons, understanding the characteristics of various arbitrage methods helps quickly determine which strategy best fits individual conditions. The following are the four most common BTC arbitrage strategies currently in the market:

- Funding Rate Arbitrage: This is the most easily executable entry arbitrage strategy for Taiwanese individual investors. Perpetual futures use the "funding rate" mechanism to exchange funds between long and short positions every 8 hours; when the market is bullish, short position holders can receive fee income from long positions. In practice, traders buy BTC in the spot market while establishing equal-sized short positions in the futures market, hedging price volatility risk while earning only funding rates. This strategy can be completed within a single platform, requires no API or automation programs, making it the lowest-barrier and most feasible arbitrage method.

- Cross-Exchange Spot Arbitrage: This strategy exploits BTC price differences between different exchanges, buying on low-price platforms and selling on high-price platforms to earn the spread. Although the logic is intuitive, actual execution difficulty is high: market spreads are usually eliminated in extremely short periods, manual operations cannot keep up; cross-platform asset transfers take time, during which reverse price risk may be borne; trading fees and withdrawal costs must also be deducted. Most cases require API automation execution, more suitable for advanced users with programming capabilities.

- Triangular Arbitrage: Triangular arbitrage is completed within a single exchange, conducting cyclical trades through exchange rate inconsistencies among three trading pairs. For example, BTC/USDT → USDT/ETH → ETH/BTC; if deviations exist among exchange rates, profits can be locked through multiple exchanges. Such opportunities typically exist only for extremely short periods (millisecond-level) and are mostly captured by high-frequency trading systems, requiring extremely high latency and execution efficiency, practically needing low-latency APIs, unsuitable for general investors' manual operations.

- Statistical Arbitrage: Statistical arbitrage is based on historical price relationships between BTC and other assets. When the two deviate from statistical mean, hedged positions are established, waiting for relationship regression to profit. This strategy relies on quantitative models and data analysis capabilities, and correlations may fail for extended periods during market structure changes or extreme market conditions, leading to sustained losses. Suitable for traders with quantitative backgrounds; not recommended for general investors to attempt directly.

BTC Arbitrage Strategy Comparison: Requirements, Tools, and Risks

|

Arbitrage Strategy |

Operational Logic |

Technical Barrier |

Capital Requirement |

Automation Need |

Main Risks |

Suitable For |

|

Funding Rate Arbitrage |

Spot long + futures short, earn funding rates |

Low |

Low to Medium |

Not Required |

Rate reversal, fees eroding profits |

Beginners, Individual investors |

|

Cross-Exchange Arbitrage |

Buy low, sell high across different exchanges for spreads |

Medium |

Medium to High |

High (API required) |

Spread disappearance, transfer delays, fees |

Advanced traders |

|

Triangular Arbitrage |

Cyclical arbitrage across multiple trading pairs within same exchange |

High |

Medium |

Very High (Low-latency programs) |

Extremely short windows, slippage, execution failure |

Algorithmic traders |

|

Statistical Arbitrage |

Hedge based on asset correlation deviations from mean |

High |

High |

High (Quantitative models) |

Correlation breakdown, model risk |

Quantitative traders |

Why BingX Is the Top Platform for Bitcoin Arbitrage Trading

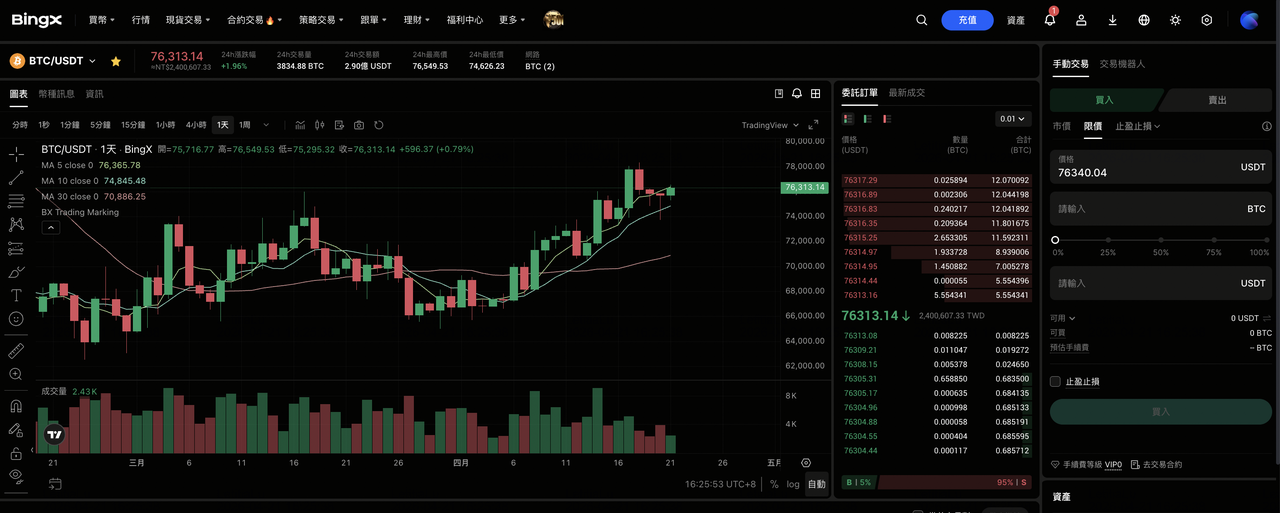

Among the four strategies above, funding rate arbitrage is the most executable option for Taiwanese individual investors. The entire process can be completed within BingX's single platform, requiring no cross-platform fund transfers or API programming. BingX has clear advantages in fee structure for this strategy: spot taker fee 0.1%, futures taker fee 0.05%, with single-round position opening cost approximately 0.15%. When funding rates exceed 0.15% (per settlement cycle), the first settlement can cover position opening costs, with subsequent settlement cycles becoming net profit. BingX's futures page simultaneously provides real-time display of BTC estimated funding rates and settlement times, with open access to historical rate queries, making arbitrage feasibility assessment more transparent and reference-based.

Operating Principles of Funding Rate Arbitrage

The core of the strategy lies in establishing fully hedged bilateral positions: simultaneously holding BTC spot long positions and equal-sized BTC futures short positions, making them offset each other under price fluctuations. When BTC rises, spot position profits are offset by futures short losses; conversely, the overall position's sensitivity to price direction is minimized, with income mainly from funding rate compensation settled every 8 hours. The key to execution is ensuring spot quantity exactly matches futures short position size; any deviation represents unhedged directional risk exposure. BingX provides complete Traditional Chinese interface and 24-hour customer support. During arbitrage operations, if account, transfer, or withdrawal issues arise, real-time Chinese assistance is available, enhancing overall execution stability.

- Low Futures Fees: Maker fee 0.02%, taker fee 0.05%, effectively reducing BTC arbitrage position opening costs, providing long-term advantages for high-frequency operations

- Transparent Funding Rates: Futures page displays estimated rates and settlement times in real-time, with queryable historical rates for clear arbitrage feasibility assessment

- Single Platform Completion: Both spot and futures operations on BingX, no cross-platform fund transfers needed, suitable for Taiwanese entry-level arbitragers

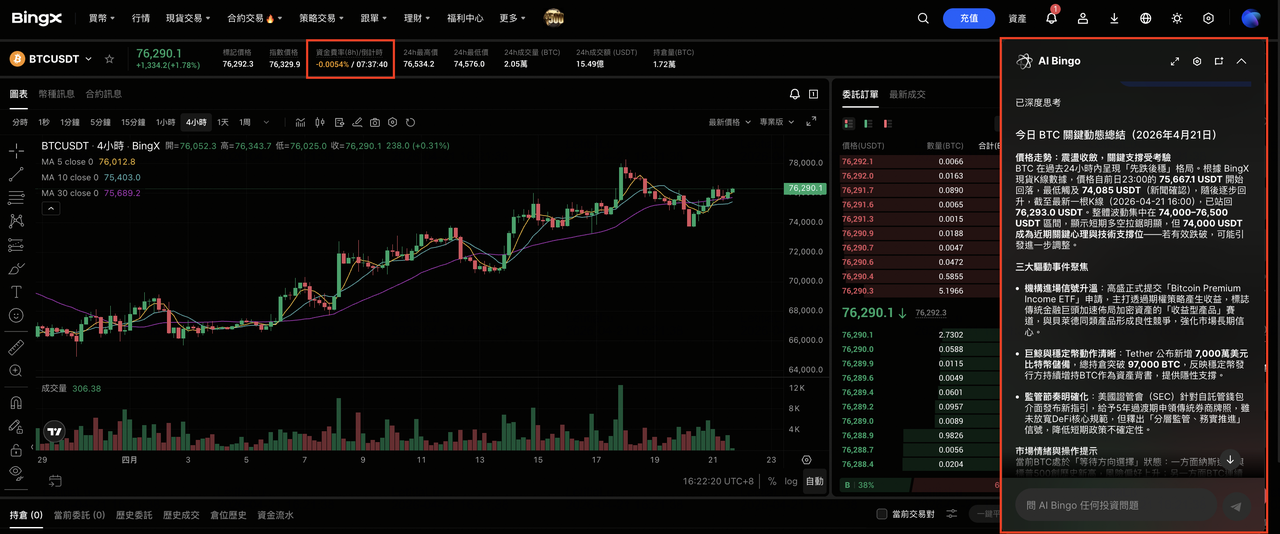

- BingX AI Assistance:BingX AI provides BTC market sentiment analysis, assisting in determining optimal timing for funding rate arbitrage position opening

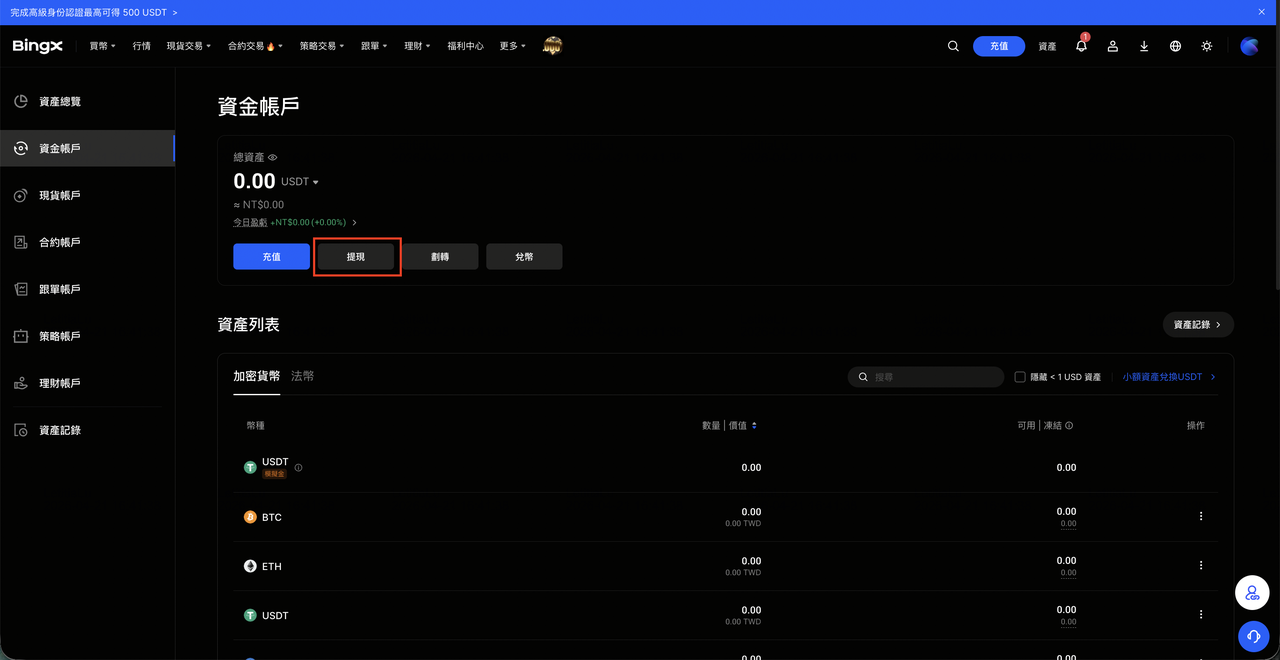

- TWD Withdrawal Path: USDT TRC-20 withdrawal fee under $1, convertible to TWD via MAX or BitoPro with clear processes

How to Execute Bitcoin Funding Rate Arbitrage on BingX: Step-by-Step Guide

Before starting BTC funding rate arbitrage execution, you must first complete BingX account registration and basic setup. It's recommended to register with a valid email or phone number and complete basic security settings (such as enabling 2FA), ensuring asset security. After registration, you can purchase USDT with credit cards or withdraw from other exchanges to BingX as arbitrage capital, preparing for subsequent operations.

The following is the standard process for executing BTC funding rate arbitrage on BingX, completely breaking down each key step from rate assessment, position opening to withdrawal.

Step 1: Check Funding Rate Direction and Size

Go to BingX BTC-USDT perpetual futures page, confirm the current funding rate is positive, and check the next settlement time. Consider entering when funding rates are above 0.05% (every 8 hours) to ensure sufficient space to cover transaction costs. Also review historical rate trends to confirm rates maintain stable positivity, avoiding uncertainties from short-term fluctuations. You can combine BingX AI market analysis to observe sentiment; when markets are bullish, funding rates are usually higher and more persistent.

Pre-Position Opening Quick Checklist:

- Is the funding rate positive (avoid reverse payments)

- Is the rate above 0.05% (every 8 hours)

- Have historical rates maintained consecutive positive values (not short-term spikes)

- Is there sufficient time until next settlement (avoid immediate settlement after opening)

- Is market sentiment bullish (increases rate persistence)

Step 2: Open Long Position on Spot Market

Enter "Spot Trading" → BTC/USDT, use limit orders to buy the target amount of BTC to control execution costs. After completion, precisely record the actual position size (e.g., 0.1 BTC), which will serve as the benchmark for subsequent futures hedging.

Spot Position Opening Checklist:

- Used limit orders (avoid taker fees increasing costs)

- Fill price within expected range

- Complete fill achieved (avoid partial fills affecting hedge)

- Actual position size recorded (e.g., 0.1 BTC)

- Trading fees included in cost calculations

Step 3: Open Equal Short Position on Futures

Go to "Assets" → "Fund Transfer", transfer USDT to futures account as margin. Enter BTC-USDT perpetual futures page, select "Isolated Margin Mode", set leverage to 1x, and use limit orders to open short positions exactly matching spot quantity (e.g., 0.1 BTC). After opening, verify again that spot and futures quantities match exactly to ensure positions are completely hedged.

Futures Hedging Checklist (Most Critical):

- Futures quantity exactly matches spot quantity (e.g., 0.1 BTC to 0.1 BTC)

- Using "Isolated Margin Mode" (avoid overall asset involvement)

- Leverage set to 1x (avoid additional risks)

- Using limit orders (control opening costs)

- Confirmed successful fill (avoid unfilled orders creating exposure)

- Spot and futures directions correct (spot long + futures short)

Step 4: Collect Funding Rate Settlement Returns

Funding rates settle every 8 hours (Taiwan time 08:00, 16:00, 00:00). When rates are positive, short position holders automatically receive compensation, with profits directly entering the futures account. You can check actual received amounts for each settlement through "Asset Records" → "USDⓢ-M Perpetual", selecting "Funding Fee" from the dropdown menu.

Step 5: Close Positions When the Rate Flips

When funding rates turn negative (short positions must pay fees), immediately end the strategy. Synchronously close both spot long and futures short positions to avoid reverse costs or unhedged risks. Both positions must be handled simultaneously to ensure complete strategy closure.

Position Closing Exit Checklist:

- Has funding rate turned negative or near 0 (arbitrage opportunity disappeared)

- Simultaneously closing both "spot long + futures short" positions (avoid single-sided exposure)

- Closing quantities exactly match original positions

- Both closing orders successfully filled (avoid remaining positions)

- Account has no remaining BTC and corresponding futures positions after closing

- Final profit check (still positive after deducting fees)

Step 6: Withdraw Profits and Complete TWD Off-Ramp

After profit accumulation, go to "Fund Account" → "Withdraw" to withdraw USDT, recommend using TRC-20 network (fees under $1). Transfer funds to MAX or BitoPro, sell USDT for TWD, and withdraw to bank accounts. Recommend keeping complete trading and fund flow records for subsequent tax reporting.

Extended Reading: Complete Comparison of Taiwan Cryptocurrency Fiat On/Off-Ramps: Which Platform Has Cheapest Deposits and Fastest Withdrawals? (2026)

Which BTC Arbitrage Method Is Most Cost-Efficient? Fees and Risks Compared

Whether arbitrage strategies are viable depends on whether overall costs can be covered by profits. Taking funding rate arbitrage as an example, position opening requires paying both spot and futures trading fees simultaneously. When executing on BingX, spot taker fee 0.1% plus futures taker fee 0.05% results in single-round costs of approximately 0.15%; using limit orders can reduce this to about 0.12%. Therefore, strategies only have sustained positive profit potential when funding rates consistently exceed this threshold.

In comparison, cross-exchange arbitrage involves not only trading fees but also withdrawal fees and fund transfer time costs, with spreads often converging rapidly during transfer periods. Triangular and statistical arbitrage don't involve cross-platform operations but face execution delay and model failure risks respectively. In other words, arbitrage costs come not only from fees but also execution efficiency and capital usage efficiency.

Overall, for Taiwanese individual investors, single-platform funding rate arbitrage remains the lowest-cost and most feasible entry method. Operations can begin with approximately 300 USDT, requiring no API or cross-platform fund transfers, with relatively simple strategy structure that's easier to execute long-term.

Extended Reading: Which Platform Has Lowest Bitcoin Purchase Fees in Taiwan? BTC Spread, Fee & Liquidity Comparison (2026)

|

Arbitrage Strategy |

Trading Fee Costs (Per Round) |

Other Costs/Risks |

Opening Cost Recoverability |

Capital Requirement |

Operational Barrier |

Suitable For |

|

BingX Funding Rate Arbitrage (Pure CEX) |

~0.15% (taker) / ~0.12% (limit) |

Rate reversal, position imbalance |

High |

~300 USDT |

Low |

Taiwanese entry arbitragers |

|

Cross-Exchange Spot Arbitrage |

~0.1%–0.2% + withdrawal fees |

Withdrawal delays, fund transfers, spread disappearance |

Medium |

~5,000 USDT+ |

High (API required) |

Advanced users |

|

Triangular Arbitrage |

~0.3% + (three trades) |

Execution delays, slippage |

Low |

~1,000 USDT |

Very High (low-latency programs required) |

Quantitative developers |

|

Statistical Arbitrage |

Varies by strategy |

Model failure, long-term holding costs |

Low |

~10,000 USDT+ |

Very High (quantitative capabilities required) |

Quantitative developers |

Best Tools and Security Practices for Advanced BTC Arbitrageurs

For users wanting to execute advanced strategies like cross-exchange arbitrage, triangular arbitrage, or statistical arbitrage, automation tools are almost essential. These arbitrage opportunities typically exist for extremely short periods (even millisecond-level), making manual operations unable to complete position opening before spreads disappear, thus requiring programs to continuously monitor multiple exchange quotes and automatically place orders. Additionally, these strategies usually require pre-configured funds across multiple platforms, further increasing the importance of fund management and security settings.

Current mainstream solutions include open-source programming frameworks (like Hummingbot), cloud subscription tools (like 3Commas, Cryptohopper), and self-built Python programs connecting to exchange APIs. The first two lower usage barriers but have limited flexibility and control; the latter provides maximum freedom but requires certain development capabilities. If using BingX as the primary execution platform, self-built programs connecting to APIs offer the highest flexibility for advanced solutions; while funding rate arbitrage can be completed within a single platform without needing automation systems.

Overall, advanced arbitrage (such as cross-exchange, triangular, or statistical arbitrage) almost all rely on automation tools and API frameworks, accompanied by higher capital requirements and security management demands; in comparison, funding rate arbitrage can be completed within a single platform without automation systems, remaining the lowest-barrier, most controllable risk entry method for Taiwanese individual investors.

Extended Reading: What's the Difference Between Scalping vs. Swing Trading in Futures? Complete 2026 Trading Strategy Comparison

|

Tool/Platform |

Type |

BingX Support |

Automation Level |

Suitable Strategies |

Capital & Security Mechanisms |

Usage Barrier |

|

BingX (Single Platform) |

Centralized Exchange |

✓ Native Support |

Low (Manual Possible) |

Funding Rate Arbitrage |

✓ Merkle Tree Proof of Reserves, User Protection Fund, IP Whitelist |

Low |

|

Hummingbot |

Open Source Framework |

Version-dependent |

High |

Cross-Exchange Arbitrage, Market Making |

Funds on exchanges, security depends on API settings |

High (Programming required) |

|

3Commas |

Cloud Subscription |

Version-dependent |

High |

Multi-Exchange Arbitrage Monitoring |

Third-party API authorization, withdrawal permissions must be restricted |

Medium |

|

Cryptohopper |

Cloud Subscription |

Version-dependent |

High |

Multi-Exchange Arbitrage, Backtesting |

Third-party API authorization, withdrawal permissions must be restricted |

Low to Medium |

|

Self-built Python + BingX API |

Custom Program |

✓ Native Support |

High |

Funding Rate Arbitrage, Cross-Exchange Arbitrage |

Customizable permissions & risk controls, highest flexibility |

High (Development capabilities required) |

5 Key Factors to Consider Before Bitcoin Arbitrage Trading

- Ensure Complete Position Hedging: Funding rate arbitrage requires simultaneously holding spot long positions and equal-sized futures short positions, with quantities exactly matching. Any difference represents unhedged directional risk that could generate losses exceeding rate income during BTC volatility. Confirm position matching immediately after opening.

- Continuously Monitor Funding Rate Changes: Funding rates fluctuate with market sentiment and may turn from positive to negative in short periods. Recommend setting rate alerts, particularly monitoring Taiwan time (UTC+8) 8:00, 16:00, 0:00 settlement times, adjusting or exiting strategies promptly when rates approach 0 or turn negative.

- Strengthen API and Account Security Settings: When using cross-exchange arbitrage tools (like Hummingbot) connecting to BingX API, enable IP whitelist and disable withdrawal permissions. API keys should not be stored in GitHub, Gmail, or messaging apps and other high-risk environments. Revoke and regenerate immediately if suspected compromise.

- Confirm Withdrawal Networks and Processes: When withdrawing USDT, ensure correct network selection. TRC-20 fees typically under $1, ERC-20 around $5-10. If network and address don't match, assets may be unrecoverable. Recommend small test transfers before large amounts.

- Maintain Transaction Records and Tax Planning: BTC arbitrage profits may be considered income in Taiwan. Recommend keeping complete records of position opening, closing, and fund flows for tax reporting. Consult crypto asset professionals when necessary.

Conclusion: Why BingX Is the Right Choice for Bitcoin Arbitrage in 2026

For Taiwanese BTC arbitrage investors, platform selection's core isn't just fee levels, but whether strategies can be executed stably with low friction. BingX's advantages are quite clear: spot and futures fee structures are simple and transparent, with competitive single-round position opening costs; funding rates and settlement times are visible in real-time, making arbitrage opportunities easier to assess; combined with complete Traditional Chinese interface, the entire operational flow from opening to closing positions is more intuitive, also reducing operational error risks.

Compared to advanced arbitrage methods requiring cross-platform fund transfers or complex tool dependencies, BingX supports completing entire funding rate arbitrage processes within a single platform, making strategy structure simpler with lower execution barriers. For most Taiwanese individual investors, this "directly usable, controllable cost" environment is key to whether arbitrage strategies can operate long-term.

Regardless of which arbitrage method is ultimately chosen, the ability to execute stably, control costs, and reduce operational risks is often more important than the strategy itself. For investors hoping to participate in BTC arbitrage systematically, starting with BingX's single-platform funding rate arbitrage is currently the most implementable and sustainable entry choice.

Related Reading

- Where to Buy Bitcoin in Taiwan? 2026 Bitcoin Exchange Recommendations and Complete Purchase Guide

- Taiwan Bitcoin Day Trading Platform Recommendations: Fee Comparison and Complete Operational Guide (2026)

- What's the Difference Between Scalping vs. Swing Trading in Futures? Complete 2026 Trading Strategy Comparison

- Complete Taiwan Cryptocurrency Futures Trading Platform Comparison (2026): Fee, Liquidity & Security Comparison

- Which Taiwan Exchange Is Best for Large Bitcoin Trading? Complete Platform Fee and Liquidity Comparison (2026)

- Which Platform Has Lowest Bitcoin Purchase Fees in Taiwan? BTC Spread, Fee & Liquidity Comparison (2026)