Executive Summary

The blockbuster public debut of Space Exploration Technologies Corp. (SPCX) on June 12, 2026, marked a watershed moment for global capital markets. By raising $75 billion at a fixed offering price of $135 per share, and immediately absorbing an additional $10.7 billion via the full execution of its 83.3 million-share over-allotment ("greenshoe") option, SpaceX locked in the largest initial public offering in human history.

On its first day of trading, intense institutional and retail demand propelled the stock to a 19.2% gain, closing its maiden session at $160.95 and elevating its valuation past $2.1 trillion. By the close of trading on June 15, momentum further accelerated, closing the session at $192.50, pushing its market capitalization over $2.5 trillion.

However, behind the retail frenzy lies a highly calculated, deterministic liquidity catalyst. Due to massive regulatory framework amendments enacted by global index providers, SpaceX has triggered an unprecedented, rapid index inclusion timeline. Over the next six weeks, a massive structural supply-demand mismatch will materialize, forcing global tracking funds and passive indices to absorb between $22 billion and $32.5 billion in raw SPCX equity.

This deep-dive institutional report details the mechanical timelines, index rules, structural constraints, and systematic tailwinds of the impending index rebalancing sweep.

SpaceX's Core Index Inclusion Timeline and Structural Rule Changes

Historically, megacap tech giants entering the public markets faced multi-month lag periods before indexing eligibility. Recognizing the risk of tracking errors for indexes excluding a $2 trillion asset, both the Nasdaq and FTSE Russell implemented historic rule changes prior to the offering.

SpaceX (SPCX) Index Inclusion Milestone Roadmap (2026–2027)

|

Target Date |

Index Milestone Event |

Operational Mechanics & Market Impact |

|

June 12, 2026 |

Nasdaq Public Debut Completed |

Stock officially opens for public trading at a $135 base IPO price, establishing its initial multi-trillion-dollar valuation baseline. |

|

June 27, 2026 |

Russell 1000 Reconstitution |

SPCX is officially added during the annual index restructuring. To minimize market shock, buying is distributed across a 5-day smoothing window. |

|

July 6, 2026 |

Nasdaq-100 "Fast Entry" Execution |

Triggers mandatory passive tracking buy sweeps on the 15th trading day of listing, creating a concentrated, highly deterministic single-day liquidity demand. |

|

After June 2027 |

S&P 500 Eligibility Window Opens |

Earliest potential date for S&P inclusion, contingent on the company meeting strict index mandates including a minimum 12-month trailing cumulative GAAP profit. |

- The June 12 Opener: SpaceX successfully launched on the Nasdaq under the ticker SPCX, closing at $160.65 (+19%) on day one with a float valuation of roughly $2.1 trillion.

- The June 27 Russell Reconstitution: Leveraging an amendment by FTSE Russell enabling megacap entrants to bypass standard lockouts after five days of trading, SPCX will be officially added during the Russell 1000 Annual Restructuring.

- The July 6 Nasdaq-100 Fast Entry: Under amended rules allowing fast-track entry on the 15th trading day for mega-IPOs matching top-tier capitalization thresholds, the index will implement a mandatory buy sweep on July 6.

- The S&P 500 Lag: Standard & Poor's enforces the most rigid barrier. SPCX will remain excluded until after June 2027, as the index requires a trailing 12-month consecutive GAAP profitability track record before considering inclusion.

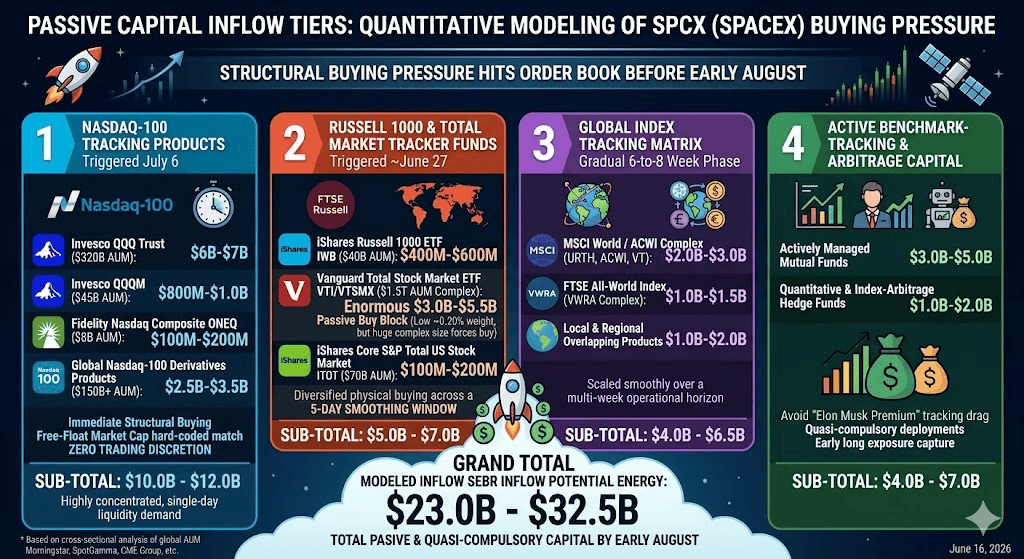

Quantitative Modeling: Passive Capital Inflow Tiers

A rigorous cross-sectional analysis of global assets under management (AUM) reveals four tiers of programmatic buying pressure that will hit the SPCX order book before early August.

Tier 1: Nasdaq-100 Tracking Products, Triggered on July 6

The Nasdaq-100 fast-track rule forces immediate structural buying across all benchmarked index funds and exchange-traded products. Because these allocations are hard-coded to match index weightings based on free-float market cap, fund managers possess zero trading discretion.

- Invesco QQQ Trust ($320 billion AUM): Estimated mandatory SPCX purchase size of $6.0 billion to $7.0 billion.

- Invesco QQQM ($45 billion AUM): Estimated mandatory SPCX purchase size of $800 million to $1.0 billion.

- Fidelity Nasdaq Composite ONEQ ($8 billion AUM): Estimated passive purchase size of $100 million to $200 million.

- Global Nasdaq-100 Derivatives/Tracking Products ($150 billion+ AUM): Estimated aggregate buy sweep of $2.5 billion to $3.5 billion.

- Tier 1 Subtotal: $10.0 billion to $12.0 billion in highly concentrated, single-day liquidity demand.

Tier 2: Russell 1000 and Total Market Tracker Funds, Triggered Around June 27

- iShares Russell 1000 ETF IWB ($40 billion AUM): Estimated purchase size of $400 million to $600 million.

- Vanguard Total Stock Market ETF VTI / VTSMX ($1.5 trillion AUM complex): Crucially, index compiler CRSP positions the float-adjusted market value of SPCX as "less than Top 100" due to its low initial float ratio, keeping VTI’s expected weight below 0.20%. However, because VTI’s aggregate tracking matrix exceeds $1.5 trillion, this minor weighting forces an enormous passive buy block of $3.0 billion to $5.5 billion.

- iShares Core S&P Total US Stock Market ITOT ($70 billion AUM): Estimated allocation of $100 million to $200 million.

- Tier 2 Subtotal: $5.0 billion to $7.0 billion. To mitigate sudden market impact, FTSE Russell has announced it will diversify its physical buying across a 5-day smoothing window rather than executing on a single close.

Tier 3: Global Index Tracking Matrix, Gradual 6-to-8 Week Phase

- MSCI World / ACWI Complex (URTH, ACWI, VT): Global indexes are modeling capital adjustments tracking $2.0 billion to $3.0 billion in multi-currency outflows into SPCX equity.

- FTSE All-World Index (VWRA Complex): Projecting systematic capital entry of $1.0 billion to $1.5 billion.

- Local & Regional Overlapping Products: Estimated at $1.0 billion to $2.0 billion.

- Tier 3 Subtotal: $4.0 billion to $6.5 billion scaled smoothly over a multi-week operational horizon.

Tier 4: Active Benchmark-Tracking and Arbitrage Capital

- Actively Managed Mutual Funds: Benchmarked long-only managers face extreme career risk if they underperform the newly altered Nasdaq/Russell indices. To avoid tracking drag caused by the 'Elon Musk Premium,' active capital is projected to deploy $3.0 billion to $5.0 billion.

- Quantitative and Index-Arbitrage Hedge Funds: Quantitative desks front-running the July 6 Nasdaq buy sweep are modeled to absorb $1.0 billion to $2.0 billion in early long exposure.

- Tier 4 Subtotal: $4.0 billion to $7.0 billion in quasi-compulsory capital deployments.

Structural Matrix: Total SPCX Buyer Potential Energy

|

Buyer Allocation Tier |

Estimated Purchase Scale |

Execution Time Window |

Operational Mandate Level |

|

Nasdaq-100 Passive Funds |

$10.0B – $12.0B |

July 6 Execution Window |

Absolute Mandatory (Single-Day Hard Target) |

|

Russell & Total Market Indexes |

$5.0B – $7.0B |

June 27 Execution Window |

Highly Mandatory (5-Day Smoothed Horizon) |

|

Global Index Complex (MSCI/FTSE) |

$4.0B – $6.5B |

Rolling Over 6 to 8 Weeks |

Highly Mandatory (Gradual Absorption) |

|

Active Benchmark Trackers |

$4.0B – $7.0B |

Continuous Post-June 12 |

Quasi-Compulsory (Career Risk Protection) |

|

Aggregate Capital Funnel |

$22.0B – $32.5B |

June 12 – Early August |

Systemic Liquidity Sweep |

SpaceX's Critical Liquidity Constraint: Available Circulating Float

The structural baseline of this market analysis rests on an extreme supply-demand mismatch. While the total asset value of SpaceX stretches beyond $2.5 trillion, the actual circulating liquid float available for open-market acquisition is severely constrained.

SPCX Circulating Float vs. Passive Index Demand

|

Liquidity Dynamic Component |

Capital Metric Value |

Structural Framework and Market Impact |

|

Total Post-Greenshoe Flooded Capital Base |

$85.7B Float-Adjusted Market Cap |

The total value of all public shares available on the open market following full execution of the over-allotment option. |

|

Minimum Mandatory Passive Index Demand |

$22.0B Fixed Inflow Requirement |

The baseline, non-discretionary capital tracking funds must buy to accurately match index weights. |

|

Maximum Modeled Institutional Demand |

$32.5B Combined Buying Pressure |

Total projected inflows including active benchmark-tracking capital and quantitative index arbitrageurs. |

Core Supply Parameters Based on SpaceX's S-1 Filing

- The Restricted Float Ratio: According to SpaceX's S-1 filing, the primary public offering represented an exceptionally thin outstanding share slice of only 4% to 5% of the enterprise's equity base.

- Absolute Float Value: Morningstar and Bloomberg calculate the current float-adjusted market value of outstanding shares between $87 billion and $90 billion.

- The Absorption Shock Index: Dividing the deterministic passive demand of $22 billion – $32.5 billion by the maximum available floating supply of $87 billion – $90 billion reveals that passive tracking index funds alone must aggressively purchase 24% to 36% of the entire circulating public supply of SpaceX in the open market.

- When adding active, non-discretionary portfolio adjustments, the total structural call on the public float scales to a staggering 35% to 40%.

Trading SPCX: Risk Assessment and Playbook for Strategic Traders

This quantitative setup creates a highly predictable, mechanical asset cycle characterized by two distinct phases: an initial capital squeeze followed by a supply-side cliff.

Phase 1: The Golden Window (June 16 – July 6)

This phase features an absolute demand monopoly. With $22B+ in guaranteed buyer flow matching against an order book with zero insider unlocking, the asset benefits from an artificial technical floor.

Short-term downside exposure is fundamentally insulated by index rebalancing rules. Price drops within this window represent clear institutional accumulation setups, as index managers are forced to buy all available liquidity blocks regardless of premium multiples.

Phase 2: The Demand Cliff and Supply Reversal (Post-July 6)

Immediately following the conclusion of the July 6 Nasdaq-100 mandatory buy sweep, the structural demand funnel drops to zero. Simultaneously, the market enters a sequence of multi-tiered supply unlock expansions.

- June 29 Retail Threshold: The initial 15-calendar-day retail "flipping" restriction implemented by major brokerages like Fidelity expires, freeing up to 30% of the initial retail allocation for short-term profit-taking.

- August 11 Insider Liquidation Line: The first tier of employee-owned equity and early-stage venture capital lockup waivers becomes eligible for public distribution, introducing a fresh supply block to the market.

How to Trade SpaceX (SPCX) on BingX

Maximizing the market mechanics of this historic listing is made seamless with BingX AI, which provides automated order routing and real-time capital flow analysis to optimize entries during the passive index buy window.

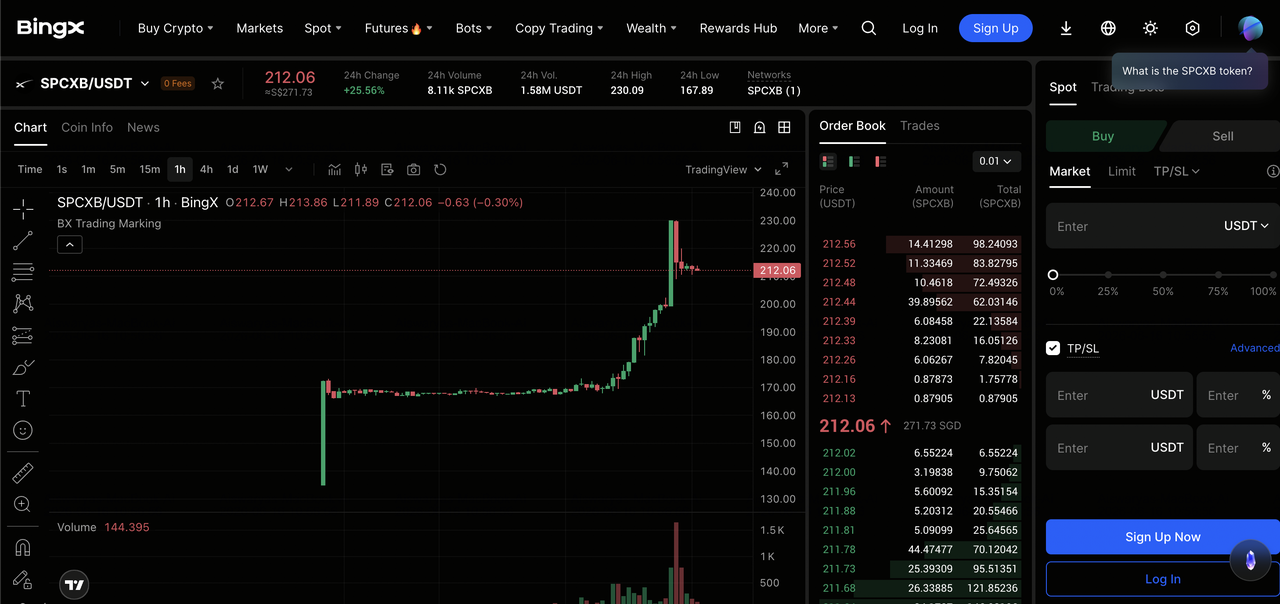

Buy, Sell, or HODL SpaceX Tokenized Stock (SPCXB) bStocks on the Spot Market

SPCXB/USDT trading pair on BingX spot market

- Navigate to the Spot Market: Log into your BingX account, hover over the Spot tab, and select Spot to look up the SPCXB/USDT pair.

- Execute Your Order: Analyze live order book depth, choose between a Limit or Market order type, enter your desired capital allocation, and confirm the purchase to secure the underlying asset in your spot wallet.

Read more: What Is SpaceX Tokenized Stock (SPCXB) and How to Buy It?

How to Trade SpaceX Futures via BingX TradFi

- Access TradFi Derivatives: Switch over to the BingX TradFi interface and navigate to the equity perpetuals tab to pull up the SPCX/USDT perpetual contract.

- Deploy Leveraged Capital: Select your margin mode, choose an appropriate leverage tier to navigate short-term volatility, and open a Long or Short position based on technical support retests or index inclusion dates.

Conclusion: Should You Invest in SpaceX (SPCX) Stock?

SpaceX’s equity structure represents a pure index-driven capital squeeze. For the next three weeks, traditional fundamental valuation models, such as Morningstar’s conservative $63 fair value target, will remain detached from market pricing due to indexing demands.

Traders should utilize this Golden Window to capture momentum but must maintain high vigilance and adjust defensive stops immediately following the July 6 index rebalance, protecting capital against the impending post-inclusion liquidity cliff.

Related Reading

- Top 10 Things to Know About the SpaceX IPO: Pricing, Valuation, and How to Trade It

- What Is SpaceX Tokenized Stock (SPCXB) and How to Buy It?

- Top Space Stocks to Buy Ahead of SpaceX IPO

- How to Trade SpaceX Pre-IPO on BingX Pre-IPO: SPACEX (VNTL), SPACEX (PreStocks), and SPCX

- How the SpaceX IPO on June 12 Is Launching Elon Musk Past the Trillion-Dollar Net Worth Mark